The value of an investment, and any income from it, can fall as well as rise and investors may not get back the amount invested.

Under the Radar

International Smaller Companies

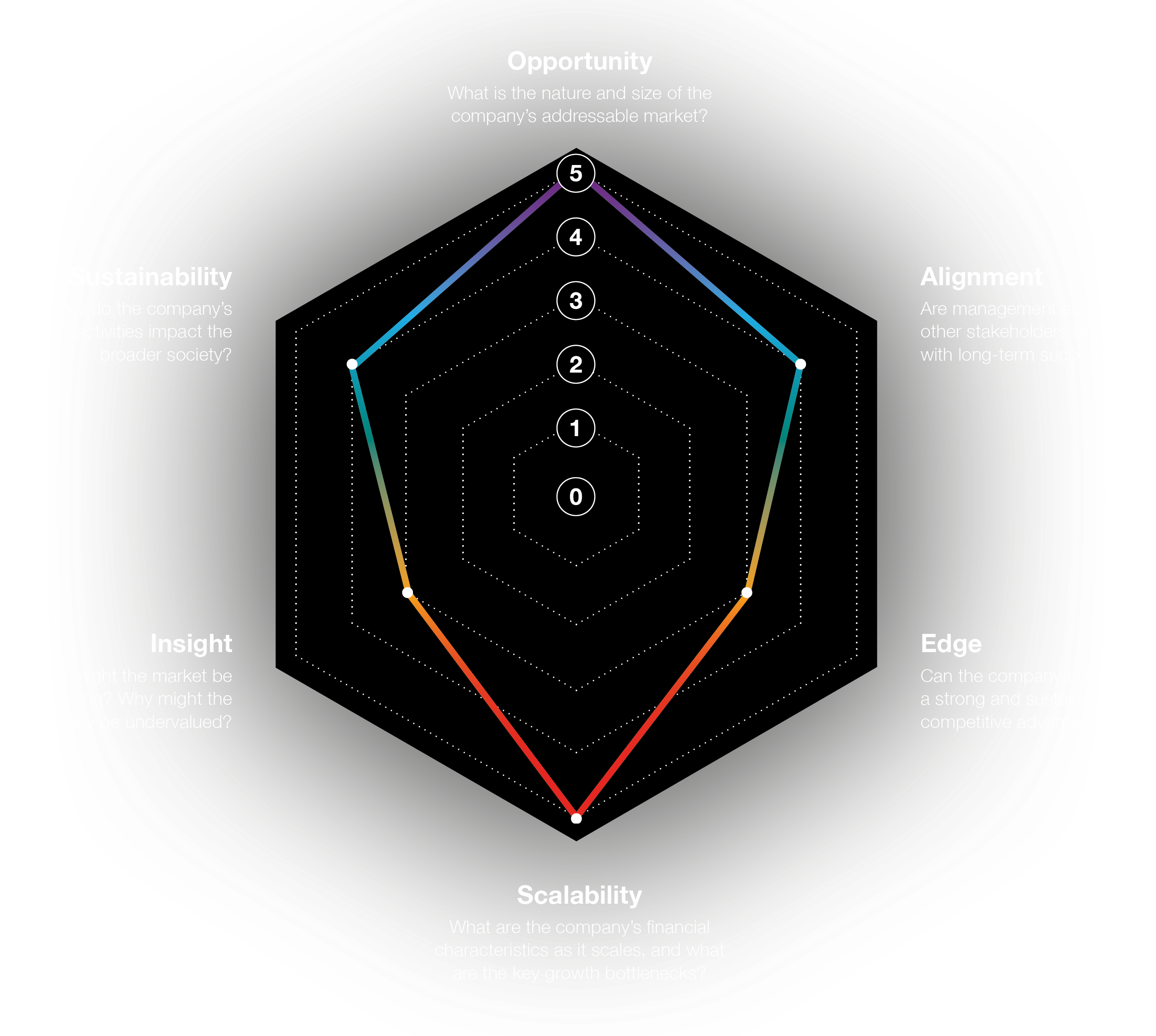

The idea of karma, or the notion that your thoughts and actions determine the life you lead, is an idea that permeates religion, either in terms of the ‘as you sow, so shall you reap’ teachings of Christianity or the ‘a man is born to the world he has made’ of Buddhist teaching. Without having to subscribe to either, Baillie Gifford’s International Smaller Companies team think that sustainability, which we frame as the question – how do the company’s activities impact the broader society? – warrants a place on our Radar framework to help us uncover the most exciting smaller companies from around the world to invest in.

We are not alone. One of the notable recent trends in our industry is the rising focus of environmental, societal and governance (ESG) issues. However, it can sometimes seem that the intent to do good is lost in translation, because there are conflicting principles as to what ESG investing should involve or indeed what it is it should be trying to achieve. Investors and their end clients consider ESG for a wide range of reasons and hence place it higher or lower on their list of investment priorities. Reflecting this diversity of emphasis, it follows that there are various terms floating around to describe these approaches. The problem is that the terms – socially responsible investing, impact investing, ethical investing, to name but a few – are being used interchangeably. As a result, it is not always clear to the end client what it is that they are subscribing to and, therefore, what they should be expecting to get from investing in this manner.

Our approach to ESG is simple. As investors in the International Smaller Companies team, we believe that assessing companies on ESG considerations ultimately helps us to improve investment returns. That we are also hopefully ‘doing the right thing’ by doing so is of course important to us, but we recognise that it is inevitably subjective and are keen to emphasise that this is not our starting point. Our mandate is to invest and generate meaningful investment returns over the long term for our clients.

Why should investors care?

Our impression is that despite mounting evidence, the assertion that ESG considerations are returns-enhancing remains needlessly contentious – particularly in relation to the E (Environmental) and S (Societal) within ESG. My colleague, Remya Nair, will cover Governance when we take a closer look at another spoke in the Radar, Alignment. Here we focus on the E and the S, or perhaps more intuitively, how a company deals with its stakeholders (we use this term in a general sense to cover not just employees, creditors and shareholders, but also the entire supply chain which the company is part of); and how this company contributes to and/or impacts the broader society. Environmental concerns should be considered an important subset of this, but for the main part, the paper addresses the wider issue of sustainability.

For investors with a long investment horizon, the link between high returns and sustainability is completely logical. Indeed, a company’s approach on sustainability matters may well be the most powerful indicator there is of a company’s quality and its culture. A management team that thinks deeply about its company’s role within society and its interactions with its stakeholders will be naturally long-term orientated (just as we are at Baillie Gifford); whereas lesser executives, sometimes through an excessive focus on specific targets (usually financial), often compromise the longer-term robustness and development of the company in one way or another. There are endless examples of companies failing to invest in promising opportunities because of the shorter-term hit to profits that would ensue, and of companies that encounter serious operational issues because they have neglected the interests of one or other stakeholder groups. Industrial actions, regulatory clamp-downs/controls, supply chain disruptions, customer backlash, mass data leaks and so on, do not happen purely by accident. What goes around, comes around.

A company’s approach on sustainability matters may well be the most powerful indicator there is of a company’s quality and its culture…What goes around, comes around.

One way to view sustainability considerations, therefore, is to see it as a proactive risk management tool that works on an individual stock level. Companies that are run sustainably, in a broad sense of the word as applied here, are less prone to ‘going wrong’, all else being equal. But this would be massively understating the significance of sustainability – for many companies in our portfolio, the relationship with sustainability runs far deeper than just reducing risk.

From our point of view, researching smaller companies, studying a company’s philosophy and policies on sustainability is often particularly revealing. The relative lack of resources means that many simply don’t have specialist teams to implement comprehensive ESG ‘best practises’ or shout about these policies through glossy publications – and nor do we necessarily want to encourage our investee companies to do so. What a company chooses to do tells us a lot about who they really are and what really matters. The importance of this is exacerbated because information for smaller companies is often less readily available – a challenge that we face across all aspects of small cap investing – and understanding the underlying viewpoint of the company’s management is therefore crucial.

What's in it for Business?

Consider the following quote, courtesy of Brunello Cucinelli – the eponymous founder of the Italian luxury company best known for cashmere knitwear:

I believe in a humanistic enterprise: business should comply in the noblest manner with all the rules of ethics that man has devised over the centuries. I dream about a form of humanistic modern capitalism with strong ancient roots, where profit is made without harm or offence to anyone, and part of it is set aside for any initiative that can really improve the condition of human life: services, schools, places of worship and cultural heritage. In my organization the focal point is the common good, which is the guiding force in pursuing prudent and courageous actions. In my business, people are at the very center of every production process, because I am convinced that human dignity is restored solely through the rediscovery of the conscience. Work elevates human dignity and the emotional ties that derive from it.

Our research suggests that his company practises what Cucinelli preaches. Employees are treated well – there is a very strong emphasis on work-life balance (e.g. a no-email policy after 5.30pm!) and staff enjoy salaries significantly above the industry average, among other perks. Solomeo, a hilltop medieval hamlet in rural Umbria where Brunello Cucinelli is now headquartered, has largely been renovated from Cucinelli’s philanthropy over the past 30 years. Sure, these policies help boost staff morale, which in turn benefits the company. But this is also the essence of the brand upon which the business is built upon. Customers aren’t just paying for the cashmere, but also the ethos of the company.

For other companies, sustainability provides direct business opportunities. Katitas, a Japanese housebuilder, has a business model that involves buying derelict homes, and selling them after refurbishment. It may not seem like a revolutionary idea, but it is unusual in a market dominated by new builds, where houses are typically knocked down after two or three decades. Katitas’s opportunity is therefore sizeable. It directly addresses Japan’s chronic housing shortage by providing affordable, good quality homes, often helping to revitalise local communities in decline in

the process.

The last example that I would like to highlight is FDM, a British company that provides IT and business consultants to a range of client companies. On the face of it, it is an IT staffing company. However, FDM not only recruits its consultants (known as ‘Mounties’) from a much wider variety of backgrounds than is the norm for the industry, but it also puts them through its own two-year IT training programme. This includes those with non-technical university degrees, ex-military personnel and those returning to work. FDM’s contribution and support towards social mobility as well as women in tech (a zero gender pay gap and circa 50% female in senior management) are particularly noteworthy. Is this altruistic? Not completely – FDM’s positioning plainly makes business sense. Qualified IT professionals are in short supply, the company’s established ‘Mounties model’ taps into relatively under-explored talent pools and it helps guarantee a supply of consultants. It ultimately allows the company to scale into a vast, exciting market opportunity.

Integrating Sustainability into Investment Practice

Having articulated why sustainability is an important investment factor, just as assessing a company’s market opportunity and competitive edge are, it follows to ask how we incorporate sustainability considerations into the International Smaller Companies’ investment process.

Despite assigning each company a score against sustainability, as we do for all six factors on our Radar framework, this does not reflect a quantitative measurement of an individual sustainability marker, or such like. Instead, our aim is to assess sustainability in an integrated and largely qualitative manner based on the unique circumstances and traits of the companies that we are researching, drawing upon specialist help from our own Governance & Sustainability team as required (who will also provide a degree of independent portfolio challenge on a periodic basis). While our methodology may not appear particularly systematic, nor should it be. Each company has its own set of sustainability-related opportunities and challenges. That is why we are sceptical of companies (and rating agencies) that approach ESG with a tick-box mentality.

Another tangible output of our explicit acknowledgement of sustainability as a key investment factor is that it helps us as shareholders to engage with companies. As much as we like to think that our companies are well run and are thoughtful on sustainability matters, many are far from perfect and have significant challenges of their own, whether it is a company specific issue or one that impacts the whole industry. For example, while we admire Brunello Cucinelli’s humanist philosophy, our research on cashmere sourcing also highlighted that the social and ecological impact of cashmere production; and the supply chain, much of it based in Mongolia, may well be vulnerable to sudden environmental changes. As a result, we are engaging directly with the company to understand more about the company’s policies, and as shareholders with a long-term horizon, encourage the company to further improve their approach.

Karma is Everything

Summing up, what is sustainability to us? The answer is multi-faceted. Sustainability is Opportunity – think Katitas’ market. Sustainability is Edge – think Brunello Cucinelli’s brand. Sustainability is a big part of Alignment. Sustainability helps us understand a company’s potential to Scale – think of FDM’s Mounties model. And for us, sustainability is a powerful source of Insight and a core part of our investment philosophy.

Ultimately, no company operates in isolation. The long-term prospect of each company and its individual array of stakeholders is intertwined in complex and often unpredictable ways. Sustainability is simply a lens through which we try to understand where the opportunities and tensions are in a company’s web of interdependence with the broader society, and what the company is doing about them. Often, it involves an explicit cost to the companies; and benefits that are indirect, uncertain. In a general sense, sustainability is the cultivation of good karma.

Risk Factors

The views expressed in this article are those of the International Smaller Companies team and should not be considered as advice or a recommendation to buy, sell or hold a particular investment. They reflect personal opinion and should not be taken as statements of fact nor should any reliance be placed on them when making investment decisions.

This communication was produced and approved in March 2022 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

Potential for profit and loss

All investment strategies have the potential for profit and loss, your or your clients’ capital may be at risk. Past performance is not a guide to future returns.

Stock examples

Any stock examples and images used in this article are not intended to represent recommendations to buy or sell, neither is it implied that they will prove profitable in the future. It is not known whether they will feature in any future portfolio produced by us. Any individual examples will represent only a small part of the overall portfolio and are inserted purely to help illustrate our investment style.

This article contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research and Baillie Gifford and its staff may have dealt in the investments concerned.

Baillie Gifford holds the following stocks: Brunello Cucinelli, FDM, Katitas.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this article are for illustrative purposes only.

Important information

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). Baillie Gifford & Co Limited is an Authorised Corporate Director of OEICs.

Baillie Gifford Overseas Limited provides investment management and advisory services to non-UK Professional/ Institutional clients only. Baillie Gifford Overseas Limited is wholly owned by Baillie Gifford & Co. Baillie Gifford & Co and Baillie Gifford Overseas Limited are authorised and regulated by the FCA in the UK.

Persons resident or domiciled outside the UK should consult with their professional advisers as to whether they require any governmental or other consents in order to enable them to invest, and with their tax advisers for advice relevant to their own particular circumstances.

Financial intermediaries

This communication is suitable for use of financial intermediaries. Financial intermediaries are solely responsible for any further distribution and Baillie Gifford takes no responsibility for the reliance on this document by any other person who did not receive this document directly from Baillie Gifford.

Europe

Baillie Gifford Investment Management (Europe) Limited provides investment management and advisory services to European (excluding UK) clients. It was incorporated in Ireland in May 2018 and is authorised by the Central Bank of Ireland. Through its MiFID passport, it has established Baillie Gifford Investment Management (Europe) Limited (Frankfurt Branch) to market its investment management and advisory services and distribute Baillie Gifford Worldwide Funds plc in Germany. Similarly, it has established Baillie Gifford Investment Management (Europe) Limited (Amsterdam Branch) to market its investment management and advisory services and distribute Baillie Gifford Worldwide Funds plc in The Netherlands. Baillie Gifford Investment Management (Europe) Limited also has a representative office in Zurich, Switzerland pursuant to Art. 58 of the Federal Act on Financial Institutions (‘FinIA’). It does not constitute a branch and therefore does not have authority to commit Baillie Gifford Investment Management (Europe) Limited. It is the intention to ask for the authorisation by the Swiss Financial Market Supervisory Authority (FINMA) to maintain this representative office of a foreign asset manager of collective assets in Switzerland pursuant to the applicable transitional provisions of FinIA. Baillie Gifford Investment Management (Europe) Limited is a wholly owned subsidiary of Baillie Gifford Overseas Limited, which is wholly owned by Baillie Gifford & Co.

Hong Kong

Baillie Gifford Asia (Hong Kong) Limited 柏基亞洲(香港)有限公司 is wholly owned by Baillie Gifford Overseas Limited and holds a Type 1 and a Type 2 license from the Securities & Futures Commission of Hong Kong to market and distribute Baillie Gifford’s range of collective investment schemes to professional investors in Hong Kong. Baillie Gifford Asia (Hong Kong) Limited 柏基亞洲(香港)有限公司 can be contacted at Suites 2713–2715, Two International Finance Centre, 8 Finance Street, Central, Hong Kong. Telephone +852 3756 5700.

South Korea

Baillie Gifford Overseas Limited is licensed with the Financial Services Commission in South Korea as a cross border Discretionary Investment Manager and Non-discretionary Investment Adviser.

Japan

Mitsubishi UFJ Baillie Gifford Asset Management Limited (‘MUBGAM’) is a joint venture company between Mitsubishi UFJ Trust & Banking Corporation and Baillie Gifford Overseas Limited. MUBGAM is authorised and regulated by the Financial Conduct Authority.

Australia

Baillie Gifford Overseas Limited (ARBN 118 567 178) is registered as a foreign company under the Corporations Act 2001 (Cth) and holds Foreign Australian Financial Services Licence No 528911. This material is provided to you on the basis that you are a ‘wholesale client’ within the meaning of section 761G of the Corporations Act 2001 (Cth) (‘Corporations Act’). Please advise Baillie Gifford Overseas Limited immediately if you are not a wholesale client. In no circumstances may this material be made available to a ‘retail client’ within the meaning of section 761G of the Corporations Act.

This material contains general information only. It does not take into account any person’s objectives, financial situation or needs.

South Africa

Baillie Gifford Overseas Limited is registered as a Foreign Financial Services Provider with the Financial Sector Conduct Authority in South Africa.

North America

Baillie Gifford International LLC is wholly owned by Baillie Gifford Overseas Limited; it was formed in Delaware in 2005 and is registered with the SEC. It is the legal entity through which Baillie Gifford Overseas Limited provides client service and marketing functions in North America. Baillie Gifford Overseas Limited is registered with the SEC in the United States of America.

The Manager is not resident in Canada, its head office and principal place of business is in Edinburgh, Scotland. Baillie Gifford Overseas Limited is regulated in Canada as a portfolio manager and exempt market dealer with the Ontario Securities Commission (‘OSC’). Its portfolio manager licence is currently passported into Alberta, Quebec, Saskatchewan, Manitoba and Newfoundland & Labrador whereas the exempt market dealer licence is passported across all Canadian provinces and territories. Baillie Gifford International LLC is regulated by the OSC as an exempt market and its licence is passported across all Canadian provinces and territories. Baillie Gifford Investment Management (Europe) Limited (‘BGE’) relies on the International Investment Fund Manager Exemption in the provinces of Ontario and Quebec.

Oman

Baillie Gifford Overseas Limited (‘BGO’) neither has a registered business presence nor a representative office in Oman and does not undertake banking business or provide financial services in Oman. Consequently, BGO is not regulated by either the Central Bank of Oman or Oman’s Capital Market Authority. No authorization, licence or approval has been received from the Capital Market Authority of Oman or any other regulatory authority in Oman, to provide such advice or service within Oman. BGO does not solicit business in Oman and does not market, offer, sell or distribute any financial or investment products or services in Oman and no subscription to any securities, products or financial services may or will be consummated within Oman. The recipient of this material represents that it is a financial institution or a sophisticated investor (as described in Article 139 of the Executive Regulations of the Capital Market Law) and that its officers/employees have such experience in business and financial matters that they are capable of evaluating the merits and risks of investments.

Qatar

The materials contained herein are not intended to constitute an offer or provision of investment management, investment and advisory services or other financial services under the laws of Qatar. The services have not been and will not be authorised by the Qatar Financial Markets Authority, the Qatar Financial Centre Regulatory Authority or the Qatar Central Bank in accordance with their regulations or any other regulations in Qatar.

Israel

Baillie Gifford Overseas is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755–1995 (the Advice Law) and does not carry insurance pursuant to the Advice Law. This material is only intended for those categories of Israeli residents who are qualified clients listed on the First Addendum to the Advice Law.

Ref: 19851 10009601