Listen to this article

This audio is generated using AI

© The Maclean Brothers

As with any investment, your capital is at risk.

The image jars in the best way: an oar in one hand, a global studio in the other. It’s the feeling of the frontier suddenly moving. Imagine where this level of pervasive connectivity, combined with generative AI and autonomous robots, could lead?

Harnessing massive structural shifts is part of our investment edge: our 5-10-year time horizon and our experience of investing through multiple system changes in society, from the beginning of the internet through the mobile and cloud eras, are key.

We know that we can’t say where a technology may take us exactly, so you have to think probabilistically, and some patterns and laws help give us certainty. We know that it pays to back tech-savvy leaders and founders driving disruption, and we seek a value proposition to the customer that will drive significant change. Using these methods, we can predict which companies might form the foundational layers for the future.

For example, in 2013, when we were first analysing Tesla, there were some predictions we could make with a high degree of confidence about the energy density of batteries, the cost of onboard computing and the power of software. Wright's law in manufacturing dictated that as Tesla made more vehicles, it would be able to do so increasingly efficiently. Jevon’s paradox dictates that those costs decline, and increased energy efficiency would disproportionately impact demand. In 2023, the Tesla Model Y became the best-selling passenger vehicle in the world. While he is controversial, having mercurial tech-savvy Elon Musk as CEO was also key to Tesla’s success over that decade.

We could tell similar stories about our long-term investments in Amazon, Netflix and NVIDIA, among many others.

Now we are in a new technological paradigm. Things are getting weird, quickly.

Streets that drove the same way for a century have cars with nobody in the front seat. Hiring pipelines built on “learn on the job” are wobbling, while AI copilots are becoming standard for employees. None of this is linear. That’s the point: the weirdness is the signal.

Street-level weird: robotaxis jump from novelty to infrastructure

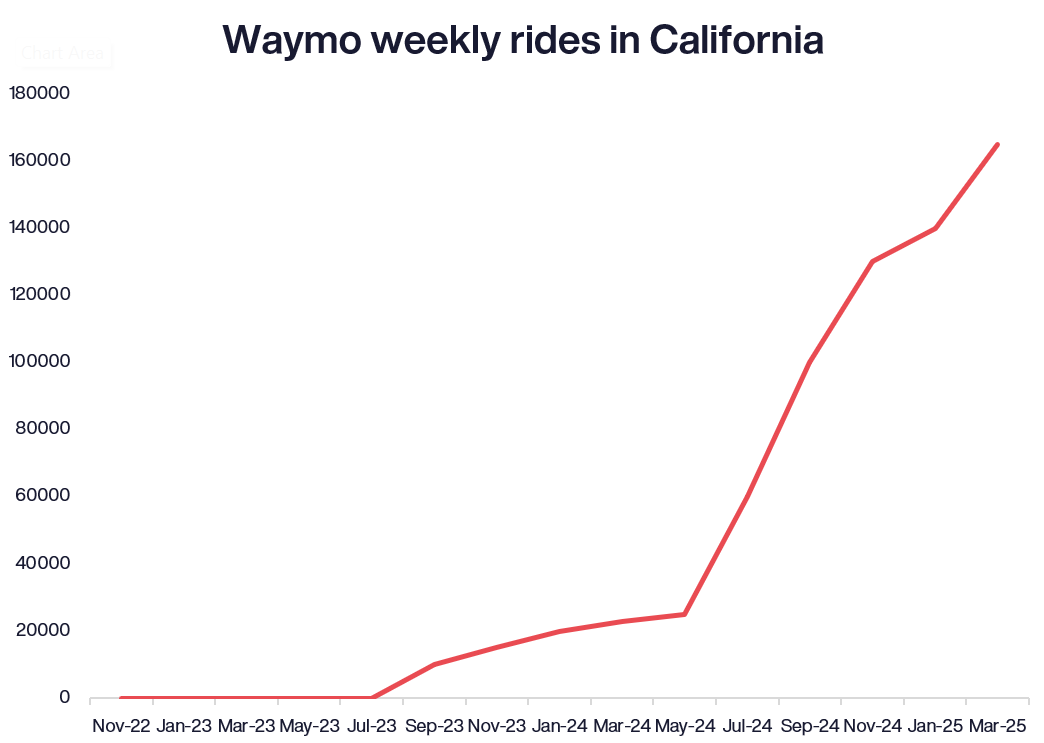

If you visit San Francisco today, there’s a decent chance you’ll ride with Waymo, the autonomous taxi company. Paid trips have surged from experimental levels to hundreds of thousands per week across its markets, with California service areas widening and total ridership crossing eight figures. Waymo is now ahead of Lyft in terms of the number of rides, despite currently taking longer and costing more. This is an early sign of product–market fit before cost curves fall and networks compound. People really like travelling without a driver. This could be a ‘normalisation moment’: fewer headline-grabbing demos, more everyday transport.

The point: once a technology is “good enough somewhere,” capital, talent and regulators reorient around the new baseline, and adjacent uses (delivery, logistics and beyond) become more plausible – like a YouTube studio in the middle of the Pacific Ocean.

Source: Nat Bullard data

Labour-market weird: juniors feel it first

AI will bring about the most significant change to the global labour market in human history, so says the CEO of leading AI company Anthropic, Dario Amodei. Recent evidence suggests this may have already started: since late 2022, employment for 22–25-year-olds in the most AI-exposed occupations (such as software development or customer support) declined by about 6 per cent, even as older workers in the same roles grew by roughly 6–9 per cent. In AI-exposed jobs, entry-level hiring is approximately 13 per cent lower than expected versus comparable roles, even after controlling for company-wide trends.

Of course, reality is nuanced: within a single firm, AI can reduce headcount in Department A while raising it in Department B so that macro aggregates can mask sharp local effects. And yes, it’s observational, not causal. But it is a signal that something weird is going on, at the very least. Just look at Microsoft – AI coding copilots and research assistants are now table stakes for many developers and analysts – up to 30 per cent of Microsoft’s code is now written by AI.

So what? Why this matters for our portfolio work

The Macleans’ crossing is a visceral metaphor. New capabilities create disruption and innovation. When the middle of the Pacific becomes a broadcast studio, everything else, such as how we travel, how our businesses operate and how we work, trade and socialise with each other, could all be upended in hard-to-predict ways.

We aim to create portfolios that are on the right side of this disruption. As such, we seek to invest in enablers and embedded platforms tied to falling cost curves, enhanced workflows, distribution, autonomy and developer ecosystems – the infrastructure that is hard to dislodge, and where we see real traction and signal in company operations and fundamentals.

©2025 Aurora Operations, Inc.

For example, one of our exposures to ‘street-level weird’ is self-driving vehicle company Aurora Innovation, which has driverless trucks delivering goods along highways in Texas.

From the commercial launch of its autonomous trucks at the end of April 2025 to the end of June, Aurora has already logged more than 50,000 driverless miles in daytime with clear weather conditions. In July, the company completed validation and began driverless operations at night, and it now has three driverless trucks on its Dallas to Houston route. Aurora has maintained close to 100 per cent on-time performance, with a perfect safety record. By the end of this year, it aims to open two more routes from Fort Worth to El Paso and Phoenix, while also working to validate driverless operations in more challenging weather, which is also expected by the end of 2025. A small but impressive start, with steady progress to address a huge opportunity: the trucking market in the US alone was $875 bn in 2021, a third of which was driver wages. We wouldn’t be surprised if the majority of truck miles driven were autonomous in ten years. Will human drivers even be seen as weird in 2035?

Investment manager Kirsty Gibson meeting some of the team at Aurora in 2024.

Elsewhere, relating to weirdness in the labour market and the enterprise, our investment in cloud-based data storage and analysis company Snowflake is an interesting example. Like Aurora, Baillie Gifford has invested in Snowflake since it was a private company. Our original thesis at IPO in 2020 was that it would grow rapidly because it simplifies messy, siloed data for its customers with a fast, easy, pay-as-you-go Data Cloud. The powerful tailwind of the shift from on-premises to cloud computing, the ever-increasing data growth, and the desire to gain insights from it were hugely appealing.

However, growth slowed in the post-pandemic period due to its customers optimising their cloud spend to control costs in a higher interest rate environment. As generative AI began to gain traction, the CEO at the time, Frank Slootman, announced his retirement in early 2024 to give a “hard-driving technologist” the helm, Sridhar Ramaswamy, Snowflake’s senior vice president (SVP) of AI, and ex-head of Google Ads. This was the tech-savvy leader Snowflake needed for its next phase of growth centred on AI.

Since then, growth has reaccelerated, with AI now powering 25 per cent of all customer projects. Its most recent results suggest AI is automating and accelerating cloud migrations through tools like SnowConvert AI. Ramaswamy says, “Today, AI is a core reason why customers are choosing Snowflake, influencing nearly 50 per cent of new logos won” in the last quarter. Fundamental acceleration like this at Snowflake’s scale is impressive.

Weird today, norm tomorrow

In conclusion, ‘weird’ is what system change feels like up close: robotaxis normalising in one city while juniors are squeezed even as senior productivity climbs and cloud migration accelerates, self-driving trucks on the highway day and night, and a live ocean podcast from the literal middle of nowhere. For long-term investors, the task isn’t to pick a single story. It’s to see the big picture, look for signals and patterns, and then back the teams and exceptional growth companies most likely to convert today’s strangeness into tomorrow’s operating leverage and returns.

Risk factors

The views expressed should not be considered as advice or a recommendation to buy, sell or hold a particular investment. They reflect opinion and should not be taken as statements of fact nor should any reliance be placed on them when making investment decisions.

This communication was produced and approved in September 2025 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

This communication contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research, but is classified as advertising under Art 68 of the Financial Services Act (‘FinSA’) and Baillie Gifford and its staff may have dealt in the investments concerned.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this communication are for illustrative purposes only.

Important information

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). Baillie Gifford & Co Limited is an Authorised Corporate Director of OEICs.

Baillie Gifford Overseas Limited provides investment management and advisory services to non-UK Professional/Institutional clients only. Baillie Gifford Overseas Limited is wholly owned by Baillie Gifford & Co. Baillie Gifford & Co and Baillie Gifford Overseas Limited are authorised and regulated by the FCA in the UK.

Persons resident or domiciled outside the UK should consult with their professional advisers as to whether they require any governmental or other consents in order to enable them to invest, and with their tax advisers for advice relevant to their own particular circumstances.

Financial Intermediaries

This communication is suitable for use of financial intermediaries. Financial intermediaries are solely responsible for any further distribution and Baillie Gifford takes no responsibility for the reliance on this document by any other person who did not receive this document directly from Baillie Gifford.

Europe

Baillie Gifford Investment Management (Europe) Ltd (BGE) is authorised by the Central Bank of Ireland as an AIFM under the AIFM Regulations and as a UCITS management company under the UCITS Regulation. BGE also has regulatory permissions to perform Individual Portfolio Management activities. BGE provides investment management and advisory services to European (excluding UK) segregated clients. BGE has been appointed as UCITS management company to the following UCITS umbrella company; Baillie Gifford Worldwide Funds plc. BGE is a wholly owned subsidiary of Baillie Gifford Overseas Limited, which is wholly owned by Baillie Gifford & Co. Baillie Gifford Overseas Limited and Baillie Gifford & Co are authorised and regulated in the UK by the Financial Conduct Authority.

China

Baillie Gifford Investment Management (Shanghai) Limited 柏基投资管理(上海)有限公司(‘BGIMS’) is wholly owned by Baillie Gifford Overseas Limited and may provide investment research to the Baillie Gifford Group pursuant to applicable laws. BGIMS is incorporated in Shanghai in the People’s Republic of China (‘PRC’) as a wholly foreign-owned limited liability company with a unified social credit code of 91310000MA1FL6KQ30. BGIMS is a registered Private Fund Manager with the Asset Management Association of China (‘AMAC’) and manages private security investment fund in the PRC, with a registration code of P1071226.

Baillie Gifford Overseas Investment Fund Management (Shanghai) Limited

柏基海外投资基金管理(上海)有限公司(‘BGQS’) is a wholly owned subsidiary of BGIMS incorporated in Shanghai as a limited liability company with its unified social credit code of 91310000MA1FL7JFXQ. BGQS is a registered Private Fund Manager with AMAC with a registration code of P1071708. BGQS has been approved by Shanghai Municipal Financial Regulatory Bureau for the Qualified Domestic Limited Partners (QDLP) Pilot Program, under which it may raise funds from PRC investors for making overseas investments.

Hong Kong

Baillie Gifford Asia (Hong Kong) Limited 柏基亞洲(香港)有限公司 is wholly owned by Baillie Gifford Overseas Limited and holds a Type 1 license from the Securities & Futures Commission of Hong Kong to market and distribute Baillie Gifford’s range of collective investment schemes to professional investors in Hong Kong. Baillie Gifford Asia (Hong Kong) Limited 柏基亞洲(香港)有限公司 can be contacted at Suites 2713-2715, Two International Finance Centre, 8 Finance Street, Central, Hong Kong. Telephone +852 3756 5700.

South Korea

Baillie Gifford Overseas Limited is licensed with the Financial Services Commission in South Korea as a cross border Discretionary Investment Manager and Non-discretionary Investment Adviser.

Japan

Mitsubishi UFJ Baillie Gifford Asset Management Limited (‘MUBGAM’) is a joint venture company between Mitsubishi UFJ Trust & Banking Corporation and Baillie Gifford Overseas Limited. MUBGAM is authorised and regulated by the Financial Conduct Authority.

Australia

Baillie Gifford Overseas Limited (ARBN 118 567 178) is registered as a foreign company under the Corporations Act 2001 (Cth) and holds Foreign Australian Financial Services Licence No 528911. This material is provided to you on the basis that you are a “wholesale client” within the meaning of section 761G of the Corporations Act 2001 (Cth) (“Corporations Act”). Please advise Baillie Gifford Overseas Limited immediately if you are not a wholesale client. In no circumstances may this material be made available to a “retail client” within the meaning of section 761G of the Corporations Act.

This material contains general information only. It does not take into account any person’s objectives, financial situation or needs.

South Africa

Baillie Gifford Overseas Limited is registered as a Foreign Financial Services Provider with the Financial Sector Conduct Authority in South Africa.

North America

Baillie Gifford International LLC is wholly owned by Baillie Gifford Overseas Limited; it was formed in Delaware in 2005 and is registered with the SEC. It is the legal entity through which Baillie Gifford Overseas Limited provides client service and marketing functions in North America. Baillie Gifford Overseas Limited is registered with the SEC in the United States of America.

The Manager is not resident in Canada, its head office and principal place of business is in Edinburgh, Scotland. Baillie Gifford Overseas Limited is regulated in Canada as a portfolio manager and exempt market dealer with the Ontario Securities Commission ('OSC'). Its portfolio manager licence is currently passported into Alberta, Quebec, Saskatchewan, Manitoba and Newfoundland & Labrador whereas the exempt market dealer licence is passported across all Canadian provinces and territories. Baillie Gifford International LLC is regulated by the OSC as an exempt market and its licence is passported across all Canadian provinces and territories. Baillie Gifford Investment Management (Europe) Limited (‘BGE’) relies on the International Investment Fund Manager Exemption in the provinces of Ontario and Quebec.

Israel

Baillie Gifford Overseas Limited is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the Advice Law) and does not carry insurance pursuant to the Advice Law. This material is only intended for those categories of Israeli residents who are qualified clients listed on the First Addendum to the Advice Law.

Singapore

Baillie Gifford Asia (Singapore) Private Limited is wholly owned by Baillie Gifford Overseas Limited and is regulated by the Monetary Authority of Singapore as a holder of a capital markets services licence to conduct fund management activities for institutional investors and accredited investors in Singapore. Baillie Gifford Overseas Limited, as a foreign related corporation of Baillie Gifford Asia (Singapore) Private Limited, has entered into a cross-border business arrangement with Baillie Gifford Asia (Singapore) Private Limited, and shall be relying upon the exemption under regulation 4 of the Securities and Futures (Exemption for Cross-Border Arrangements) (Foreign Related Corporations) Regulations 2021 which enables both Baillie Gifford Overseas Limited and Baillie Gifford Asia (Singapore) Private Limited to market the full range of segregated mandate services to institutional investors and accredited investors in Singapore.

170821 10057469