Key points

- Higher oil prices can ripple through emerging markets via currencies, inflation and interest rates

- That can create resilience in places such as Brazil, while leaving oil importers like India more vulnerable

- For our clients, the opportunity may sit not only in energy producers but in the wider businesses shaped by energy security

As with any investment, your capital is at risk.

We’re highly sceptical about the certainty in tone of some market commentary about the conflict in the Middle East. You’ll be pleased, I hope, that this isn’t another ‘What happens next?’ article.

But when the viability of the key global shipping route for oil and gas comes into question, then it’s important that we lay out what the less secure energy backdrop might mean for our clients’ portfolio.

The first-order implications are relatively straightforward: oil producers see stronger realised prices and better cash generation, and in periods like this they can also be treated by the market (and governments) as even more strategically important assets than they already were. As you know, we do have exposure to traditional energy businesses in the portfolio, and we have also been spending time thinking about new energy ideas.

But what also matters to us in each case is the quality of the asset base, the strength of the balance sheet and the scope for operational progress. Petrobras, the Brazilian oil major, is a good example, where the appeal is about the rising asset quality, and the production growth possible over the long term. Its recent results showed production growth of 11 percent year-on-year, which is higher than we’ve seen for some time.

The second-order implications for the portfolio are much broader and potentially more impactful: the impact of higher oil prices on countries’ external balances will show up in currencies, inflation and the path of interest rates. Our understanding of the portfolio’s actual energy position has also been informed by our analytics team's work on the portfolio’s oil sensitivity.

We need to think about energy exposure more broadly than the sector line alone. Some of the exposure in our clients’ portfolio is direct, but a good deal of it sits in the shape of the portfolio, especially through the overweight position in certain Latin American countries, like Brazil, on one side, and your large underweight to India on the other.

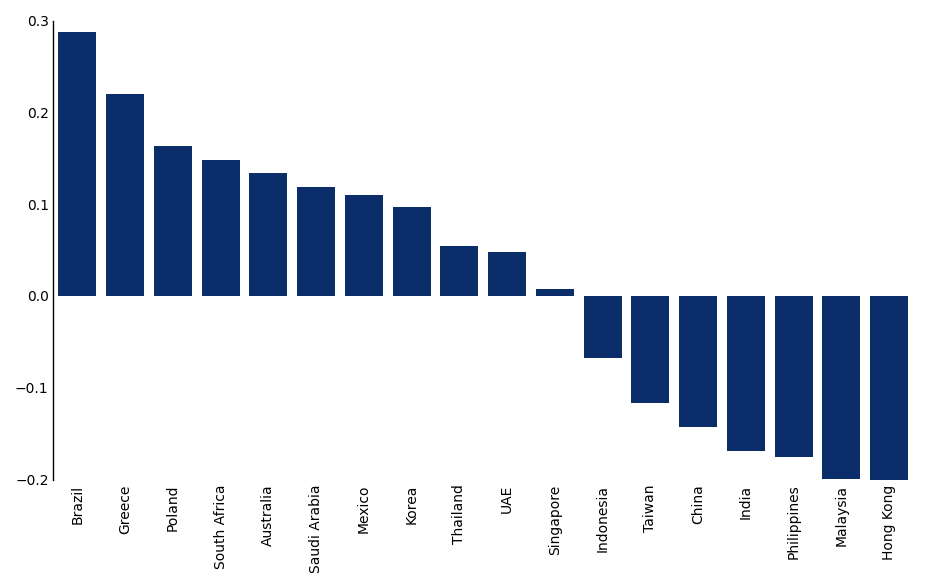

The chart below helps illustrate this. It shows how different emerging markets have historically moved with changes in the oil price. A positive reading indicates that returns have tended to rise alongside oil prices, while a negative reading suggests the opposite.

Emerging markets: correlation with oil price

Monthly outperformance vs MSCI EM index correlated with Brent crude since 2011.

Source: Peramunetilleke, Desh, et al. EM: War, Oil, and Momentum Unwind. Jefferies Equity Research, 12 March 2026, FactSet

Starting with Brazil, which is the largest overweight country in our clients’ portfolio. Brazil’s oil story is anchored in large, low-cost resources outside the Gulf chokepoint. Oil is already Brazil’s largest export (c. 13 percent of total exports) so higher oil can reinforce a stronger macro backdrop for a wider set of domestic businesses, and the relevant sensitivity is not confined to the companies that sit in the energy bucket.

Petrobras is one of the more obvious direct beneficiaries when oil moves higher, but the more interesting point sits one layer further out. Its related royalties and taxes account for roughly 10 percent of Brazilian fiscal revenue. That can improve confidence in the fiscal outlook and reduce pressure on longer-term interest rates.

It is through those channels that the effects begin to reach a broader set of businesses, including B3, Axia Energia and Bradesco. Obviously, none of these companies sit in the energy sector, yet all can benefit from stronger oil through improved credit conditions and a more supportive domestic backdrop. While we have reduced Petrobras in recent quarters, the proceeds have largely moved into these domestic Brazilian names that should benefit in this environment.

India is the mirror image, as the country is one of the largest oil importers in the world, importing roughly 85 percent of its crude. When oil stays high, the effects tend to spread quite quickly through the economy. Borrowing conditions can tighten and higher input costs can squeeze company margins. In that context, our underweight to India is helpful if oil remains elevated. We will watch how quickly the impact of high oil prices gets ‘priced in’ to the Indian equity market: might this give us opportunities?

The picture is not entirely one-dimensional though when we look at various businesses in India, and Reliance Industries’ oil refinery business is a good example of why. A refiner is not automatically hurt by a higher oil price. What matters is whether products like diesel, petrol and jet fuel rise by more than the crude used to make them. When that happens, refining margins can actually strengthen, which perhaps even gives parts of Reliance’s refinery business some protection even as higher oil remains a broader headwind for India.

What about China? As an oil importer, it too could feel the effects of higher oil and tighter liquefied natural gas (LNG) markets, but it also comes into this period with more buffers than many of its Asian peers. Domestic petroleum and liquids production reached 5.3 million barrels a day last year. Broader crude inventories are now estimated to be well above 1 billion barrels.

Moreover, China has the most diversified energy mix in the world. It has spent years building alternatives to imported oil and gas, and those alternatives are now large enough to matter in a shock. Over 2023–2024 it more than doubled installed solar capacity, added record wind capacity and accelerated electrification in transport through electric vehicle (EV) adoption, which is now the highest penetration rate in the world.

The result is that crude oil only made up around a fifth of China’s total energy consumption in 2024. That does not make China immune, but it does suggest a degree of resilience. In our view, China looks better placed than much of the region to absorb an energy shock, even if the headlines imply otherwise.

Our clients' portfolio invests in CATL, the Chinese battery manufacturer. While classified as an industrial, we would argue it is one of the most important energy exposures in the portfolio. It sits at the centre of the energy transition, spanning both electric vehicles and, increasingly, energy storage.

This segment now accounts for roughly a fifth of revenues, up from negligible levels five years ago, yet remains underappreciated by the market.

There is a conceivable possibility that oil is higher for a prolonged period of time. If we do see sustained triple-digit oil prices, then it’s likely we’d make broader positioning changes. As you’d expect, this is a key source of debate in the team. We are careful to lean on a wide range of resources to help us here, including energy analysts and, perhaps more importantly, political analysts too.

We have also been thinking about what opportunities may emerge from this environment beyond energy names. A less secure energy backdrop often prompts a broader infrastructure response. Countries place greater value on storage, grid resilience, and, in some cases, nuclear, because the priority shifts from simply securing supply at the lowest cost to securing supply that is reliable and resilient.

These responses usually require large amounts of physical buildout. The beneficiaries may therefore include not only producers, but also some of the companies involved in designing, constructing and equipping that infrastructure, including selected Korean engineering and construction businesses. If energy security becomes more firmly embedded as a policy priority, some of the eventual winners may sit further along the value chain.

Overall, while we are cautious on the geopolitics, we are clear on the portfolio logic. Some parts of the portfolio may be helped by this environment, while others are more exposed to it. We are not trying to predict every turn in the Middle East. Instead, we are focused on what a more uncertain energy backdrop means for our clients’ portfolio as a whole. An important part of that is recognising that energy exposure sits in more places than the sector line alone suggests.

We are also thinking carefully about a more inflationary world, where we think the financial characteristics of portfolio companies (notably their balance sheet strength) will be vital. Investing in emerging markets is never straightforward, and recent events have been yet another reminder of that. Power comes not from near term prediction, but from how well the portfolio is built for growth and to withstand shocks.

Risk factors

The views expressed should not be considered as advice or a recommendation to buy, sell or hold a particular investment. They reflect opinion and should not be taken as statements of fact nor should any reliance be placed on them when making investment decisions.

This communication was produced and approved in March 2026 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

Potential for Profit and Loss

All investment strategies have the potential for profit and loss, your or your clients’ capital may be at risk. Past performance is not a guide to future returns.

This communication contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research, but is classified as advertising under Art 68 of the Financial Services Act (‘FinSA’) and Baillie Gifford and its staff may have dealt in the investments concerned.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this communication are for illustrative purposes only.

191631 10062026