Painted tiles in Badajoz, Spain, depicting Hernán Cortes and his burning ships in 1519

As with any investment, your capital is at risk.

Is there an AI bubble? Recent warnings from JPMorgan chief executive Jamie Dimon, central banks and technology executives themselves suggest there could be, and that the risk of it bursting is on many minds.

Today, a mix of macroeconomic uncertainty, high valuations and speculative investment seems toxic. Are we on the precipice of disaster? Or is the world about to embark on an unprecedented era of soaring productivity? Moreover, how should we, as capital allocators, act?

The dilemma calls to mind the story of the Spanish explorer Hernán Cortés. Legend has it that when Cortés arrived near modern-day Veracruz, Mexico in 1519, he burned his ships so his men would know there was no retreat. He was all in. Should investors do the same with AI? Or sail back to safety?

Two tests for a bubble

Before asking whether there is a bubble, it helps to define one. History offers multiple examples, including the dotcom bubble, railways, tulips and gold rushes.

Two conditions must be met:

- Excessively speculative investment beyond reasonable expectation of return

- Insensible valuations

Let’s look at the first condition. Put differently, this is when the supply of goods runs well ahead of current demand.

Consider the dotcom boom-and-bust of the late 1990s. Companies laid mile after mile of fibre optic cable – far too much, far too quickly. Utilisation was estimated at about 5 per cent. Simultaneously, investors valued companies without profits, revenues or even business models on eyeballs alone.

Is there a parallel today? I’d suggest not.

The amounts that the massive cloud service providers we now call ‘hyperscalers’ are spending are large. But what is remarkable is where the money comes from, not the sums themselves.

At the time of writing, the hyperscalers were on track to have spent about $200bn on AI-related capital expenditure within the US in 2025. That’s roughly 0.7 per cent of the country’s GDP.

In previous infrastructure booms, the figures involved were much higher. When the UK built railway infrastructure in the 19th century, spending reached 7 per cent of GDP. The US spent more building out highways postwar.

What stands out is that this time, the investment is coming from just a few large companies, not the amount itself.

Even if spend on supply is reasonable in an infrastructure context, could it be argued that it outstrips current demand? There is little evidence. Currently, the limiting factor is the supply of chips. NVIDIA and TSMC cannot make enough to meet demand, even as each new generation of processors delivers more performance per dollar.

We also know the chips are being used. The frontier AI lab Anthropic, which is responsible for the large language model Claude, is one of the fastest-growing software businesses ever.

Insensible valuations

What about the second condition for a bubble – that of insensible valuations?

The AI sector contains diverse businesses. There are probably pockets of excess. But valuations for major AI companies are far from insensible.

NVIDIA trades on 25 times forward earnings – ie its share price is 25 times its expected profits per share over the coming year, based on analysts’ consensus forecasts

Costco, the US bulk goods retailer, commands 42 times. NVIDIA’s valuation is only cheap if profitability holds, but that is the point. The valuation predicts a marked slowdown in profit growth. Hardly a frenzy.

The key is to remember the long-term reality of the situation today. Spending on AI is not unusual in terms of amounts. Demand is real, and enormous – and this is at a very early point in the technology’s development. At the same time, valuations for the key companies involved are not unreasonable.

Where the real excess may be

So there is no bubble? Not necessarily. But it might not be in AI. If anything, the froth looks less concentrated in AI than in the supposedly safe parts of the market.

Since 2022, the S&P 500 has re-rated upward to levels well above long-run averages, despite rising interest rates. Perhaps growth justifies this? Not at all.

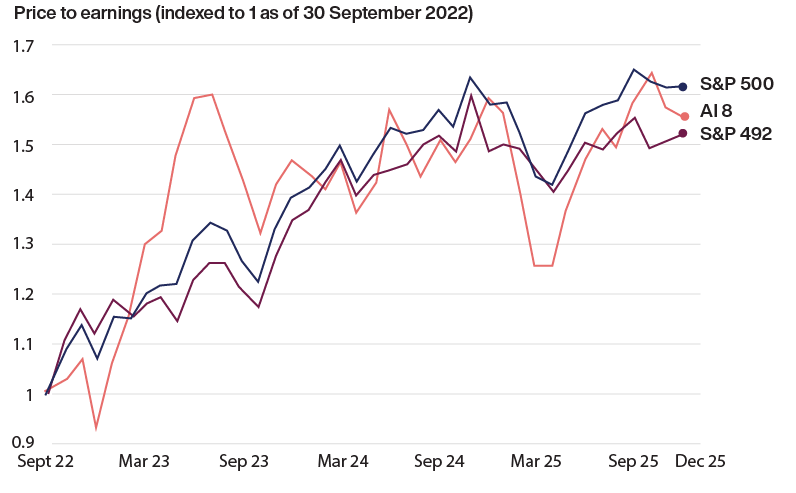

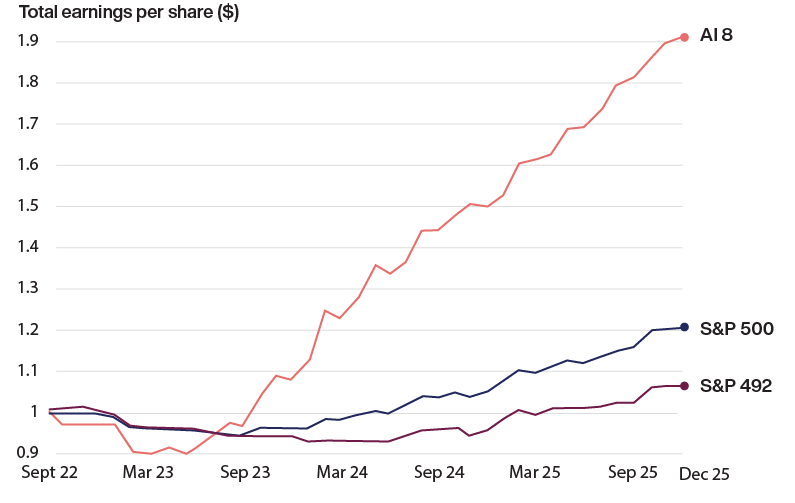

Valuations have risen strongly

Earnings growth for the ‘AI 8’ – Microsoft, Broadcom, Google and others – has been terrific. For everything else, growth has been pedestrian. Analysis suggests growth in gross profits is about as bad as it has been for the median US company going back to the 1980s.

AI earnings are pulling decisively ahead of the wider market

Source: Baillie Gifford & Co, S&P, Revolution. USD. As at September 2025.

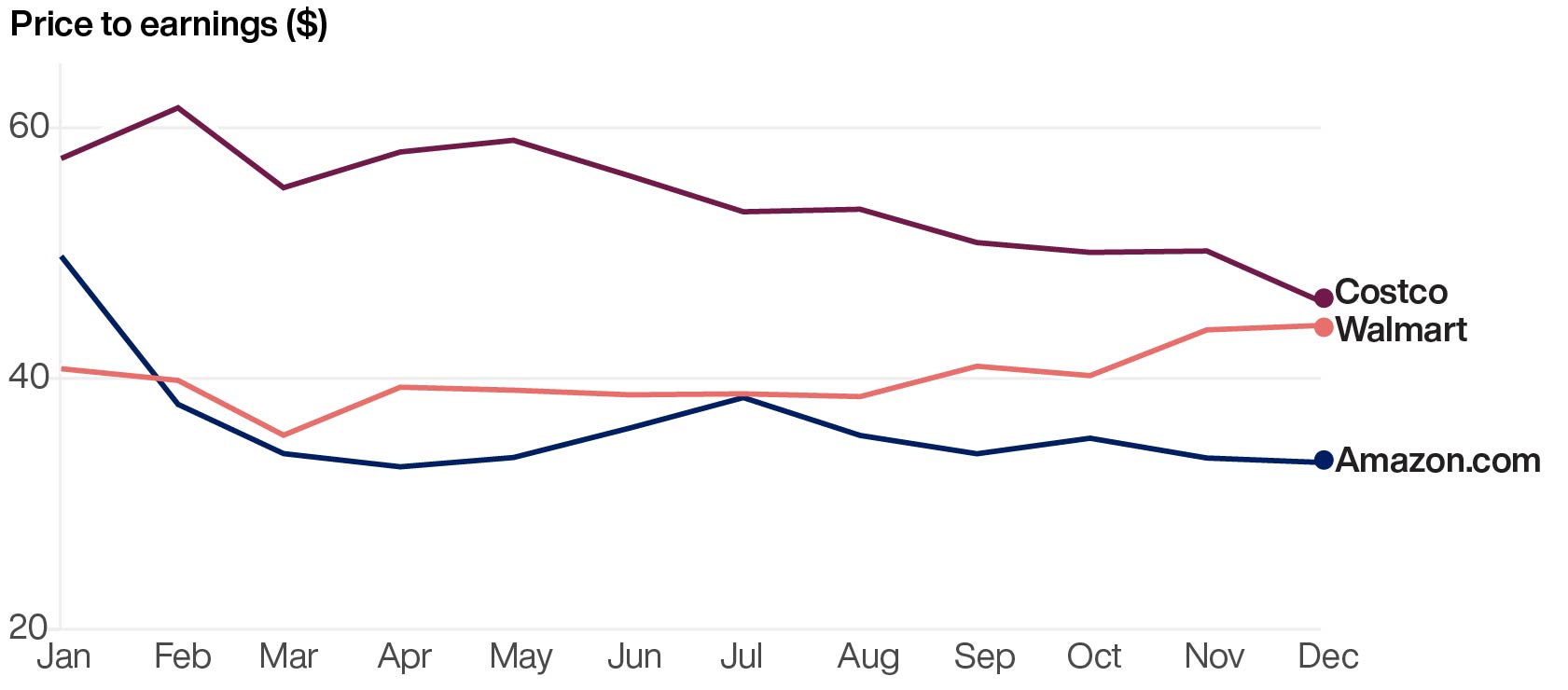

This brings us back to bulk retailer Costco. Let’s rank its valuation multiple and its expected year-over-year growth in profit-per-share for fiscal year 2027 against those of the retailer Walmart and hyperscaler Amazon:

- Costco – is forecast to grow just under 10 per cent

- Walmart – its profit-per-share growth is forecast to grow 12 per cent

- Amazon, with a profit-per-share forecast to grow 22 per cent

Yet, as of 31 December 2025:

- Costco was trading at about a 46-times price-to-earnings (P/E) ratio - ie its share price reflects investors’ willingness to pay $46 for every $1 of profit the company generated over the past year, based on its last four sets of quarterly results.

- Walmart at a 44 P/E ratio

- Amazon at a 33 P/E ratio

Upside down?

Source: Baillie Gifford & Co, Revolution, FactSet. USD. As at December 2025.

The Magnificent Seven are exceptional businesses. Most companies are not. Yet they have re-rated upward too. The US represents two-thirds of the global index, so stodgy and ‘expensive’ shares account for close to half the global market.

It could be argued that these premium valuations anticipate a new surge in growth from here. But remember, the S&P 500 today is much more profitable than in history, and not just because it is more tech-orientated.

US manufacturers increased net profit margins from about 5 per cent in the 1990s to about 15 per cent today. About a quarter came from lower interest rates. Another quarter from lower tax. Another quarter to a third from the impact of globalisation and outsourcing.

Thinking back to the tariffs announcements from spring 2025, what is the outlook? Tariffs are a tax. Given US finances, tax cuts elsewhere are not sustainable. The workforce is shrinking as the population ages and immigration falls, adding wage inflation to pressures on companies being asked to reshore.

As my colleague Tom Slater, head of Baillie Gifford’s US Equities Team, recently put it: “Today’s real danger lies in assuming things will revert to how they have always been. They will not. Coming decades will bring extraordinary advances and extraordinary dislocations. They will reward scale, ambition and adaptability. They will penalise complacency, inertia and the illusion of safety. For investors, the prudent course is not to spread capital thinly across what looks comfortable, but to ensure meaningful exposure to what is inevitable.”

The Cortés lesson

So, should you be all-in on AI as the only growth story?

Like many good historical tales, the Cortés boat-burning tale is dramatic – and totally wrong. Cortés didn’t torch them all. He did beach some. But he sent others home to Spain, others to find supplies, still more he dismantled and used to build a settlement. He was pragmatic and flexible.

Our Global Alpha strategy is similarly flexible and ruthlessly selective. We seek out and hold exceptional AI stocks, while finding growth in totally unrelated areas. We are especially interested in businesses that sit at bottlenecks in the AI value chain, where demand for their products far exceeds supply.

So, what are the exceptional AI stocks and where do we see those bottlenecks?

It is common to hear that in a gold rush, you should sell picks and shovels. At the start of the California gold rush, shovels were the bottleneck: you couldn’t dig for gold without one. Samuel Brannan, a ‘shovel baron’, became California’s first millionaire by selling them.

But his success attracted competition. The market became flooded with shovels. Prices fell by two-thirds between 1851 and 1855. Brannan went bust and died destitute.

Not all bottlenecks persist. Some do. The key is investing across the AI value chain – but only in genuine bottlenecks.

Nobody is about to flood the market with GPUs (graphics processing units, a type of specialised processor adept at AI tasks), because only NVIDIA designs the best. And only TSMC can make them efficiently.

© Utah State Historical Society Classified Photo Collection

At the other end of the AI value chain, Global Alpha favours companies that own distribution – such as Microsoft – or that apply the technology in their own businesses, for example: the mobile game advertising platform AppLovin.

What we avoid is AI-related businesses without proven business models, and companies whose share prices have been driven up on temporary shortages or datacentre rollout alone.

Uncorrelated growth

Enthusiastic as we are about generative AI, it’s not the only growth story.

The market is narrow, but the world is broad. While the AI bull market was surging in 2025, Global Alpha invested in UK-based Games Workshop. It has doubled revenues and tripled profits since Covid by selling its fantasy and sci-fi tabletop wargames. Another recent new purchase is Japan’s Keyence, which sells machine vision systems to automate factories.

In the US, FTAI Aviation refurbishes jet engines for airlines in a world where Boeing cannot get out of its own way. And Samsara provides sensors and software so that logistics companies can track all their trucks, drivers, and other equipment, allowing them to spot problems early.

Content-creating AI is a wonderful growth story. But we do not have to bet everything either way. By being selective, it is possible to choose parts of this paradigm shift that will be enduring sources of value, while filling our portfolios with stocks that can grow whether there is a bubble, tariffs or neither.

So don’t burn your boats. The set-up for the selective stock picker has never been better.

Annual past performance to 31 December each year (%)

| 2021 | 2022 | 2023 | 2024 | 2025 | |

| Global Alpha Composite (gross) | 8.0 | -28.6 | 20.3 | 11.9 | 18.6 |

| Global Alpha Composite (net) | 7.3 | -29.1 | 19.5 | 11.1 | 17.9 |

| MSCI ACWI | 19.0 | -18.0 | 22.8 | 18.0 | 22.9 |

Annualised returns to 31 December 2025 (%)

| 1 year | 5 years | 10 years | |

| Global Alpha Composite (gross) | 18.6 | 4.2 | 11.3 |

| Global Alpha Composite (net) | 17.9 | 3.6 | 10.6 |

| MSCI ACWI | 22.9 | 11.7 | 12.3 |

Source: Baillie Gifford, MSCI. US dollars. Returns have been calculated by reducing the gross return by the highest annual management fee for the composite. 1 year figures are not annualised.

Past performance is not a guide to future returns.

Legal notice: MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, endorsed, reviewed or produced by MSCI. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Risk Factors

The views expressed should not be considered as advice or a recommendation to buy, sell or hold a particular investment. They reflect opinion and should not be taken as statements of fact nor should any reliance be placed on them when making investment decisions.

This communication was produced and approved in January 2026 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

Potential for Profit and Loss

All investment strategies have the potential for profit and loss, your or your clients’ capital may be at risk. Past performance is not a guide to future returns.

This communication contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research, but is classified as advertising under Art 68 of the Financial Services Act (‘FinSA’) and Baillie Gifford and its staff may have dealt in the investments concerned.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this communication are for illustrative purposes only.