All investment strategies have the potential for profit and loss, capital is at risk. Past performance is not a guide to future returns.

© Wachirawit Iemlerkchai / Alamy Stock Photo

Fusajiro Yamauchi may not be a familiar name to you, but over 130 years ago, he founded a company that now has one of the world’s most widely recognised brands: Nintendo.

Despite its longevity in an industry where success is fleeting and failure frequent, market pundits are pondering Nintendo’s prospects. They are questioning where the Switch – a hybrid console allowing users to play at home or on the go – is in its cycle and if gamers will substitute it for other forms of entertainment, post-pandemic.

Our investment case is different and is based on two main assumptions:

1. Nintendo owns some of the best and most recognisable brands and franchises in gaming

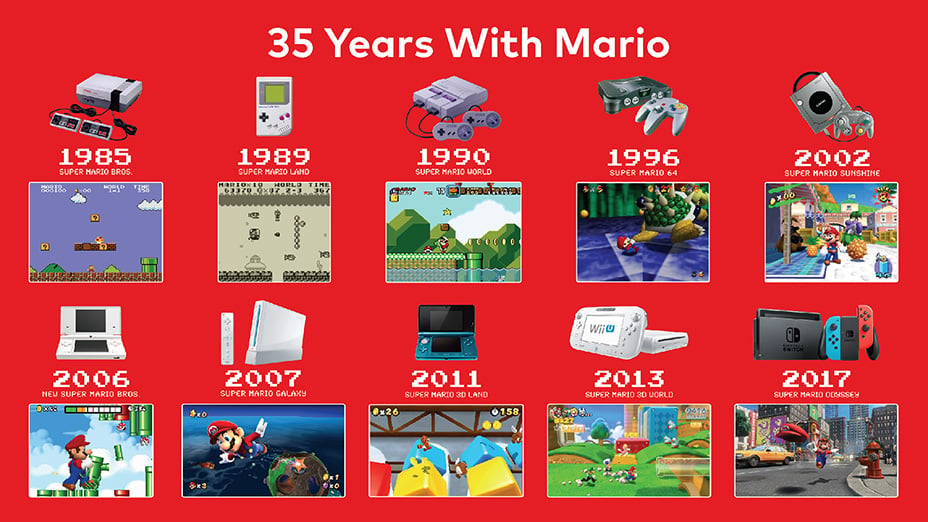

The company is unparalleled in possessing immensely strong intellectual property (IP) in the form of character franchises. The moustachioed Italian plumber, Mario, is an excellent example of Nintendo’s cross-generational appeal. The lovable tradesman has featured in over 200 games since his first appearance as ‘Jumpman’ in the Donkey Kong game released in 1981. Mario is also the best-selling video game franchise of all time, having sold more than half a billion copies worldwide. Other Nintendo games, The Legend of Zelda, Donkey Kong and Pokémon, add to this strong string of compelling franchises.

The best-selling video game franchises

Video game franchises with the most worldwide unit sales (as of 2021*)

*Or latest available. Tetris + physical sales and paid mobile downloads as of 2014.

Source: https://www.statista.com/chart/26129/best-selling-video-game-franchises/

Nintendo's characters emerge out of a unique entrepreneurial corporate culture. The company is known for its eccentricity and secrecy, partly due to its fiercely protected IP. A strong corporate culture that is a celebration of work and play, that encourages ‘idle chatter’ among employees is said to have helped produce this series of hits.

Nintendo also has a much better understanding of the whole process of brand-building than most competitors. Its family-friendly content lends itself to successful merchandising, which keeps the characters fresh, regardless of their 30-plus years on our screens and consoles. For instance, there is a Super Nintendo World amusement park in Osaka, and two more are being developed in the US.

Nintendo has also created a range of ‘toys-to-life’ merchandise (Amiibo) that consist of figurines that can affect gameplay when connected to consoles. There’s also a new animated Mario film slated for release next year. All of the above helps to reinforce brand loyalty and amass new users, particularly among younger generations. This creativity helps avoid the risk of Nintendo becoming a ‘nostalgia brand’, confined to a limited but loyal player base.

2. It operates within an industry enjoying growth

Over the last decade and a half, online gaming has grown from oddity to enormity. Cloud gaming or streaming may become equally commonplace, where users can play on multiple devices without localised computer processing power (ie without a console or gamer PC) as games are accessible remotely from the cloud.

This development may be the latest part in the progression of gaming from arcades, to PCs, to laptops, to phones. Just as videos went from VHS to DVD and then Netflix. This change could dramatically increase the user base as games become more immersive and engaging. Digital delivery would also allow the cheap back catalogue of games to be sold, creating a new source of profits for Nintendo. Greater connectivity and user engagement would ensure smoother earnings cycles through updates and add-ons.

There are questions as to whether this will make the industry less of a content oligopoly dominated by a few big companies. However, like the situation in music-streaming with Spotify, it appears to be far more favourable to the existing big brand players, like Nintendo. Its strong character franchises would help guarantee discovery (amid abundance of new content) and provide pricing power to negotiate better platform fees as distributors vie for access to the best characters.

There is also an argument that democratising access to content could kill the need for consoles. However, the raison d’etre of its proprietary hardware is not necessarily to generate additional revenue itself but, as Nintendo states, to be: “the most effective way of allowing our software to be played”. This suggests that an experimental approach to software is imbued within its creation of consoles and will likely lead to further complementary innovations.

The Switch console, its add-ons, the Ring Fit (which allows users to roleplay and exercise with its Pilates ring and leg strap) and the cardboard Labo (that allowed gamers to craft game kits) are examples of Nintendo’s ingenuity. Right now, deep in the Nintendo labs, engineers will be working hard on the next console intended to out-innovate the Switch – no mean feat, given it ranks as the company’s most successful console to date. The prospects for further success seem strong, which should result in substantial value creation.

Nintendo Switch extends lead over its predecessors

Lifetime unit sales of Nintendo's home video game consoles (as of 30 June 2022)

Source: https://www.statista.com/chart/12750/nintendo-home-console-sales/

Having navigated changes within the industry for over a century, we believe that Nintendo’s unrivalled and attractive portfolio of gaming characters will remain core to its competitive advantage and allow it to capitalise on the advent of changes to content delivery. This opportunity helps us to overlook short-term consensus concerns while also discounting additional upside from its cashed-up balance sheet and its attractive opportunity within China.

Risk factors

The views expressed should not be considered as advice or a recommendation to buy, sell or hold a particular investment. They reflect opinion and should not be taken as statements of fact nor should any reliance be placed on them when making investment decisions.

This communication was produced and approved in October 2022 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

Past performance is not a guide to future results. Changes in the investment strategies, contributions or withdrawals may materially alter the performance and results of the portfolio. All investment strategies have the potential for profit and loss.

This communication contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research, but is classified as advertising under Art 68 of the Financial Services Act (‘FinSA’) and Baillie Gifford and its staff may have dealt in the investments concerned.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this communication are for illustrative purposes only.

Important Information

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). Baillie Gifford & Co Limited is an Authorised Corporate Director of OEICs.

Baillie Gifford Overseas Limited provides investment management and advisory services to non-UK Professional/Institutional clients only. Baillie Gifford Overseas Limited is wholly owned by Baillie Gifford & Co. Baillie Gifford & Co and Baillie Gifford Overseas Limited are authorised and regulated by the FCA in the UK.

Persons resident or domiciled outside the UK should consult with their professional advisers as to whether they require any governmental or other consents in order to enable them to invest, and with their tax advisers for advice relevant to their own particular circumstances.

Financial Intermediaries

This communication is suitable for use of financial intermediaries. Financial intermediaries are solely responsible for any further distribution and Baillie Gifford takes no responsibility for the reliance on this document by any other person who did not receive this document directly from Baillie Gifford.

Europe

Baillie Gifford Investment Management (Europe) Limited provides investment management and advisory services to European (excluding UK) clients. It was incorporated in Ireland in May 2018. Baillie Gifford Investment Management (Europe) Limited is authorised by the Central Bank of Ireland as an AIFM under the AIFM Regulations and as a UCITS management company under the UCITS Regulation. Baillie Gifford Investment Management (Europe) Limited is also authorised in accordance with Regulation 7 of the AIFM Regulations, to provide management of portfolios of investments, including Individual Portfolio Management (‘IPM’) and Non-Core Services. Baillie Gifford Investment Management (Europe) Limited has been appointed as UCITS management company to the following UCITS umbrella company; Baillie Gifford Worldwide Funds plc. Through passporting it has established Baillie Gifford Investment Management (Europe) Limited (Frankfurt Branch) to market its investment management and advisory services and distribute Baillie Gifford Worldwide Funds plc in Germany. Similarly, it has established Baillie Gifford Investment Management (Europe) Limited (Amsterdam Branch) to market its investment management and advisory services and distribute Baillie Gifford Worldwide Funds plc in The Netherlands. Baillie Gifford Investment Management (Europe) Limited also has a representative office in Zurich, Switzerland pursuant to Art. 58 of the Federal Act on Financial Institutions (‘FinIA’). The representative office is authorised by the Swiss Financial Market Supervisory Authority (FINMA). The representative office does not constitute a branch and therefore does not have authority to commit Baillie Gifford Investment Management (Europe) Limited. Baillie Gifford Investment Management (Europe) Limited is a wholly owned subsidiary of Baillie Gifford Overseas Limited, which is wholly owned by Baillie Gifford & Co. Baillie Gifford Overseas Limited and Baillie Gifford & Co are authorised and regulated in the UK by the Financial Conduct Authority.

China

Baillie Gifford Investment Management (Shanghai) Limited

柏基投资管理(上海)有限公司(‘BGIMS’) is wholly owned by Baillie Gifford Overseas Limited and may provide investment research to the Baillie Gifford Group pursuant to applicable laws. BGIMS is incorporated in Shanghai in the People’s Republic of China (‘PRC’) as a wholly foreign-owned limited liability company with a unified social credit code of 91310000MA1FL6KQ30. BGIMS is a registered Private Fund Manager with the Asset Management Association of China (‘AMAC’) and manages private security investment fund in the PRC, with a registration code of P1071226.

Baillie Gifford Overseas Investment Fund Management (Shanghai)

Limited柏基海外投资基金管理(上海)有限公司(‘BGQS’) is a wholly owned subsidiary of BGIMS incorporated in Shanghai as a limited liability company with its unified social credit code of 91310000MA1FL7JFXQ. BGQS is a registered Private Fund Manager with AMAC with a registration code of P1071708. BGQS has been approved by Shanghai Municipal Financial Regulatory Bureau for the Qualified Domestic Limited Partners (QDLP) Pilot Program, under which it may raise funds from PRC investors for making overseas investments.

Hong Kong

Baillie Gifford Asia (Hong Kong) Limited 柏基亞洲(香港)有限公司 is wholly owned by Baillie Gifford Overseas Limited and holds a Type 1 and a Type 2 license from the Securities & Futures Commission of Hong Kong to market and distribute Baillie Gifford’s range of collective investment schemes to professional investors in Hong Kong. Baillie Gifford Asia (Hong Kong) Limited 柏基亞洲(香港)有限公司 can be contacted at Suites 2713–2715, Two International Finance Centre, 8 Finance Street, Central, Hong Kong. Telephone +852 3756 5700.

South Korea

Baillie Gifford Overseas Limited is licensed with the Financial Services Commission in South Korea as a cross border Discretionary Investment Manager and Non-discretionary Investment Adviser.

Japan

Mitsubishi UFJ Baillie Gifford Asset Management Limited (‘MUBGAM’) is a joint venture company between Mitsubishi UFJ Trust & Banking Corporation and Baillie Gifford Overseas Limited. MUBGAM is authorised and regulated by the Financial Conduct Authority.

Australia

Baillie Gifford Overseas Limited (ARBN 118 567 178) is registered as a foreign company under the Corporations Act 2001 (Cth) and holds Foreign Australian Financial Services Licence No 528911. This material is provided to you on the basis that you are a ‘wholesale client’ within the meaning of section 761G of the Corporations Act 2001 (Cth) (‘Corporations Act’). Please advise Baillie Gifford Overseas Limited immediately if you are not a wholesale client. In no circumstances may this material be made available to a ‘retail client’ within the meaning of section 761G of the Corporations Act.

This material contains general information only. It does not take into account any person’s objectives, financial situation or needs.

South Africa

Baillie Gifford Overseas Limited is registered as a Foreign Financial Services Provider with the Financial Sector Conduct Authority in South Africa.

North America

Baillie Gifford International LLC is wholly owned by Baillie Gifford Overseas Limited; it was formed in Delaware in 2005 and is registered with the SEC. It is the legal entity through which Baillie Gifford Overseas Limited provides client service and marketing functions in North America. Baillie Gifford Overseas Limited is registered with the SEC in the United States of America.

The Manager is not resident in Canada, its head office and principal place of business is in Edinburgh, Scotland. Baillie Gifford Overseas Limited is regulated in Canada as a portfolio manager and exempt market dealer with the Ontario Securities Commission ('OSC'). Its portfolio manager licence is currently passported into Alberta, Quebec, Saskatchewan, Manitoba and Newfoundland & Labrador whereas the exempt market dealer licence is passported across all Canadian provinces and territories. Baillie Gifford International LLC is regulated by the OSC as an exempt market and its licence is passported across all Canadian provinces and territories. Baillie Gifford Investment Management (Europe) Limited (‘BGE’) relies on the International Investment Fund Manager Exemption in the provinces of Ontario and Quebec.

Israel

Baillie Gifford Overseas is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755–1995 (the Advice Law) and does not carry

Ref: 27013 10014423