Key points

-

The LTGG portfolio holds companies controlling scarce infrastructure and earning structurally powerful returns

-

Tight equity market correlations reinforce the importance of diversification, so we continue to cast the net wide

-

Underlying cash flow growth is at a decade high and portfolio valuations are very compelling

As with any investment, your capital is at risk.

Ninety-nine miles west of our new Haymarket office in Edinburgh lies the Gulf of Corryvreckan. The tide runs very strongly through this narrow Hebridean strait. On a calm day, the water is glassy. Divers visit the submerged pinnacles, and strong swimmers can cross the entire stretch of water. Conditions can change very quickly though and a notorious whirlpool often spools up from nowhere.

Local folklore attributes it to a sea witch but there’s a more prosaic explanation. When wind opposes the tide that has been accelerated by underwater bottlenecks, the water folds back on itself in a frothy spinning cauldron.

A few years ago, a mannequin thrown into the Corryvreckan whirlpool for a TV documentary was sucked downwards and eventually retrieved several miles away. The hapless dummy’s lifejacket was torn and its pockets were filled with gravel from the seabed, 250 metres beneath the surface.

During the first half of this year, global equity markets have been on swashbuckling form. Geopolitical concerns have largely been shrugged off, while the race to accelerate AI capability has continued in full flood. The market’s main response to further leaps in reasoning and agentic systems has been to chase short-term pinch points up the AI supply chain.

Manufacturers of dynamic random-access memory (DRAM), central processing units (CPUs), semiconductors and other computing components have led the charge, driving the lion’s share of recent market returns. It’s been a narrow and difficult market to navigate in that sense – and as a result, Long Term Global Growth (LTGG) has lagged the index, despite delivering decent absolute returns.

Against this heady backdrop, it pays to step back. There are still many questions about where the economics of frontier AI will settle.

First, the long-term cost of building and operating AI datacentre capacity remains uncertain, with limited visibility on token usage for particular applications. We’re seeing a shift from ‘all-you-can-eat buffet’ pricing to usage-based charging models. There are further questions around whether small language models (SLM’s) can in fact, match large ones for many everyday tasks. At the same time, access to leading AI models may be shaped by increasingly capricious governments.

Given all these questions, the LTGG doctrine of holding our contentions ‘passionately but lightly’ seems especially pertinent at the current juncture.

It’s important that we continue to stress test new ideas across every level of the AI layer cake. We’ve continued to pound the pavements of Silicon Valley and Shenzhen accordingly. Although we’re open to the possibility that historically commoditised and cyclical parts of the compute supply chains may see improving economics, capital is already flowing towards many near-term pinch points to expand capacity. This begs the question of whether the recent earnings growth surge in parts of the index is sustainable.

Given the wide range of potential outcomes, LTGG’s preferred approach is to own companies that are structurally difficult to substitute, and where we have greater confidence in the sustainability of high earnings growth.

Image: generated by AI

The Corryvreckan bottleneck’s turbulence stems from a hard underwater basalt plug known as the Old Hag. We’re looking to hold companies with similarly unassailable leads in their domains. Nvidia and ASML, both held in the LTGG portfolio for around a decade, are two such examples.

Nvidia remains a fascinating case study: a $5tn company whose net income continues to accelerate from a trailing 12-month base in excess of 100 percent. Founder Jensen Huang is playing a much broader game of chess than most participants in the AI ecosystem. He continues to shore up a grip on the whole supply chain – from the suppliers building infrastructure to those developing models on top of their ecosystems.

The message from across the leading independent AI labs is that they cannot get their hands on enough compute and the rental rates for Nvidia chips continue to climb. With just 16 percent of US adults using AI daily, there is a massive runway for future adoption. It will be interesting to see whether Nvidia’s planned expansion into the PC market helps to unlock the next phase of the opportunity.

ASML presides over a similarly intractable bottleneck. Its extreme ultraviolet (EUV) lithography equipment enables the manufacturing of chips that are one twenty-thousandth the width of a human hair. The company’s effective monopoly rests on an ecosystem of nearly 5,000 tier-one suppliers.

For over four decades, ASML has been carefully cultivating and perfecting this intricate supply chain. It has taken equity stakes in critical companies, structuring relationships and revenue shares to avoid overdependence on any single customer or supplier. ASML’s earnings growth is accelerating and free cash flow has more than tripled over the past three years, outpacing its share price by some margin. We continue to see huge scope for growth.

The most recent purchase for the LTGG portfolio is also based on its position as a compute supply chain lynchpin. In the two decades since its first launch, SpaceX has delivered more than 50 times the payload into space of its nearest western competitor – an Old Hag-like command of the bottleneck in launch capabilities.

This new holding’s long-term roadmap is based on the provision of large-scale orbital compute infrastructure, with the potential deployment and operation of a million compute-bearing satellites.

Unsurprisingly, the market noise surrounding the company’s high-profile initial public offering (IPO) has been deafening. The analytical challenge here has been reminiscent of other prominent listings we’ve looked at on the LTGG Team over the years – squaring a vertigo-inducing near-term valuation multiple with the clear potential for outlier returns.

Logjams beyond compute

Over the past couple of decades, the market has persistently underestimated Amazon’s ability to invest at scale – converting marginal costs into capital costs, then leveraging those capital costs by selling internally-developed services to other businesses.

This dynamic is in full swing at Amazon Web Services (AWS). Its $150bn revenue run rate is fuelled not only by AI but also by a widely underappreciated CPU and custom silicon business that is growing at triple-digit rates.

The playbook is now being replicated through Amazon Supply Chain Services (ASCS), which enables external customers to access Amazon’s freight, trucking and distribution network. With the Global Supply Chain Pressure Index sitting at its highest ever level, Amazon can preside over this logjam by opening up its infrastructure of 80,000 trailers, 100 aircraft and 24,000 containers to third parties.

CATL’s command of the battery supply chain makes it a critical enabler of both AI and the broader electrification of the global economy. Image: © Xinhua/Shutterstock

Meanwhile, we’ve added to our holding in CATL, a critical cornerstone of the global energy storage market. As energy security and consumption become increasingly central to political policy, CATL’s growing grip on key power bottlenecks stems from its control of the upstream battery supply chain.

By securing strategic mineral reserves and aggressively scaling gigafactories, founder Robin Zheng and his mercurial team can dictate the global pace of deployment for stationary energy storage systems. The multi-billion-dollar global expansion is well underway. With customer reliance on CATL’s cells deepening, market share is rising and margins continue to improve.

CATL’s technological lead is also extending. The April announcement of the Qilin sodium-ion battery (capable of charging to 1,500 km of range in a few minutes) felt like an overlooked ‘Deepseek’ moment for energy. As Robin Zeng points out, “The boundaries of electrochemistry are still far from being reached, and the possibilities of materials science are still far from being exhausted.”

CATL plans to establish 100,000 charging and swapping stations by the end of 2028, and there is an increasingly credible path for the company to become the AWS of energy services.

A big chunk of stock market capital has been pursuing defence stocks recently. But in a market prone to chasing thematic labels, there’s an important distinction to be made between the companies enjoying a short-term sugar rush from a related index classification, and those that preside over enduring bottlenecks. We believe that Cloudflare sits firmly in the latter camp.

The company now intercepts and autonomously mitigates 250 billion cyber threats each day. Its vast infrastructure footprint and developer ecosystem of over a million users constitute a formidable self-reinforcing moat. That creates a powerful flywheel dynamic because every threat absorbed by Cloudflare strengthens its globally distributed immune system, improving the speed and accuracy of its threat intelligence.

Competitors without a similarly scaled, shared-edge architecture struggle to replicate this advantage. A recently announced tie-up with Anthropic pushes Cloudflare deeper into the emerging Al agent ecosystem, with the potential to deepen its moat still further.

Shifting sands in commerce

Beyond our reflections on the bottleneck controllers, we have been thinking about the commerce-related holdings in the portfolio. Mr Market has been fretting about whether these businesses can withstand the rise of agentic AI, but we’ve been exploring the extent to which they might instead accelerate by surfing on advances in agentic commerce and proprietary data.

Shopify is particularly interesting in this context. Its share price is little changed over the past five years, despite free cash flow increasing fivefold over the same period. Revenue growth has ticked up to the mid-30s this year on the back of an acceleration in gross merchandise value (GMV) and operating margins are also expanding.

Agentic commerce introduces complexity around advertising, checkout, payment, inventory processing and shipping, and our hypothesis is that Shopify gatekeeps that complexity. This means that regardless of which large language models (LLMs) or shopping agents win out, Shopify should be well placed to provide the commerce infrastructure substrate.

Founder Tobi Lutke, well-known for his technical prowess, has been spending a lot of time coding lately. We suspect that this is in marked contrast with most listed company chief executives. Shopify’s ability to adapt should remain well-honed as a result.

Nubank’s digital financial platform is widening access to credit whilst rapidly taking share from established banks in Latin America. Image: © Shutterstock / Postmodern Studio

We’ve been similarly encouraged by the operational performance of the portfolio’s two Latin American commerce holdings. Nubank has continued to take share from traditional banks in the region and is now the second-largest financial institution in Brazil.

Revenue has grown about 40 percent over the past 12 months, while Nubank’s efficiency ratio – the cost to generate $100 of revenue – has fallen to below 20 percent. Top-tier legacy banks fight tooth and nail to break below 50 percent on this metric.

Nubank’s edge extends beyond its lack of physical infrastructure. We’ve been speaking with David Velez and his team about their replacement of traditional credit-scoring systems with real-time AI models that ingest the unstructured transaction data that traditional models routinely ignore. This is particularly relevant in Latin America, where millions of consumers have little or no credit history. As a result, Nubank can dynamically adjust credit limits in real time while maintaining tight control of overall risk.

Meanwhile, Mercadolibre (Meli), NuBank’s Latin American brethren, has been growing faster still – with revenue accelerating to almost 50 percent year-over-year. Like Nubank, its share price has languished while it has deliberately reinvested several hundred basis points of margin back into user acquisition and shipping infrastructure.

Over the years, Meli has been very consistent in applying this Amazon-esque approach; trading the juicing of short-term earnings for the long-term benefit of an ever-deepening moat. Mr Market has a different exchange rate of time-to-value and shows little tolerance for long-term measures of this nature at present.

The future right tail

Given correlations in the equity markets of late, we’ve been closely monitoring the shape and metabolism of the LTGG portfolio. Our situational awareness is aided by a more advanced suite of analytics tools than we had at our disposal a few years ago.

We have decided to sell Atlassian from the portfolio following a decade-long tenure. While the company continues to grow in the mid-20s and near-term operational performance should hold up, we have longer-term concerns that Atlassian’s enterprise offering may find itself on the wrong side of AI-driven disruption.

We have redeployed part of the Atlassian sale proceeds to fund an addition to Adyen. In our view, the structural moat and quality of Adyen’s enterprise payments business is materially higher, despite it having been caught up in the same indiscriminate sectoral basket sell-off.

Tight equity market correlations underscore the importance of maintaining a diverse idea pipeline. New portfolio holding QXO is a technologically advanced consolidator and distributor in the building materials industry.

The contrast between QXO and SpaceX, as our other new holding this quarter, is based on our observation that historic LTGG outliers have materialised in different ways and from different parts of the market. We need to continue casting our idea net widely.

Two decades ago, Atlas Copco, a Swedish mining technology company, was the largest holding in LTGG. At the time, around a quarter of the portfolio was invested in mining and resource companies, several of which went on to deliver very substantial returns.

We have recently been revisiting this domain and our logic is simple. While AI token use can scale exponentially, the essential physical inputs to the AI buildout can only expand linearly; indeed, in areas such as copper, supply is barely responding to surging demand.

The likes of Zijin Mining and Freeport-McMoRan deserve some more research work from us, as do MP Materials (America’s only fully-integrated rare-earth producer) and Cameco, a leading uranium supplier. As elsewhere, our challenge is to identify companies that preside over enduring structural bottlenecks convincingly, separating them from the current market hype around any player that happens to sit at a transient market pinch point.

Other stocks in the recent idea hopper have included Kratos (weapon components), Alnylam (RNA-inference therapeutics) and Meesho (Indian discount online commerce). We’ve also revisited Chinese online travel company Trip.com, a former LTGG holding.

At the mercy of sea witch

Seventy-nine years ago, novelist George Orwell took his family to a remote lodge on the Isle of Jura while he finished writing the seminal 1984. His diaries describe a marvellous summer, with endless balmy days and unusually calm weather.

Nearing the end of his manuscripts, George decided to take his young family on a motorboat excursion. But he completely misread the tide tables. The boat’s outboard motor was too feeble to resist Corryvreckan’s pull and the whirlpool tore it off.

Fortunately for Orwell and his hapless crew, the sea witch was in a kindly mood. Although her maelstrom capsized the boat, she generously deposited them on a rocky outcrop nearby. Eventually rescued with his shaken family by a passing lobster boat, Orwell is said to have muttered, “I thought we were goners,” before returning to complete 1984 once the shock had receded.

Current fair weather and rising tides in the equity markets can be deceptively seductive for equity market tourists. Beneath the surface, supply/demand imbalances in the equity base persist and material geopolitical challenges are largely being shrugged off. The MSCI AC World Index has risen almost 13 percent so far this year, a very unusual outcome in a historic context.

Why has LTGG lagged this rising market? Not all the technical factors are transparent or explainable, but what’s clear is that the share prices of many index constituents have been rising heroically, driven by both upward reratings and recent earnings spikes that are of unproven durability. By contrast, growth engine longevity and robust underpinnings are being meaningfully discounted by market analysts who very rarely look more than a couple of years ahead.

Fundamental truths and hard stones

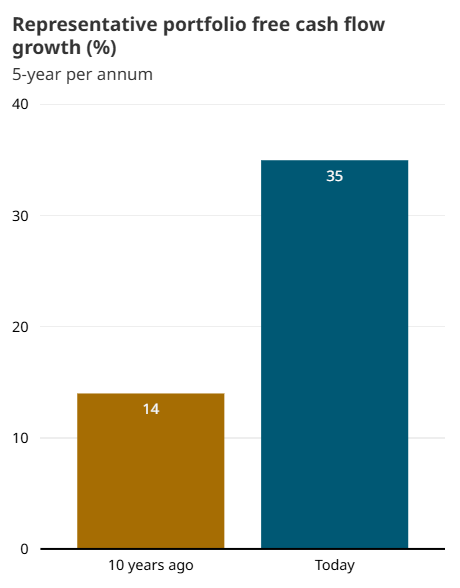

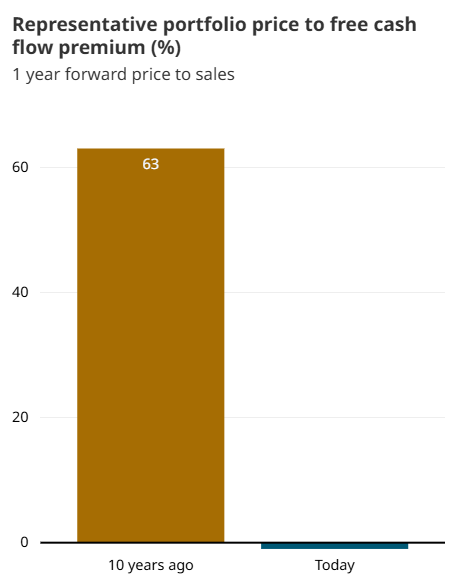

The dynamics above mean that, despite LTGG’s annual free cash flow growth more than doubling to 35 percent over the last decade, the historic valuation premium for this superior growth has collapsed. One-year forward price-to-sales and price-to-earnings multiples have shrunk to their lowest levels in a decade. More strikingly, for the first time in LTGG’s history, the portfolio trades at a lower price-to-free-cash-flow multiple than the index.

Source: Baillie Gifford & Co, FactSet, MSCI. Excludes cash. US dollar. Based on a representative LTGG portfolio. Index: MSCI All Country World. As at 31 May 2026.

This bears repeating. Never before has LTGG’s prodigious cashflow growth been available at such compelling valuations.

Four months after his fracas with the Corryvreckan, George Orwell was admitted to Hairmyres Hospital with advanced tuberculosis. Beneath a stoic exterior, his underlying inner health had been deteriorating for some time. The shock of the Corryvreckan encounter hastened that decline. 1984 was published the following year but Orwell died less than two years later.

The Market Sea Witch has been in an indulgent mood of late. However, no equity market participant should rely on that persisting. Over time, share prices are driven by fundamentals, not by hope, by faith or by fear of missing out.

As Orwell wrote in 1984, “Truisms are true, hold onto that! The solid world exists, its laws do not change. Stones are hard, water is wet, objects unsupported fall towards the earth’s centre.”

With its strong immune system, prodigious underlying cashflow progression, and powerful growth engines, LTGG is exceptionally well placed for that eventuality.

Annual past performance to 31 March each year (%)

| 2022 | 2023 | 2024 | 2025 | 2026 | |

| Long Term Global Growth Composite (gross) | -17.5 | -17.5 | 27.1 | 8.5 | 5.0 |

| Long Term Global Growth Composite (net) | -18.1 | -18.1 | 26.2 | 7.7 | 4.3 |

| MSCI ACWI Index | 7.7 | -7.0 | 23.8 | 7.6 | 20.5 |

Annualised returns to 31 March 2026 (%)

| 1 year | 5 years | 10 years | 20 years | Since Inception* | |

| Long Term Global Growth Composite (gross) | 5.0 | -0.3 | 15.4 | 11.4 | 12.3 |

| Long Term Global Growth Composite (net) | 4.3 | -1.0 | 14.6 | 10.6 | 11.5 |

| MSCI ACWI Index | 20.5 | 10.0 | 11.9 | 8.2 | 8.8 |

Source: Revolution, MSCI. US dollars. Net returns have been calculated by reducing the gross return by the highest annual management fee for the composite. 1 year figures are not annualised. *Inception date: 29 Feb 2004

Past performance is not a guide to future returns.

Legal notice: MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, endorsed, reviewed or produced by MSCI. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Risk factors and important information

The views expressed should not be considered as advice or a recommendation to buy, sell or hold a particular investment. They reflect opinion and should not be taken as statements of fact nor should any reliance be placed on them when making investment decisions.

This communication was produced and approved in July 2026 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

Potential for Profit and Loss

All investment strategies have the potential for profit and loss, your or your clients’ capital may be at risk. Past performance is not a guide to future returns.

This communication contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research, but is classified as advertising under Art 68 of the Financial Services Act (‘FinSA’) and Baillie Gifford and its staff may have dealt in the investments concerned.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this communication are for illustrative purposes only.

10064113