Key points

Transitions can be difficult, but recognising creative destruction is good for sustainable investment is an important step in finding the upcoming sustainable companies that will drive a more prosperous future.

All investment strategies have the potential for profit and loss, capital is at risk. Past performance is not a guide to future returns.

A revolution is on the horizon. Over the coming decades, our society needs to find ways to deliver prosperity in a sustainable and inclusive manner. This transition will have a profound impact on all industries. We believe that many incumbents will be challenged by this, creating opportunities for younger, innovative, and mission-driven companies to take their place. For investors, this presents an exciting opportunity to back growth businesses, contribute towards the transition to a sustainable future and generate attractive long-term investment returns.

The power of creative destruction

We believe that many incumbents will be structurally challenged by the transition towards a more sustainable future. For some, this is because their business models are based on fundamentally broken assumptions about the world. If a company is in the business of selling cheap, throw-away clothes, then being truly sustainable is going to hurt its bottom-line, because it means getting rid of everything it has been doing. For others, their past successes are now their Achilles’ heel. They are being held back by bureaucracy, legacy assets, vested interests and the demands of short-term shareholders. It’s a sad reflection of our industry that few incumbents can overcome those challenges and make a genuine positive impact on society. Instead, what we often see is management teams trying to cling on to their social license to operate by publishing glossy corporate social responsibility (CSR) reports, creating a few lines of ‘more sustainable’ products, while at the same time protecting and milking their legacy assets. If we are to move towards a more prosperous, sustainable and inclusive world, then our hope lies elsewhere.

Fortunately, there is another way. In Capitalism, Socialism, and Democracy (1942), Austrian economist Joseph Schumpeter coined the phrase “creative destruction” - a process that “revolutionises the economic structure from within, incessantly destroying the old one, incessantly creating a new one”. Creative Destruction is a fundamental part of capitalism where entrepreneurs upend legacy industries. Those entrepreneurs do not have abundant resources, but they are ambitious and willing to take risks. More importantly, they are more agile and innovative because they don’t have to worry about protecting legacy assets or upsetting vested interests. Free from the challenges that hold back incumbents, they are coming up with innovations that will contribute towards a better future: from electric vehicles to plant-based meat, from digital bank accounts to novel therapeutics. For the rest of the article, we will look at two companies doing just that: Coursera and Beyond Meat.

Coursera

Improving education is a pressing challenge. The cost of education has increased significantly above inflation in recent decades. For more and more people, especially those on low-incomes, good-quality education is becoming increasingly unaffordable. As access to education deteriorates, society’s accumulated human capital, people’s expected lifetime earnings and social mobility all decrease. One explanation for the escalating cost of education is Baumol’s cost disease. It argues that prices will rise for sectors that experience little or no increase in labour productivity but require to pay higher salaries to attract employees. This is likely the case for education. Compared to other sectors, the use of technology in education has been limited. The incumbents in the industry, textbook publishers and some for-profit education institutions, have failed to innovate. Instead, they have simply passed on the cost increases to students year after year.

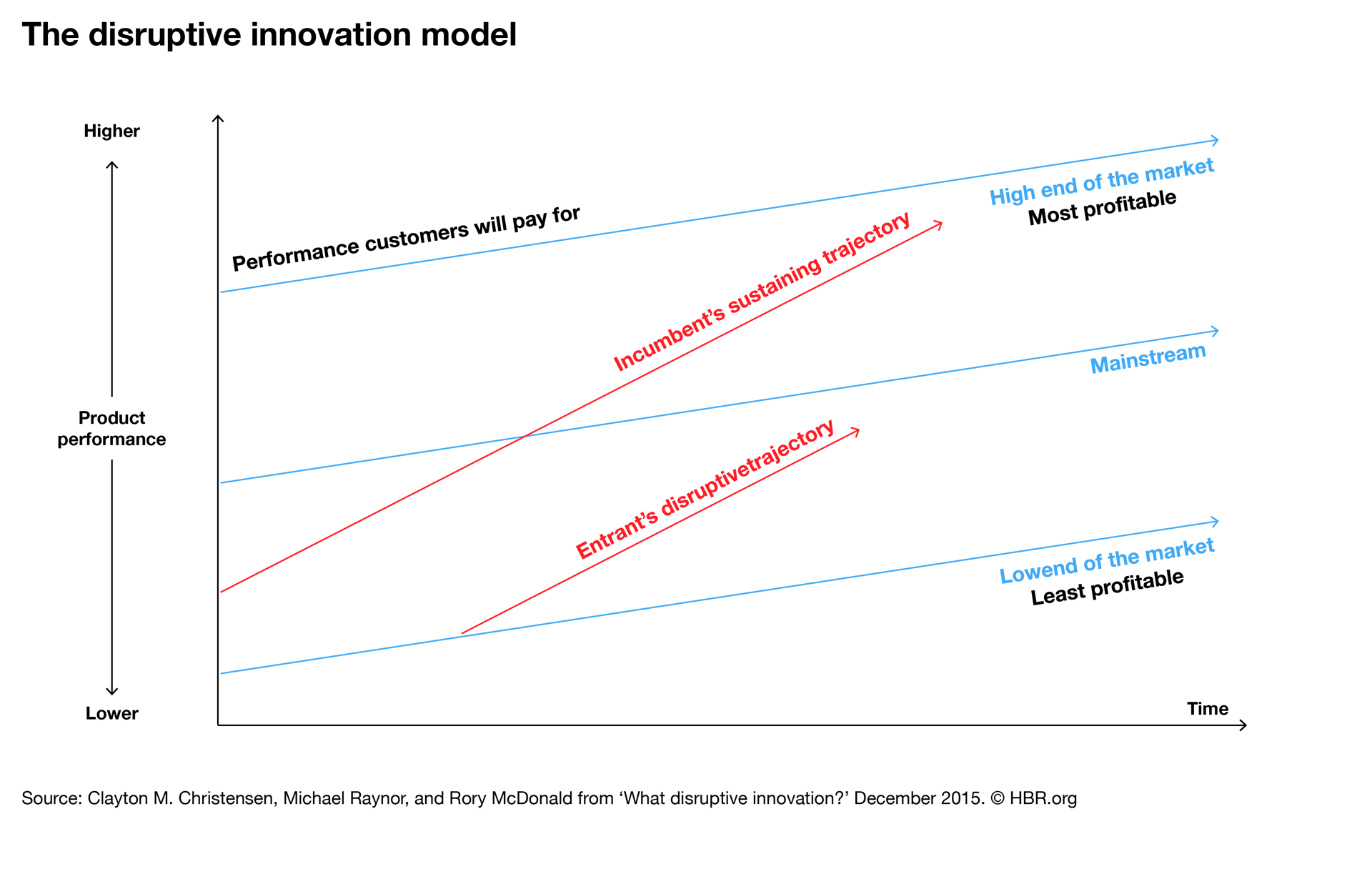

Coursera was founded with the ambition of democratising learning. By distributing learning contents online and enabling anyone to enrol, it aims to make education cheaper and more accessible. This model, known as Massive Open Online Courses (MOOCs), is not without criticisms, which include low completion rates and the bias towards affluent learners with access to IT. However, viewing Coursera purely as a MOOCs platform underestimates its long-term potential. In a way, Coursera is following the model of disruptive innovation proposed by the late Clayton Christensen. Christensen and his colleagues argued that when incumbents are occupied with serving the high end of the market with expensive products, they create an opportunity for newcomers to enter the market by serving the neglected customers, initially with a lower priced and lower performance product, which over time improves as the companies scale.

Coursera’s initial target audience consisted mainly of people who are interested in acquiring new knowledge or gaining skills to advance or switch their career. Historically, they had been underserved by incumbents in the education sector and had to rely on expensive textbooks, evening classes or instructor-led training. Coursera provided a cheaper and more accessible alternative. As the direct-to-consumers business scaled, Coursera was able to invest in adding more functionalities. Today, Coursera offers a range of contents and tools that satisfy the needs of different learners, from guided projects to specialisations, to online degrees.

One impressive aspect of Coursera is its ability to work with different stakeholders in the education ecosystem, including learners, universities, employers and governments. A good example of this is Coursera for Campus, where Coursera provides its contents to colleges and universities. Some of those institutions, in particular community and teaching colleges, are facing a myriad of challenges. Escalating cost of education has made their degrees more expensive, and the value of their degrees is diminishing due to changes to the job market from technology and automation. The result is a decline in enrolment and significant funding strains. In the US for example, enrolments to degree-granting institutions have fallen from a peak of 21 million in 2010 to just over 19 million in 2020[1] and the pandemic seems to be accelerating this trend. With Coursera for Campus, colleges and universities are able to strengthen their curriculums in a more cost-effective way by incorporating lectures and projects from leading universities and businesses. Additionally, because Coursera has job-relevant training from employers such as Google, Microsoft, and Salesforce, those hybrid degrees are able provide students with the relevant skills for a changing job market.

Beyond Meat

The livestock industry has many characteristics that make it ripe for disruption. It’s a tremendously inefficient industry. The US livestock industry converts 1,187 Pcal (1012 kcal) of feed into 83 Pcal of human edible proteins annually, an overall efficiency of merely seven per cent[2]. It is also a very concentrated industry, with the four largest companies controlling 85 per cent of the US beef market[3]. The combination of inefficiency and market concentration, which is often linked with price gauging behaviours, has resulted in a lack of innovation and a steady increase in prices for consumers. Since 2000, the price of ground beef in the US has risen by 167 per cent[4] compared to a 55 per cent cumulative increase in the Consumer Price Index[5]. At the same time, consumer tastes are changing. As the awareness of the environmental, health and animal welfare impact of meat consumption increases, more and more people are looking for alternatives.

Beyond Meat is one of the leading companies in the plant-based proteins category. The company’s insight is that the composition of meat is knowable and can be created using plant-derived ingredients rather than relying on the inefficient animal farming process. After years of research and development, Beyond Meat has created a range of products including burgers, sausages, mince and chicken nuggets that look, taste and smell just like their animal-derived counterparts. Whereas plant-based products have mainly targeted vegans and vegetarians in the past, Beyond Meat is looking to help meat-eaters consume more plant-based proteins. The company sees this as the area where it can have the greatest positive impact.

We believe that the incumbents like the meat packers are going to struggle in this transition. They have profitable legacy businesses to protect and they are being held back by vested interests in the system. A great example of this is when Tyson Foods released products that contained both animal and plant-based ingredients, satisfying its suppliers but not the consumers. The inability of incumbents to quickly adapt to changing consumer tastes will create opportunities for companies such as Beyond Meat. It’s still too early to say that Beyond Meat will definitely emerge as the winner in this transition, but given the size of the livestock market, if the company is successful, its impact on society and the financial returns for shareholders could be enormous.

Summary

We believe that entrepreneurs and innovative companies will play an important role in contributing towards a more sustainable future. On top of that, by disrupting slow-moving incumbents, they can create economic value for shareholders over the long term. This is risky and not all of them will succeed, but for those who are successful, the returns for society and shareholders could be enormous. As long-term investors, we believe that one of the most valuable activities we can do is to support those entrepreneurs and innovative companies in their mission to create a better future.

[1] National Center for Education Statistics (link)

[2] Energy and protein feed-to-food conversion efficiencies in the US and the potential food security gains from dietary changes; A. Shepon, G. Eshel, E. Noor and R. Milo. 2016

[3] Packers and Stockyards Division Annual Report 2019, USDA

[4] https://www.bls.gov/regions/mid-atlantic/data/averageretailfoodandenergyprices_usandmidwest_table.htm

Important information

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by theFinancial Conduct Authority (FCA). Baillie Gifford & Co Limited is an Authorised CorporateDirector of OEICs.

Baillie Gifford Overseas Limited provides investment management and advisory servicesto non-UK Professional/Institutional clients only. Baillie Gifford Overseas Limited is whollyowned by Baillie Gifford & Co. Baillie Gifford & Co and Baillie Gifford Overseas Limitedare authorised and regulated by the FCA in the UK.

Persons resident or domiciled outside the UK should consult with their professionaladvisers as to whether they require any governmental or other consents in order toenable them to invest, and with their tax advisers for advice relevant to their ownparticular circumstances.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this article are for illustrative purposes only.

Europe

Baillie Gifford Investment Management (Europe) Limited provides investment management and advisory services to European (excluding UK) clients. It was incorporated in Ireland in May 2018 and is authorised by the Central Bank of Ireland. Through its MiFID passport, it has established Baillie Gifford Investment Management (Europe) Limited(Frankfurt Branch) to market its investment management and advisory services and distribute Baillie Gifford Worldwide Funds plc in Germany. Similarly, it has established Baillie Gifford Investment Management (Europe) Limited (Amsterdam Branch) to market its investment management and advisory services and distribute Baillie Gifford Worldwide Funds plc in The Netherlands. Baillie Gifford Investment Management (Europe) Limited also has a representative office in Zurich, Switzerland pursuant to Art. 58 of the Federal Act on Financial Institutions ('FinIA'). It does not constitute a branch and therefore does not have authority to commit Baillie Gifford Investment Management (Europe) Limited. It is the intention to ask for the authorisation by the Swiss Financial Market Supervisory Authority (FINMA) to maintain this representative office of a foreign asset manager of collective assets in Switzerland pursuant to the applicable transitional provisions of FinIA. Baillie Gifford Investment Management (Europe) Limited is a wholly owned subsidiary of Baillie Gifford Overseas Limited, which is wholly owned by Baillie Gifford &Co.

China

Baillie Gifford Investment Management (Shanghai) Limited

柏基投资管理(上海)有限公司 (‘BGIMS’) is wholly owned by Baillie Gifford Overseas Limited and may provide investment research to the Baillie Gifford Group pursuant to applicable laws. BGIMS is incorporated in Shanghai in the People’s Republic of China (‘PRC’) as a wholly foreign-owned limited liability company with a unified social credit code of 91310000MA1FL6KQ30. BGIMS is a registered Private Fund Manager with the Asset Management Association of China (‘AMAC’) and manages private security investment fund in the PRC, with a registration code of P1071226.

Baillie Gifford Overseas Investment Fund Management (Shanghai) Limited

柏基海外投资基金管理(上海)有限公司 (‘BGQS’) is a wholly owned subsidiary of BGIMS incorporated in Shanghai as a limited liability company with its unified social credit code of 91310000MA1FL7JFXQ. BGQS is a registered Private Fund Manager with AMAC with a registration code of P1071708. BGQS has been approved by Shanghai Municipal Financial Regulatory Bureau for the Qualified Domestic Limited Partners (QDLP) Pilot Program, under which it may raise funds from PRC investors for making overseas investments.

Hong Kong

Baillie Gifford Asia (Hong Kong) Limited

柏基亞洲(香港)有限公司 is wholly owned by Baillie Gifford Overseas Limited and holds a Type 1 and a Type 2 license from the Securities & Futures Commission of Hong Kong to market and distribute Baillie Gifford's range of collective investment schemes to professional investors in Hong Kong. Baillie Gifford Asia (Hong Kong) Limited

柏基亞洲(香港)有限公司 can be contacted at Suites 2713–2715, Two International Finance Centre, 8 Finance Street, Central, Hong Kong. Telephone +852 3756 5700.

South Korea

Baillie Gifford Overseas Limited is licensed with the Financial Services Commission in South Korea as a cross border Discretionary Investment Manager and Non-discretionary Investment Adviser.

Japan

Mitsubishi UFJ Baillie Gifford Asset Management Limited ('MUBGAM') is a joint venture company between Mitsubishi UFJ Trust & Banking Corporation and Baillie Gifford Overseas Limited. MUBGAM is authorised and regulated by the Financial Conduct Authority.

Australia

Baillie Gifford Overseas Limited (ARBN 118 567 178) is registered as a foreign company under the Corporations Act 2001 (Cth) and holds Foreign Australian Financial Services Licence No 528911. This document is provided to you on the basis that you are a 'wholesale client' within the meaning of section 761G of the Corporations Act 2001 (Cth) ('Corporations Act'). Please advise Baillie Gifford Overseas Limited immediately if you are not a wholesale client. In no circumstances may this document be made available to a 'retail client' within the meaning of section 761G of the Corporations Act. This document contains general information only. It does not take into account any person's objectives, financial situation or needs.

South Africa

Baillie Gifford Overseas Limited is registered as a Foreign Financial Services Provider with the Financial Sector Conduct Authority in South Africa.

North America

Baillie Gifford International LLC is wholly owned by Baillie Gifford Overseas Limited; it was formed in Delaware in 2005 and is registered with the SEC. It is the legal entity through which Baillie Gifford Overseas Limited provides client service and marketing functions in North America. Baillie Gifford Overseas Limited is registered with the SEC in the United States of America.

The Manager is not resident in Canada, its head office and principal place of business is in Edinburgh, Scotland. Baillie Gifford Overseas Limited is regulated in Canada as a portfolio manager and exempt market dealer with the Ontario Securities Commission ('OSC'). Its portfolio manager licence is currently passported into Alberta, Quebec, Saskatchewan, Manitoba and Newfoundland & Labrador whereas the exempt market dealer licence is passported across all Canadian provinces and territories. Baillie Gifford International LLC is regulated by the OSC as an exempt market and its licence is passported across all Canadian provinces and territories. Baillie Gifford Investment Management (Europe) Limited ('BGE') relies on the International Investment Fund Manager Exemption in the provinces of Ontario and Quebec.

Oman

Baillie Gifford Overseas Limited ('BGO') neither has a registered business presence nor a representative office in Oman and does not undertake banking business or provide financial services in Oman. Consequently, BGO is not regulated by either the Central Bank of Oman or Oman's Capital Market Authority. No authorization, licence or approval has been received from the Capital Market Authority of Oman or any other regulatory authority in Oman, to provide such advice or service within Oman. BGO does not solicit business in Oman and does not market, offer, sell or distribute any financial or investment products or services in Oman and no subscription to any securities, products or financial services may or will be consummated within Oman. The recipient of this document represents that it is a financial institution or a sophisticated investor (as described in Article 139 of the Executive Regulations of the Capital Market Law) and that its officers/employees have such experience in business and financial matters that they are capable of evaluating the merits and risks of investments.

Qatar

The materials contained herein are not intended to constitute an offer or provision of investment management, investment and advisory services or other financial services under the laws of Qatar. The services have not been and will not be authorised by the Qatar Financial Markets Authority, the Qatar Financial Centre Regulatory Authority or the Qatar Central Bank in accordance with their regulations or any other regulations in Qatar.

Israel

Baillie Gifford Overseas is not licensed under Israel's Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755–1995 (the Advice Law) and does not carry insurance pursuant to the Advice Law. This document is only intended for those categories of Israeli residents who are qualified clients listed on the First Addendum to the Advice Law.

14251 10006041