The value of an investment, and any income from it, can fall as well as rise and investors may not get back the amount invested.

Under the Radar

International Smaller Companies

As with most professions, elements of what we do are often misunderstood. For us, mentioning the fact that we are investors to family and friends tends to elicit a particular response. There is an assumption that we dissect company financials forensically and are all accounting standards connoisseurs. Understandably, we don’t always argue against these misplaced assumptions! Numbers clearly matter – after all, a company’s intrinsic value reflects expectations for its future cashflows. Its financials help us understand how the business works, give a comparatively unbiased snapshot of its recent past, and help us imagine the company’s prospects. But numbers are just part of the story.

It surprises some who are less familiar with our industry that investors can approach analysis from various angles, depending on their investment mandate and style. Many people see analysis as being similar to a general healthcare check, or a vehicle inspection. That is not the case. The fundamental difference is that these checks are designed to detect what may go wrong, rather than what can go right.

By contrast, our work is perhaps more akin to running a screening programme for future Olympic champions, rather than spotting early symptoms for common diseases. Talent scouts in gymnastics looking for the next Simone Biles do not apply the same methods as those hunting for the new Michael Phelps in the swimming pool. However, the commonality is that finding a few superstars matters much more than avoiding the complete failures. It’s a fact of life that some prospects simply don’t work out, but there will be some star performers. Similarly, in equities investing, our success will likely be determined by the relatively small proportion of real winners.

We appreciate that potential returns are highly asymmetric. At a stock level, the most we can lose if we get it completely wrong is 100 per cent. If we get it right, the upside is often a multiple of our initial investment. Even moderately-growing companies can go up multiple times over five to 10 years (our typical holding period) as compounding effects take hold. Investors in smaller companies are particularly blessed with a fertile hunting ground for such opportunities, given the breadth of the universe, the diversity within it, and the inefficiencies of the market.

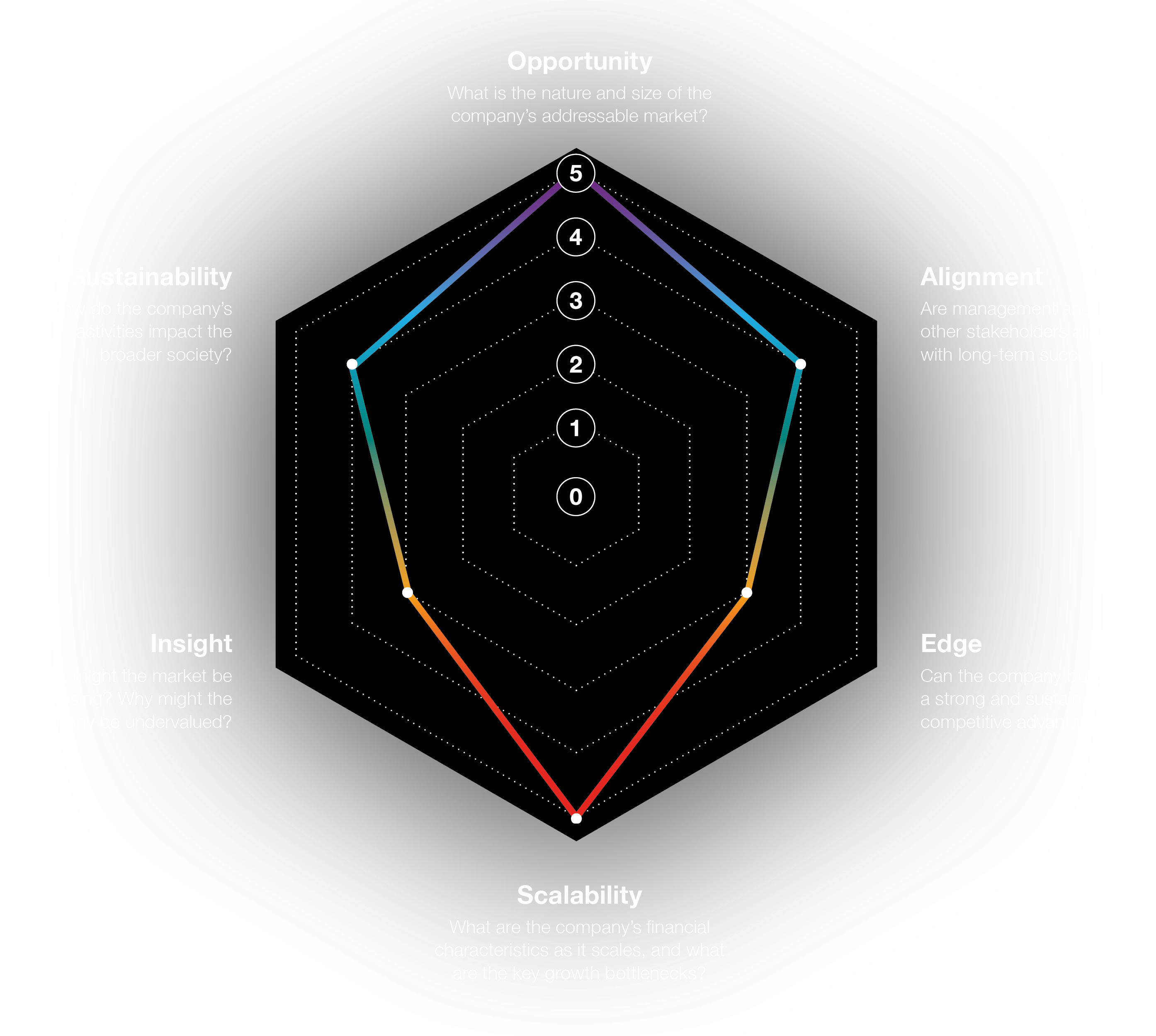

Besides using scalability as a model to help gauge the potential upside at the inception of an investment, it is also a powerful framework to monitor a company’s development.

The core message here is that, with an eye on the long-term upside, having a clear understanding of the company’s ability to scale up its business is what matters. Going back to our Radar research framework – if Opportunity addresses WHERE a company can get to, Edge looks at WHY this company may get there (as opposed to one of its competitors), and Alignment analyses WHO is driving the business forward; the question of scalability looks at how this will happen.

This raises several questions. How does a company grow into the opportunity that we identified and what are the underlying mechanics of that growth? Will progress likely happen through periods of dramatic growth spurts or steadily over the long run? Will this need multiple injections of capital or can growth be self-funded? Does the company benefit simply from increasing scale, or are there more powerful network effects at play? Answering these questions is a way of teasing out potential investment pay-off if the company succeeds.

Besides using scalability as a model to help gauge the potential upside at the inception of an investment, it is also a powerful framework to monitor a company’s development. The practical outcome in thinking about scalability is the clear identification of the key bottlenecks. When these bottlenecks shift (whether fundamentally, or simply our assessment of them), we pay attention. The rest of the time, ‘company news’ is often just noise.

Bottlenecks in our context come in many different forms, and every company has them. Some are related to the nature of the company’s markets and products. For example, we invest in a number of biotechnology companies that are commercialising novel therapies. It takes years for something to get from the lab to the clinic and eventually to become medical orthodoxy, almost regardless of the availability of capital and how promising the initial breakthrough is.

When Japan introduced a new conditional approval system for novel therapies based on regenerative medicine in 2015, it cleared the way for Japanese biotechs such as Healios to commercialise new therapies based on advances in induced pluripotent stem cells. For other markets, companies with innovative products are often fighting against inertia – enterprise software is one obvious product category where sales and implementation processes can be painfully long in some cases – almost regardless of how compelling the product is. Decision making within corporates often goes far beyond ‘does this make sense for the company?’. Understanding friction points in these processes is crucial. An example is Kinaxis – a Canadian software company that sells complex supply chain simulation tools to some of the largest enterprises in the world. It can take up to two years for the company to bring a new client on board, but we have been encouraged that implementation is now increasingly done through external partners, a shift that hints

at improving scalability.

Other bottlenecks can be internal in nature. Some businesses are naturally capital intensive, limiting growth as capital is tied up by the business for extended periods rather than reinvested to accelerate growth. For others, there may be operational constraints if parts of the operations are unable to keep pace with the rest of the business. For example, it may be difficult to recruit and retain a specific type of employee with sought-after expertise. Or perhaps there are constraints in the supplier base.

Nakedwines.com, an online wine retailer Naked Wines, is an interesting case study. The business model is that its customers, by paying a monthly subscription (effectively prepayment for wines), contribute towards a fund that in turn invests in independent winemakers. In return, these subscribers, known as Angels, get exclusive access to their products at wholesale prices. The main bottleneck is clear – independent winemakers with the right combination of ambitions and qualities do not roll off a production line. Thus far, the company has invested in over 150 winemakers from around the world, but there remains a waiting list to become an Angel. In a virtuous cycle where an increasing pool of committed Angels and winemakers stimulate the growth of each other, the limiting factor to growth appears to be the latter. An understanding of this underlying dynamic allows us to appreciate the strategic priorities of the company, and to assess the long-term potential of the business in a more nuanced fashion.

Finally, there are cases where the most pressing bottleneck is a company’s mindset. It may be shaped by the management’s motivations and experiences, the history of the business, or the circumstances of its shareholder base. These are intangible factors that are often poorly captured by numbers and underline why direct and open engagement with our investee companies is an integral part of our process.

Conclusion

Scalability is the capacity of an entity to be changed in scale. In a financial context, it is sometimes seen as a matter of mechanics describing revenue growth and how profitability follows. From our perspective, it is one of our core investment factors because it helps us to assess upside and ongoing progress.

Understanding scalability requires not just a grasp of the mechanics, but also an appreciation of the unique mix of tangible and intangible bottlenecks that a company has, as well as the recognition that progress is rarely smooth. Indeed, most companies that we invest in ultimately fall way short of what we might expect of them. However, the minority – those that at least get close to delivering on their potential and deliver multiples of the initial investment – make all the difference.

Risk factors

The views expressed in this article are those of the International Smaller Companies team and should not be considered as advice or a recommendation to buy, sell or hold a particular investment. They reflect personal opinion and should not be taken as statements of fact nor should any reliance be placed on them when making investment decisions.

This communication was produced and approved in March 2022 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

Potential for profit and loss

All investment strategies have the potential for profit and loss, your or your clients’ capital may be at risk. Past performance is not a guide to future returns.

Stock examples

Any stock examples and images used in this article are not intended to represent recommendations to buy or sell, neither is it implied that they will prove profitable in the future. It is not known whether they will feature in any future portfolio produced by us. Any individual examples will represent only a small part of the overall portfolio and are inserted purely to help illustrate our investment style.

This article contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research and Baillie Gifford and its staff may have dealt in the investments concerned.

Baillie Gifford holds the following stocks: Brunello Cucinelli, FDM, Katitas.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this article are for illustrative purposes only.

Important information

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). Baillie Gifford & Co Limited is an Authorised Corporate Director of OEICs.

Baillie Gifford Overseas Limited provides investment management and advisory services to non-UK Professional/ Institutional clients only. Baillie Gifford Overseas Limited is wholly owned by Baillie Gifford & Co. Baillie Gifford & Co and Baillie Gifford Overseas Limited are authorised and regulated by the FCA in the UK.

Persons resident or domiciled outside the UK should consult with their professional advisers as to whether they require any governmental or other consents in order to enable them to invest, and with their tax advisers for advice relevant to their own particular circumstances.

Financial intermediaries

This communication is suitable for use of financial intermediaries. Financial intermediaries are solely responsible for any further distribution and Baillie Gifford takes no responsibility for the reliance on this document by any other person who did not receive this document directly from Baillie Gifford.

Europe

Baillie Gifford Investment Management (Europe) Limited provides investment management and advisory services to European (excluding UK) clients. It was incorporated in Ireland in May 2018 and is authorised by the Central Bank of Ireland. Through its MiFID passport, it has established Baillie Gifford Investment Management (Europe) Limited (Frankfurt Branch) to market its investment management and advisory services and distribute Baillie Gifford Worldwide Funds plc in Germany. Similarly, it has established Baillie Gifford Investment Management (Europe) Limited (Amsterdam Branch) to market its investment management and advisory services and distribute Baillie Gifford Worldwide Funds plc in The Netherlands. Baillie Gifford Investment Management (Europe) Limited also has a representative office in Zurich, Switzerland pursuant to Art. 58 of the Federal Act on Financial Institutions (‘FinIA’). It does not constitute a branch and therefore does not have authority to commit Baillie Gifford Investment Management (Europe) Limited. It is the intention to ask for the authorisation by the Swiss Financial Market Supervisory Authority (FINMA) to maintain this representative office of a foreign asset manager of collective assets in Switzerland pursuant to the applicable transitional provisions of FinIA. Baillie Gifford Investment Management (Europe) Limited is a wholly owned subsidiary of Baillie Gifford Overseas Limited, which is wholly owned by Baillie Gifford & Co.

Hong Kong

Baillie Gifford Asia (Hong Kong) Limited 柏基亞洲(香港)有限公司 is wholly owned by Baillie Gifford Overseas Limited and holds a Type 1 and a Type 2 license from the Securities & Futures Commission of Hong Kong to market and distribute Baillie Gifford’s range of collective investment schemes to professional investors in Hong Kong. Baillie Gifford Asia (Hong Kong) Limited 柏基亞洲(香港)有限公司 can be contacted at Suites 2713–2715, Two International Finance Centre, 8 Finance Street, Central, Hong Kong. Telephone +852 3756 5700.

South Korea

Baillie Gifford Overseas Limited is licensed with the Financial Services Commission in South Korea as a cross border Discretionary Investment Manager and Non-discretionary Investment Adviser.

Japan

Mitsubishi UFJ Baillie Gifford Asset Management Limited (‘MUBGAM’) is a joint venture company between Mitsubishi UFJ Trust & Banking Corporation and Baillie Gifford Overseas Limited. MUBGAM is authorised and regulated by the Financial Conduct Authority.

Australia

Baillie Gifford Overseas Limited (ARBN 118 567 178) is registered as a foreign company under the Corporations Act 2001 (Cth) and holds Foreign Australian Financial Services Licence No 528911. This material is provided to you on the basis that you are a ‘wholesale client’ within the meaning of section 761G of the Corporations Act 2001 (Cth) (‘Corporations Act’). Please advise Baillie Gifford Overseas Limited immediately if you are not a wholesale client. In no circumstances may this material be made available to a ‘retail client’ within the meaning of section 761G of the Corporations Act.

This material contains general information only. It does not take into account any person’s objectives, financial situation or needs.

South Africa

Baillie Gifford Overseas Limited is registered as a Foreign Financial Services Provider with the Financial Sector Conduct Authority in South Africa.

North America

Baillie Gifford International LLC is wholly owned by Baillie Gifford Overseas Limited; it was formed in Delaware in 2005 and is registered with the SEC. It is the legal entity through which Baillie Gifford Overseas Limited provides client service and marketing functions in North America. Baillie Gifford Overseas Limited is registered with the SEC in the United States of America.

The Manager is not resident in Canada, its head office and principal place of business is in Edinburgh, Scotland. Baillie Gifford Overseas Limited is regulated in Canada as a portfolio manager and exempt market dealer with the Ontario Securities Commission (‘OSC’). Its portfolio manager licence is currently passported into Alberta, Quebec, Saskatchewan, Manitoba and Newfoundland & Labrador whereas the exempt market dealer licence is passported across all Canadian provinces and territories. Baillie Gifford International LLC is regulated by the OSC as an exempt market and its licence is passported across all Canadian provinces and territories. Baillie Gifford Investment Management (Europe) Limited (‘BGE’) relies on the International Investment Fund Manager Exemption in the provinces of Ontario and Quebec.

Oman

Baillie Gifford Overseas Limited (‘BGO’) neither has a registered business presence nor a representative office in Oman and does not undertake banking business or provide financial services in Oman. Consequently, BGO is not regulated by either the Central Bank of Oman or Oman’s Capital Market Authority. No authorization, licence or approval has been received from the Capital Market Authority of Oman or any other regulatory authority in Oman, to provide such advice or service within Oman. BGO does not solicit business in Oman and does not market, offer, sell or distribute any financial or investment products or services in Oman and no subscription to any securities, products or financial services may or will be consummated within Oman. The recipient of this material represents that it is a financial institution or a sophisticated investor (as described in Article 139 of the Executive Regulations of the Capital Market Law) and that its officers/employees have such experience in business and financial matters that they are capable of evaluating the merits and risks of investments.

Qatar

The materials contained herein are not intended to constitute an offer or provision of investment management, investment and advisory services or other financial services under the laws of Qatar. The services have not been and will not be authorised by the Qatar Financial Markets Authority, the Qatar Financial Centre Regulatory Authority or the Qatar Central Bank in accordance with their regulations or any other regulations in Qatar.

Israel

Baillie Gifford Overseas is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755–1995 (the Advice Law) and does not carry insurance pursuant to the Advice Law. This material is only intended for those categories of Israeli residents who are qualified clients listed on the First Addendum to the Advice Law.

Ref: 19850 10009603