Key points

- LTGG believes optimism is a disciplined investment practice, not wishful thinking

- Companies like NVIDIA, Tesla and Amazon show how patience through volatility can create exceptional gains

- Pessimism feels safer but can close off opportunity; successful investing requires imagination

Image generated using AI

As with any investment, your capital is at risk.

To our ancient ancestors, it paid to err on the side of caution. Mistaking a stick for a snake might be inconvenient. Mistaking a snake for a stick could be fatal. So-called ‘Error Management Theory’ is one way that evolutionary psychologists explain some of the hard-wired cognitive biases that our species is still saddled with today.

But what might have saved us in the treacherous jungles of yesteryear is of much less use to the investor navigating the markets of today. Other well-documented cognitive biases, such as loss aversion – the tendency to feel the pain of loss more acutely than the pleasure of equivalent gain – make it easy to see why humans might prefer a cautious approach.

On top of that, more modern afflictions, such as the news cycle’s tendency to amplify catastrophe and failure, can alter our perceptions of the natural order of things. Small wonder, then, that pessimism abounds.

It is in this context that Long Term Global Growth (LTGG) has always sought to cultivate optimism. Indeed, at a conference earlier this month, members of the LTGG team spoke on the topic of ‘Optimising for Optimism’.

Timely as that theme might appear in a year when the Scotland men’s football team prepares for its first World Cup since 1998, the point was not to encourage wishful thinking. Rather, it was to emphasise that optimism, in the LTGG sense, is a deliberate discipline.

It means the ability to imagine what the market cannot. To take the possibility of extraordinary success seriously. It means the willingness to appear wrong, and occasionally even to be wrong, in the pursuit of exceptional returns.

Optimism in practice

Optimism is built into the very foundations of our investment process. Our 10 Question Stock Research Framework demands that we think imaginatively – that we consider how a company could be worth five times as much, and what it might look like 10 years from now.

The reason we do this is down to the asymmetric payoffs inherent in equity investing: losses are capped at what you put in. Gains, on the other hand, are potentially unlimited. Capturing those rare outliers more than compensates for the disappointments encountered along the way. And if we don’t train ourselves to think optimistically, we risk missing out on that unlimited upside.

In process terms, optimism finds perhaps its truest expression in the enforced period of positivity during the first half of every LTGG stock discussion. Nobody is allowed to say anything negative, as we force ourselves to explore all of the ways in which an investment case might go right. And yet, sometimes even that isn’t enough.

True outliers have a habit of exceeding not only market expectations, but our own attempts to imagine them. In 2016, our ‘blue sky’ case for NVIDIA envisioned the company reaching a $500bn valuation by 2026. At the time of writing, it was worth more than $5tn.

And to return to our footballing analogy, it is important to distinguish between the blind faith of Scotland’s travelling faithful as they head to North America this summer, and LTGG’s particular brand of optimism – perhaps we could call it ‘informed optimism’.

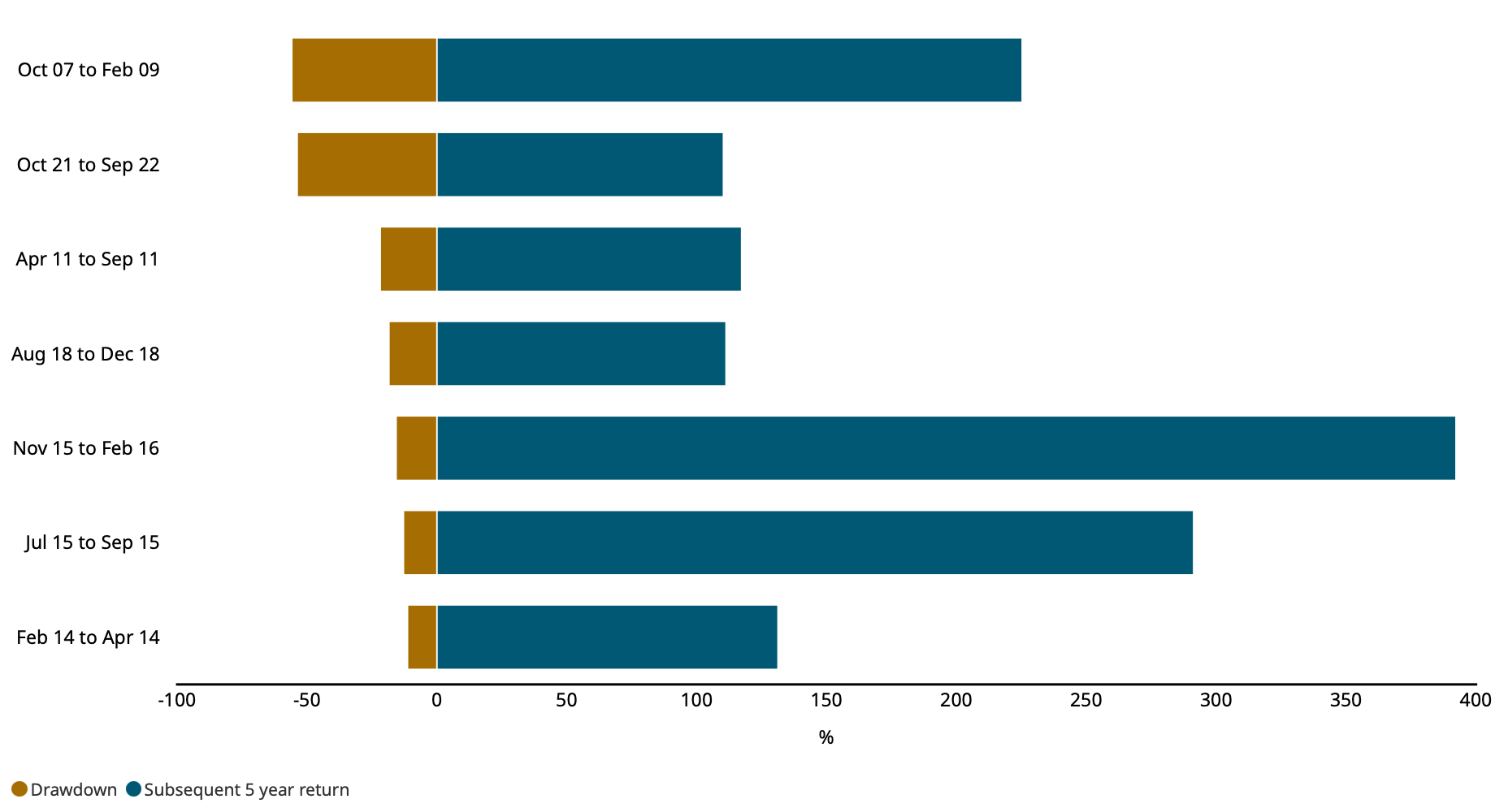

The biggest drawdown periods have been followed by exceptional returns

Source: Revolution. US dollar. As at 28 February 2026. LTGG composite drawdowns greater than 10% and their recovery since inception, 29 February 2004.

The views that we construct on companies are well-grounded in research, and in probability-weighted upside scenarios. That rigour is crucial, because while blind faith might sustain you through a nerve-jangling penalty shootout, it is less likely to serve you through a 60 percent drawdown.

Informed optimism, on the other hand, allows us to home in on what’s really important about the thesis. In that sense, it helps us to ground our conviction and deal with the inevitable volatility that comes our way.

Take, for instance, our recent experience with AppLovin, the digital advertising company. In February 2025, within months of our first purchase for clients, the stock fell 56 percent following a coordinated short-seller attack.

The reports were, it must be said, phenomenally persuasive. Sophisticated, technically detailed, and accusing AppLovin of complex shenanigans that ultimately inflated the impressive ROI it claimed to be delivering to customers.

In that scenario, it’s easy to see how an investment case based on blind faith might have crumbled. But informed optimism sent us back to the research.

We cross-referenced the short-sellers’ claims against our original due diligence and, crucially, against conversations with AppLovin's actual customers. That work revealed that the most serious allegation rested on the short-sellers’ fundamental misunderstanding of the company's revenue model.

Armed with renewed conviction in the thesis, we not only held our nerve but also made a small addition. Since those short seller attacks, AppLovin’s revenue has increased 84 percent, its EBITDA is up 100 percent, and it has delivered a roughly 3.5x return for clients since we first purchased in 2024 – making it one of the top contributors to the fund over the last five years. Panic born of blind faith would have wiped out much of that return.

Mistakes, we’ve made a few…

It is important to say that we don’t always get this right. One criticism often levelled at LTGG is that we can be slow to sell. That criticism is not always unfair. Our history is full of investment cases that didn’t pan out the way we hoped. But that is the nature of asymmetric returns. Many companies will disappoint. We can live with that.

The greater danger for LTGG is the opposite: giving up too early on a company whose upside remains far larger than the market appreciates. Some of our most painful mistakes have been premature sales of exceptional businesses.

In 2022, we sold Meta due to concerns over increasing competition in digital advertising and its ambitions for the so-called ‘Metaverse’. Since then, the share price has more than quintupled. Nostra culpa. But it is painful experiences such as these that force us to take our time, ensuring we do our utmost to exercise the optimism muscle.

Equally, some of our most valuable successes have been companies that experienced bouts of extreme negativity: NVIDIA, Tesla, Amazon, Hermès. All are companies that have returned our initial investment 30 times or more. And without our willingness to fully test the optimistic case, we would have been less likely to exercise our hold discipline. And less likely to have captured those outlier returns for our clients.

Perspective and patience

Optimism can also be a matter of perspective. The same facts can be viewed positively or negatively depending on your starting point. One of the obvious ways this applies for LTGG is our time horizon.

We are considering our investment opportunities over a period of five to 10 years. The market, on the other hand, is much more concerned about what happens in the next six months.

A near-term margin squeeze may be a reason for a short-term investor to sell. For us, if it widens the competitive advantage or expands the long-term opportunity, it is a reason to hold.

Near-term margin pressure, long-term advantage: MercadoLibre’s logistics reinvestment is helping entrench its market share. © AlfRibeiro – stock.adobe.com

This is why a company like MercadoLibre – now the only public company in the world to have delivered 28 consecutive quarters of 30 percent revenue growth – can have sold off by nearly 40 percent in the last year. The likely culprit: near-term margin compression driven by MercadoLibre’s reinvestment in logistics to strengthen its market share. For a short-term investor, that is a problem. For LTGG, it is a reason to be cheerful.

Such examples are not isolated cases. They are illustrations of a discipline, honed over LTGG’s 22 years. One that has to be actively cultivated, and sometimes held against considerable pressure. Pessimism may no longer be as central to our species' survival as it once was, but it remains persuasive.

The pessimistic case is often easier to articulate. It's easier to defend to clients and colleagues alike. It sounds sophisticated, and it often feels emotionally safer. Most investors today no longer need to worry about snakes emerging from the undergrowth. But they do face other fears: being different, being wrong, career risk, to name a few. And these fears can close off opportunity.

The upside case rarely presents itself neatly formed in a spreadsheet. The great companies of tomorrow will not arrive with obvious labels. Some will look controversial, strange or expensive. The optimist’s task is to remain imaginative enough to recognise them, rigorous enough to test them, and patient enough to hold them when the market tells us we are wrong.

Annual past performance to 31 March each year (%)

| 2022 | 2023 | 2024 | 2025 | 2026 | |

| Long Term Global Growth Composite (gross) | -17.5 | -17.5 | 27.1 | 8.5 | 5.0 |

| Long Term Global Growth Composite (net) | -18.1 | -18.1 | 26.2 | 7.7 | 4.3 |

| MSCI ACWI Index | 7.7 | -7.0 | 23.8 | 7.6 | 20.5 |

Annualised returns to 31 March 2026 (%)

| 1 year | 5 years | 10 years | 20 years | Since Inception* | |

| Long Term Global Growth Composite (gross) | 5.0 | -0.3 | 15.4 | 11.4 | 12.3 |

| Long Term Global Growth Composite (net) | 4.3 | -1.0 | 14.6 | 10.6 | 11.5 |

| MSCI ACWI Index | 20.5 | 10.0 | 11.9 | 8.2 | 8.8 |

Source: Revolution, MSCI. US dollars. Net returns have been calculated by reducing the gross return by the highest annual management fee for the composite. 1 year figures are not annualised. *29 February 2004.

Past performance is not a guide to future returns.

Legal notice: MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, endorsed, reviewed or produced by MSCI. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Risk factors and important information

The views expressed should not be considered as advice or a recommendation to buy, sell or hold a particular investment. They reflect opinion and should not be taken as statements of fact nor should any reliance be placed on them when making investment decisions.

This communication was produced and approved in June 2026 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

Potential for Profit and Loss

All investment strategies have the potential for profit and loss, your or your clients’ capital may be at risk. Past performance is not a guide to future returns.

This communication contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research, but is classified as advertising under Art 68 of the Financial Services Act (‘FinSA’) and Baillie Gifford and its staff may have dealt in the investments concerned.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this communication are for illustrative purposes only.

Important Information

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). Baillie Gifford & Co Limited is an Authorised Corporate Director of OEICs.

Baillie Gifford Overseas Limited provides investment management and advisory services to non-UK Professional/Institutional clients only. Baillie Gifford Overseas Limited is wholly owned by Baillie Gifford & Co. Baillie Gifford & Co and Baillie Gifford Overseas Limited are authorised and regulated by the FCA in the UK.

Persons resident or domiciled outside the UK should consult with their professional advisers as to whether they require any governmental or other consents in order to enable them to invest, and with their tax advisers for advice relevant to their own particular circumstances.

Financial Intermediaries

This communication is suitable for use of financial intermediaries. Financial intermediaries are solely responsible for any further distribution and Baillie Gifford takes no responsibility for the reliance on this document by any other person who did not receive this document directly from Baillie Gifford.

Transformations

Go behind the scenes of more than two decades of Long Term Global Growth (LTGG) thinking. This digital series brings our thinking to life, showing how the team finds those rare companies with the potential to shape the decade ahead.

10063740