Overview

The Global Alpha Team shares insights on Q4 2025, covering the strategy's recent performance, portfolio adjustments, and market influences.

As with any investment, your capital is at risk.

Global Alpha delivered strong returns over 2025, founded on great businesses delivering growth, but did not keep pace with global indices. The valuation of the portfolio has barely moved over the course of 2025. As measured by multiples of expected profits, Global Alpha costs the same as it did at the start of the year, even after delivering good absolute returns.

While global indices delivered even higher returns in 2025, they continued to be supported by rising valuations, not just earnings growth. Global Alpha has grown its earnings faster than the index for each of the past three years, but this strong earnings growth has yet to be rewarded.

In 2025, Global Alpha’s finance-focused holdings didn’t keep up with strong returns from banks (which we don’t have any of in the portfolio). Our semiconductor manufacturing businesses were left behind by markets, while the reshaping of our healthcare holdings has not yet delivered better outcomes. Overall, strong individual contributions from a variety of holdings (from European budget airlines to algorithmic advertising) weren’t enough to overhaul market returns.

It feels a little like ordering carefully at the restaurant, picking a balance of flavours and textures through the courses. And feeling rather deflated when a flaming soufflé is paraded through the dining room and delivered to the table right next to us. It doesn’t make any direct difference to what we’ve been served. But, all puffed up and attracting admiring glances, the soufflé next door is what we, and you, could have been served last year.

We’re acutely aware that 2025 adds to an unhelpful run of underperformance that stretches back to the fallout from the Covid pandemic. A valuation headwind can only persist for so long, and by maintaining our growth standards, the portfolio is well-positioned to deliver significantly better returns to patient investors.

This letter explores why the portfolio’s blend of growth, quality, and modest valuation means substance, not hot air, will support future returns.

Portfolio Characteristics

The most important thing we can do is to continue to seek out and own underappreciated growth businesses. We recognised a few years ago that we needed to broaden the range of growth drivers in the portfolio. This broadening is intended to rein in the way the overall portfolio behaves by delivering better balance across the strategy’s three growth profiles (Disrupters, Compounders and Capital Allocators). Our progress on both fronts is evident in the portfolio’s characteristics. There are still areas to work on, of course. Continual improvement should be central to any effective portfolio construction approach.

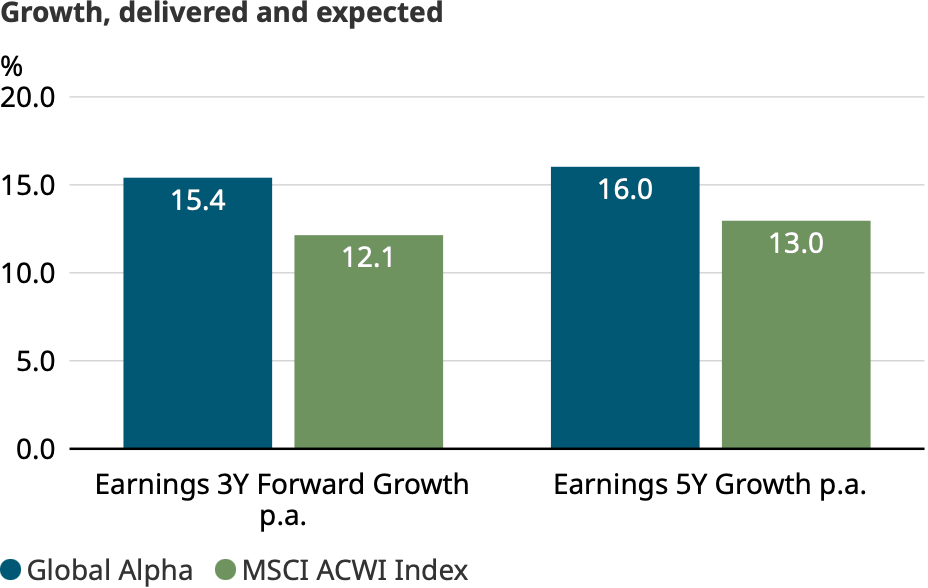

Crucially, growth has come through, and more is expected. At the same time, resilience has improved. An expected earnings growth rate of 15.4 per cent per year for Global Alpha might not sound vastly different to the MSCI ACWI index’s expected 12.1 per cent each year, but this adds up to a meaningfully different outcome over our investment time horizon. These market consensus figures contain what we believe are conservative estimates for the businesses we own. If only those expectations were delivered over the next five years, then we’d see profits up by more than 100% for Global Alpha against an index rise of 77 per cent. That’s a difference worth capturing.

Source: Baillie Gifford

It's natural to ask how much you should pay for that superior growth. Finding and owning companies with more earnings growth is only valuable if the market underappreciates them. Our insights land in two places. We are willing to make growth predictions that differ significantly from market expectations when we find sufficient evidence to support them. Second, we’re willing to factor in the implications of that growth potential for longer time horizons than stock markets generally accommodate.

Source: Baillie Gifford

Following three years of relative valuation falls, the Global Alpha portfolio is under 15% more expensive than the MSCI ACWI index based on multiples of expected earnings. For those who tend to reach for their calculators at this point, if we used the market earnings expectations above, then Global Alpha would be at the same valuation as the index inside 5 years. This is an unusually low premium, and close to the lowest it has ever been in Global Alpha’s history. And that’s before we even factor in our own views of growth at each company, which is really where the value of our insight lies.

Finally, we have written a lot about the quality and resilience of the portfolio in recent letters. This is evident in the superior gross margins, the lower reliance on debt and the shift towards profitability across the portfolio. All holdings are now profitable as we, and the companies we own, have shifted gears to deliver growth with cost control more effectively.

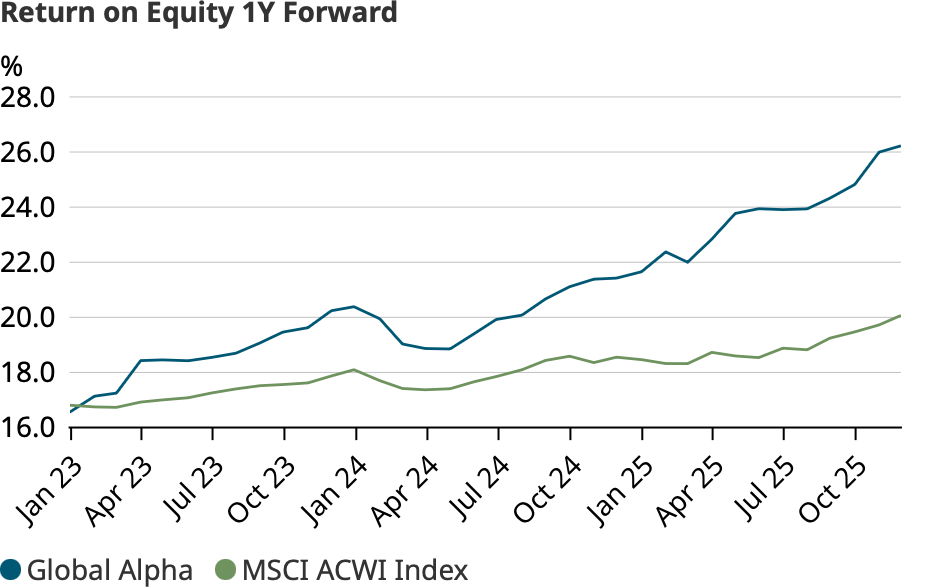

The return on equity profile (i.e., the amount of profit the portfolio’s companies generate from each dollar of shareholders’ capital) has advanced materially ahead of the index. This is as strong an indicator of improvement as we can think of. Our companies are becoming more profitable and are using capital more efficiently as they grow. This bodes well for future growth. Rather than growth being a strain for companies to cope with, it is acting as an unlock for future expansion.

The best of the opportunities ahead

We continue to build our understanding of, and conviction in, the AI phenomenon. We have no doubt that this will be a revolutionary technology, while being mindful that it could be deployed in many different ways across society. We are convinced that there are several players in the infrastructure supply chain that are well placed to benefit, either because of their position in the network or their dominance in a hard-to-replicate niche. We will keep adjusting our views as new information emerges. In the past quarter, we added to Alphabet, Google’s parent company, as evidence of a cost advantage from its internal chip development is now accumulating. We have reduced our holding in Meta, the US social media giant behind Facebook, Instagram and WhatsApp. Our view that Meta’s early and aggressive investment in AI would improve its core business has been right so far, but this perspective is not as differentiated as it was two years ago.

Source: Baillie Gifford

We own several other businesses in the hardware supply chain, most notably via large positions in NVIDIA and TSMC. When we consider the many ways that AI could develop from here, most roads lead to the Taiwanese semiconductor foundry TSMC. It now captures 70 per cent of global foundry revenues, with even higher market shares in the highest performance chips, due to its relentless pursuit of manufacturing scale and expertise. Our ownership of companies monetising AI effectively remains at an earlier stage and is a priority for further work in the year ahead. We have expanded on this important area in our Research Agenda 2025 review here: Global Alpha Research Agenda Review 2025: AI.

Our view of healthcare opportunities differs significantly from that of stock markets, where sentiment appears to have been worn down by a tough few years. Our enthusiasm for this area is high and rising, as we describe in more detail here: Global Alpha Research Agenda 2025 Review: Healthcare Evolution. During the final few months of the year, we added to our long-standing position in Thermo Fisher, a leading equipment provider to research and clinical laboratories. And we took a holding at the first opportunity in Medline by participating in its IPO for clients who were able to do so in December. Medline is one of the largest providers of medical supplies in the US, and it has an unmatched distribution network that combines with its own product manufacturing to create a powerful competitive position. It is a highly reliable distributor and, in an industry where surety of supply matters, there is a compelling basis for it to grow by taking market share for years. These purchases continue a deliberate evolution that tilts towards the broader beneficiaries of healthcare spending and innovation over individual drug candidate developers.

Our holdings in Emerging Markets point to another source of differentiation. This is our largest regional overweight compared to the index and is part of the market that Western investors often misunderstand. While we operate primarily from one office in Edinburgh, we work hard to understand Emerging Markets businesses from the local perspective of their customers. To paraphrase one of Scotland’s most famous sons, “to see the world as others see it”.

Portfolio manager Mike Taylor’s travel in South America in 2025 is one example. His work, in combination with insights from our trusted advisors, helped us add to both the Brazilian online bank Nu Holdings and the pan-regional ecommerce platform MercadoLibre. We view both as world-class operators. Nu Holdings is disrupting incumbent banks that overcharge their customers by offering a materially better deal online. Our conviction in Nu’s ability to expand well beyond its current base of 100 million customers is growing.

MercadoLibre’s shares have been weak in the second part of the year. It is investing heavily in future growth by lowering free shipping thresholds, raising marketing spending and accelerating credit growth. Our enthusiasm for the long-term growth potential this brings sits at odds with the seemingly short-term concerns of the stock market. Having trimmed the holding in the first part of the year, we are now adding again. You can read more about the case for EM here: Global Alpha Research Agenda Review 2025: Emerging consumers.

When to act

Our investment edge requires us to look past short-term market moves, but we look closely at outcomes that diverge from our expectations. There are two features to draw your attention to in particular.

Our holdings in financial services businesses were poorly positioned for 2025. It’s been a struggle on both sides of the coin. We own no traditional banks in the portfolio, and banks in several developed markets enjoyed valuation rises through the year. This has been a large enough move to have a material impact on relative returns. At the same time, some of the financial businesses we own have weighed on returns. Both the meal voucher provider Edenred and the US finance platform Block have had difficult spells.

Edenred has faced regulatory concerns in some of its key markets, where vouchers form an important part of worker compensation. We believe that Edenred will be able to navigate regulations effectively and that its scale will provide it with powerful advantages over the competition.

Block’s Square business helps merchants to collect and process payments, while its CashApp consumer finance platform provides simple financial tools that could graduate into a genuine alternative to conventional banking. Cost control issues and an uncertain consumer spending backdrop dented the share price over the course of 2025. We own Block for the exciting opportunity it has to scale both sides of its business. In our most optimistic return scenarios, Block could scale both to a point that would allow them to combine them into a system that does not need to pay for access to traditional payments infrastructure.

Financial companies always come with external risks, but we prefer businesses with growth that falls under their control. Outside of traditional finance, several of our ecommerce platforms, such as Shopify, MercadoLibre and Sea Ltd., are developing meaningful companion payment and consumer finance businesses that we think can grow profitably for years. It’s never pleasant being on the wrong side of share price returns, but a closer look at our financial exposures only serves to deepen our conviction in what we’ve chosen to own.

On the other hand, we have taken steps to improve the Compounders part of our portfolio. We own these businesses for their ability to consistently outgrow the market for a very long time. Over several years, this compounds into a growth profile that is far superior to the market. We weight the durability and reliability of growth heavily in our investment cases. We can accommodate lower absolute rates of growth in these holdings because they provide an important additional feature. They are steadier businesses, holdings that provide an anchor in stormier market conditions.

Some of our Compounder holdings have not delivered the reliability we seek, and we upgraded this part of the portfolio during 2025 with additions such as the US discount store Dollar General, the British maker of tabletop strategy games, Games Workshop, and the Japanese factory automation business Keyence. These, and other additions, are helping to bring the features we seek into the heart of the strategy. At the same time, there is still more that we could add to improve the overall balance of risk and return. 2026 may be a particularly fruitful year to search for more of these businesses. Our starting contention is that some of these steady businesses have been left behind by market rises, giving us a rare opportunity to bring in dependable growth at undemanding valuations.

Conclusion

We know how hard it is to see another year of underperformance added to the record, regardless of the absolute level of return. We are grateful for your patience during this challenging period. Successful long-term investing is a partnership, and we can only aim for long-term returns by retaining your support through the difficult moments as well as the good ones. Long-term returns are never delivered smoothly, but we recognise that we have tested the outer bounds in this respect. At the same time, the share price outcomes from the portfolio have been out of step with fundamental progress for some time now, making the opportunity for future returns unusually compelling.

We enter 2026 with a collection of tremendous businesses in the portfolio. They are growing quickly from strong financial and operating positions. We have widened the foundations of the portfolio and driven up quality. Our long-term growth investment philosophy is undimmed and is evident in the holdings that have reached the bar for inclusion in the portfolio in recent months.

Crucially, these attractive features have drawn little recognition in share price terms. The valuation gap between Global Alpha and the benchmark index is near historic lows. This feature is unlikely to last, given the strength of what we own. We are in a fantastic position to repay your support of the strategy.

Annual past performance to 31 December each year (%)

| 2021 | 2022 | 2023 | 2024 | 2025 | |

| Global Alpha Composite (gross) | 8.0 | -28.6 | 20.3 | 11.9 | 18.6 |

| Global Alpha Composite (net) | 7.3 | -29.1 | 19.5 | 11.1 | 17.9 |

| MSCI ACWI | 19.0 | -18.0 | 22.8 | 18.0 | 22.9 |

Annualised returns to 31 December 2025 (%)

| 1 year | 5 years | 10 years | |

| Global Alpha Composite (gross) | 18.6 | 4.2 | 11.3 |

| Global Alpha Composite (net) | 17.9 | 3.6 | 10.6 |

| MSCI ACWI | 22.9 | 11.7 | 12.3 |

Source: Baillie Gifford, MSCI. US dollars. Returns have been calculated by reducing the gross return by the highest annual management fee for the composite. 1 year figures are not annualised.

Past performance is not a guide to future returns.

Legal notice: MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, endorsed, reviewed or produced by MSCI. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Risk factors

This communication was produced and approved in January 2026 and has not been updated subsequently. It represents views held at the time and may not reflect current thinking.

The views expressed should not be considered as advice or a recommendation to buy, sell or hold a particular investment. They reflect opinion and should not be taken as statements of fact nor should any reliance be placed on them when making investment decisions.

This communication contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research, but is classified as advertising under Art 68 of the Financial Services Act (‘FinSA’) and Baillie Gifford and its staff may have dealt in the investments concerned.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this communication are for illustrative purposes only.

Important Information

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). Baillie Gifford & Co Limited is an Authorised Corporate Director of OEICs.

Baillie Gifford Overseas Limited provides investment management and advisory services to non-UK Professional/Institutional clients only. Baillie Gifford Overseas Limited is wholly owned by Baillie Gifford & Co. Baillie Gifford & Co and Baillie Gifford Overseas Limited are authorised and regulated by the FCA in the UK.

Persons resident or domiciled outside the UK should consult with their professional advisers as to whether they require any governmental or other consents in order to enable them to invest, and with their tax advisers for advice relevant to their own particular circumstances.

Financial Intermediaries

This communication is suitable for use of financial intermediaries. Financial intermediaries are solely responsible for any further distribution and Baillie Gifford takes no responsibility for the reliance on this document by any other person who did not receive this document directly from Baillie Gifford.

184308 10059574