Your capital is at risk. Past performance is not a guide to future returns and any income is not guaranteed.

This quarter, the portfolio achieved good absolute returns – around 7 percent in sterling terms. Dividend growth was good too – distributions were around 4 percent higher than last year. Over a single quarter, these are respectable outcomes and consistent with the steady compounding we are trying to deliver for our clients.

But when compared with what you could have had – the index return – the capital growth looks distinctly lacklustre. It is a pattern we have seen over the past couple of years. While we have generated the income you expect from us, growth has not kept pace with what you could have had elsewhere. In short, our approach has been a bit dull compared with exuberant markets driven higher by the AI arms race.

We know this is frustrating – we feel that frustration acutely ourselves. But we also know the role we play in our clients’ wider asset allocation. We’re not expected to outperform in the most buoyant market environments, but to protect capital when conditions become less forgiving. To compound steadily and provide a reliable income stream that allows more risk to be taken elsewhere.

To achieve this, our strategy is one of prudent diversification among a broad range of potential growth drivers. That can look unexciting when markets are being driven higher by a single theme. But we believe the same discipline that has held us back in this environment is also what should matter most when capital becomes more discriminating, earnings resilience is tested, and investors again place value on dependability.

This quarter, we compare the beliefs represented in the portfolio with those embedded in an index tracker, discuss the costs and benefits of those beliefs over the year so far, and show how we continue to test them through our Quality Growth Review and Dividend Hall of Shame exercises.

Believe it or not

In 1918, cartoonist and explorer Robert Ripley began publishing illustrated newspaper panels under the title “Believe It or Not!”. The format was simple - short, surprising claims about real people, places, customs, and objects from around the world. Over a hundred years later, his ‘Odditoriums’ still operate in tourist hot spots like London and New York. Their appeal comes from the mix of travel, trivia, spectacle, and the feeling that reality can sometimes be stranger than fiction.

A century after Ripley made a business of the improbable, the stock exchanges in those same cities offer their own collection of oddities. In the US market, passive’s share of assets under management is now ten percentage points higher than active, and fundamental investors make up less than an eighth of daily trading volumes. Retail participation, supercharged by the pandemic, adds further noise. The result is a market where short-term price signals are increasingly set by participants who either cannot or will not discriminate on value.

Consider this quarter’s SpaceX IPO. As index providers rush to accommodate the newly listed company, JPMorgan estimates that tracker funds will be forced to sell approximately $90 billion worth of existing holdings to make room – including more than $15 billion of Apple and more than $10 billion of each of Microsoft and Alphabet. The sellers will not be acting on any view of those companies’ prospects. They will be selling three of the most consistently profitable businesses on earth simply because the index told them to.

A tracker investment is not a neutral expression of global growth opportunities. Around one-third is aligned with the AI capex theme, and a further tenth with the associated tech platforms; but only around 5 percent in the electrification necessary to make AI scalable. These skewed exposures carry risk – not just that this theme may not continue to be rewarded as richly as it has been, but that opportunities are overlooked elsewhere as passive buying rewards only what is already large and obvious.

Let’s be clear, our portfolio is not anti-AI. We are believers in this transformative technology. But we have some caution on the speed and smoothness of its rollout. In sectors beyond technology, where return on investment remains elusive, adoption rates are likely to be slower. Companies are wrestling with heavy regulation, deep process re-engineering and data governance requirements. This could be a long process and companies will need help, which is why we are sticking by holdings like Accenture and Wolters Kluwer, even as the market writes them off as AI losers.

We believe it is right to give our clients healthy exposure to this exciting theme – we have around 14 percent of the portfolio invested in companies associated with the infrastructure buildout – but it’s prudent to balance this with a broader set of growth engines the index may overlook because they are less fashionable, less crowded or simply smaller today: financial infrastructure, industrial productivity, electrification, healthcare, digital consumption and global consumer franchises. In time, we would expect all these areas to benefit from the lower cost bases and expanded margin structures AI promises, but some may require more patience than the market is pricing in.

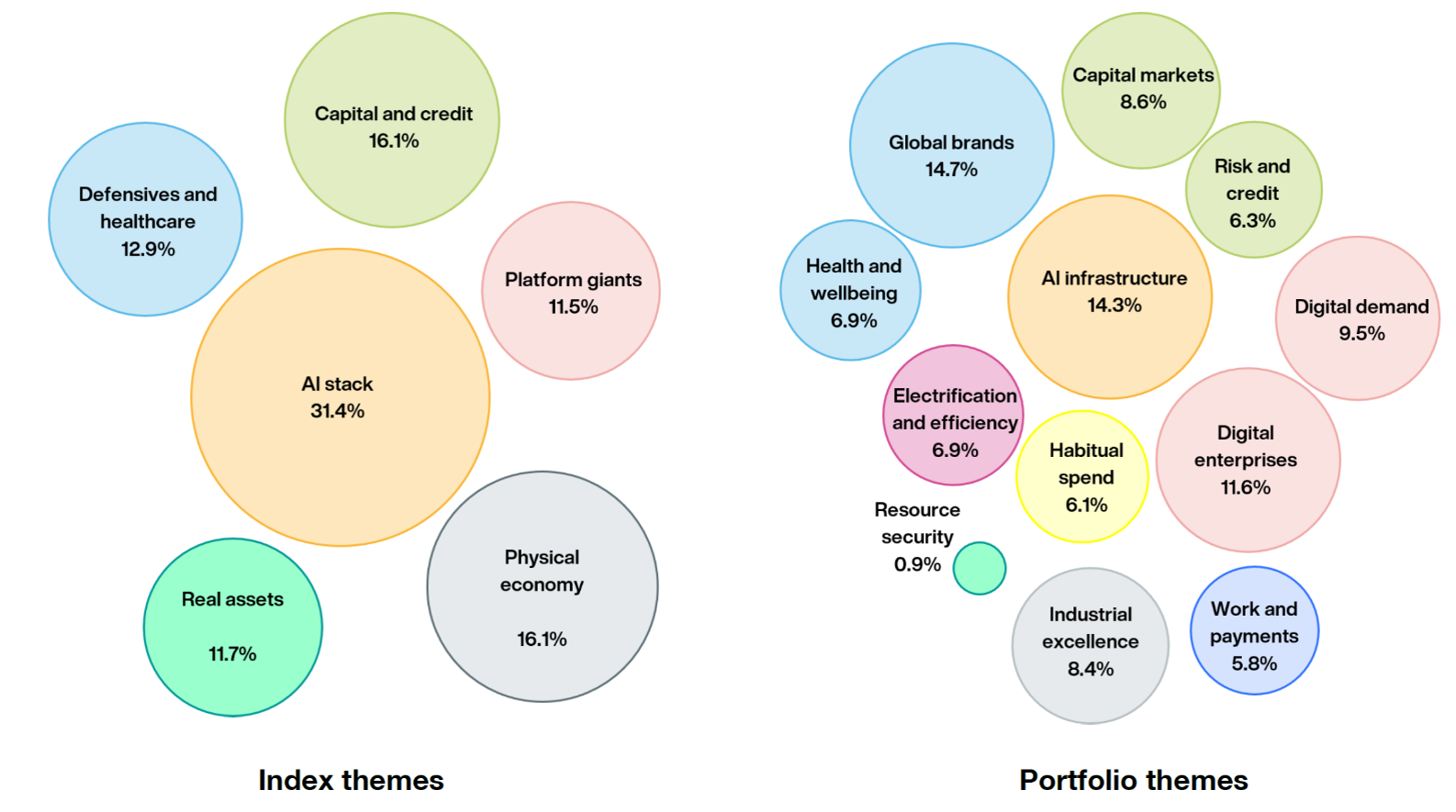

Durable Growth investors believe in a diverse array of growth drivers

Based on ChatGPT view of growth themes present in MSCI ACWI and a representative Durable Growth portfolio as at 31 May 2026. Bubble size represents portfolio/index weight; each holding assigned to one primary theme.

This is a contrasting picture, and one we see as a significant and persistent dislocation. Passive flows can make such dislocations last longer than they used to, but they also make inefficiencies more pronounced. For those with the institutional discipline and intestinal fortitude to stick to their long-term approach, the rewards from exploiting these inefficiencies could be great, not least because momentum-driven markets can fall as far and as fast as they have risen.

How our beliefs have fared

This quarter was certainly a test of that fortitude. While we saw continued operational progress from our holdings, the portfolio endured a gruesome derating worthy of a place in one of Ripley’s exhibits. Good growth in earnings and dividends was offset by falling valuations. Again, this fits the pattern of 2025, when double-digit earnings growth met a double-digit decline in valuations. Meanwhile, the index’s similar levels of growth were rewarded with expanding valuations. This difference explains the vast majority of our underperformance in the year so far, as it did last year.

The derating was most savage in the software sector, where once-envied per-seat subscription models are being questioned in light of AI agents occupying no seats at all. Intuit continues to make strong operational progress, even as the market worries that AI could disrupt its tax business. Most of the company is performing well, with particularly good momentum in its small business and assisted tax offerings. The sole area of weakness is among lower-income, price-sensitive customers using the self-file version of TurboTax, where Intuit has lost some share. This, together with a sizeable reduction in headcount, has reinforced concerns that the company may be cutting costs to defend itself from AI-led competition.

We think that interpretation is too pessimistic. Intuit’s restructuring appears more focused on simplifying the organisation, reducing duplication and redirecting investment towards its highest return opportunities. More importantly, AI is already helping the company improve its products – guiding tax customers to the right human expert, reducing the administrative burden on those experts, and helping small businesses make better financial decisions. Rather than seeing Intuit as a casualty of AI, we believe it is using it to strengthen its existing advantages.

Accenture faces a similar market narrative. Results announced in May showed earnings growth of 9 percent and a dividend increase of 10 percent, yet AI disruption fears persist and the shares now trade on an undemanding nine times next year’s earnings. In hindsight, we bought in too early, but we still believe consulting will survive the AI revolution and that Accenture will be central to spreading its benefits through the corporate world.

We have been here before. Novo Nordisk and Edenred, both under intense scrutiny in recent years, were among the top contributors this quarter as sentiment began to recover. Operational progress for both has continued throughout; only the market’s feeling towards them has changed.

Of course, there will always be instances where negative sentiment correctly reflects a deterioration in a company’s fundamentals. In the case of CME, the Chicago-based derivatives marketplace, this comes in the form of a more complicated relationship with its regulator. When we first invested, one of CME’s key strengths was its close ties with the Commodity Futures Trading Commission, the CFTC. This has deteriorated quickly, as the current administration has moved to replace CFTC executives with individuals sympathetic to new rules on polymarkets and cryptocurrencies. This is a significantly negative development for CME’s competitive position and we have moved quickly to sell the holding.

Deratings and analytical errors are painful, but missed growth is perhaps the hardest thing for an equity investor to take. Our aversion to deeply cyclical stocks meant we sat on the sidelines as memory stocks SK Hynix and Micron surged as investors searched for the next AI bottleneck. Together, these omissions cost more than 1.5 percent of relative performance.

Our own chip names more than offset this headwind, though. TSMC and Mediatek were top contributors to relative returns. Mediatek is a good example of our desire to invest where we have an uncommon understanding. When we took a holding in the fourth quarter of 2025, the valuation reflected uncertainty over how material its nascent custom AI chip business could be for a company best known for lagging-edge hardware in mobile phones. Now, with its deep involvement in Google’s TPU project, MediaTek is forecasting $2bn in sales from its custom AI chips in 2026, followed by rapid growth in the years beyond. With consensus expectations exceeded, the share price rose precipitously.

Testing our beliefs

At one point, Robert Ripley’s volume of inbound mail was second only to the US president. He built the “Believe It or Not!” brand by challenging readers to look at the evidence and tell him what they saw; and challenge him they did.

We try to apply the same challenge to the companies we own. Twice a year, we force ourselves to confront the evidence, testing whether the beliefs that led us to invest still hold. This quarter, we completed two such exercises: our Quality Growth Review and our Dividend Hall of Shame.

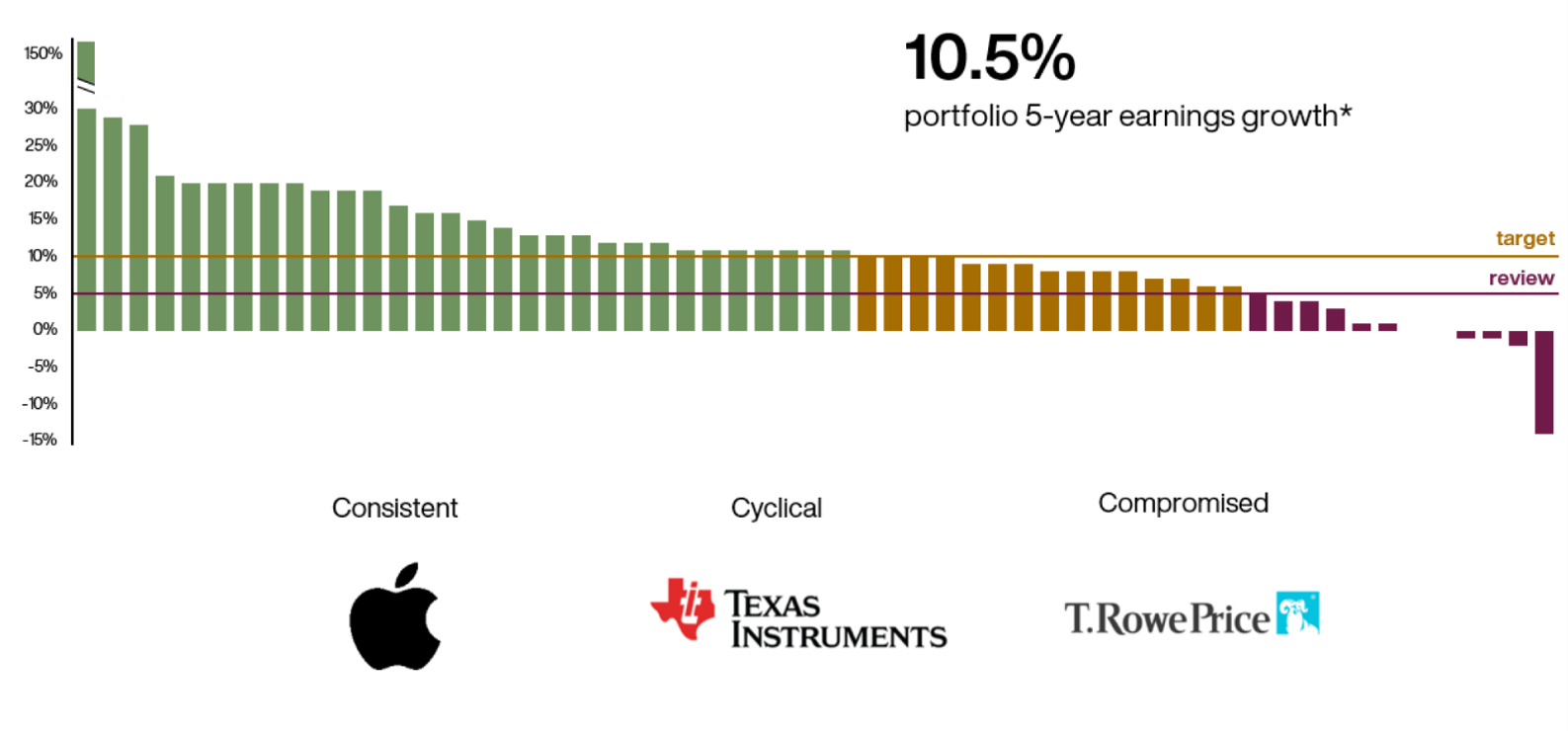

The Quality Growth Review is our annual audit of whether the companies in the portfolio are actually doing what we bought them to do. We strip out FX tailwinds, disposal gains, tax wheezes and accounting oddities, then stack every holding by clean EPS growth over one, five and ten years against the 10 percent earnings growth we seek from the portfolio.

This exercise is designed to make us uncomfortable. The portfolio-level result was reassuring – five-year earnings growth remains around our 10 percent target. But that average contains a wide spread of experience: some holdings have compounded earnings well above our hurdle, some are in cyclical troughs, while others deserve more attention.

For those in the middle ground, we must ask: is this compounding interrupted or compounding disrupted? Is there evidence of acceleration, or are we just hoping for it? Does the valuation give us enough compensation to wait, or are we tying up clients’ capital in a dull exhibit with no potential value? This is very different from defending a prior decision. It is a fresh assessment: would we buy this today, knowing what we now know?

In one case this quarter, the answer was an unambiguous no. When we first invested in T. Rowe Price, we admired its culture of long-termism and its genuine commitment to client service. But the structural shift towards passive alternatives has proven more relentless than we anticipated, fee pressure has shown no sign of abating, and outflows have continued to compound the problem. The world has changed for asset managers and T. Rowe has not kept pace with it. We sold the position and have reinvested the proceeds elsewhere.

5-year clean EPS growth ranked by holding

5 year EPS CAGR stripped of FX, disposals and tax effects. Source: Annual Results Review 2026. 5 years to 31 December 2025. In US Dollar. T.Rowe Price no longer held. *Source: FactSet. As at 31 May 2026. In US Dollar. Based on a Global Income Growth portfolio, representative of the Durable Growth team.

The Dividend Hall of Shame is exactly as glamorous as it sounds. Ripley’s Odditoriums have shrunken heads and two-headed calves; ours has dividend cuts, cash-flow cover and uncomfortable minutes from old stock discussions. It asks whether we correctly assessed the resilience of income our clients depend upon.

Last year, only three of our approximately sixty holdings cut their dividends. Two of those – UOB and MediaTek – were holdings we had correctly identified as carrying meaningful dividend risk at the time of purchase. The Diageo post-mortem was uncomfortable because the warning signs were not invisible. We put too much weight on willingness to pay – the 25-year progressive dividend record and management’s commitment to it – and not enough on ability to pay. Free cash flow had weakened, working capital was more demanding and capex was rising as the company built out Guinness capacity in response to millions of twenty-somethings attempting to ‘split the G’. In plain terms, the dividend looked affordable on earnings, but much less so on cash.

That lesson matters beyond one holding. We are changing the way we assess dividend resilience so that free cash flow cover carries more weight than accounting earnings. We are also trying to make our GRIT scores less static. A major profit warning, a CFO change or the arrival of a new chief executive should not just prompt a news update. It should force us to ask whether the original growth, resilience and income judgments still hold.

None of this is pleasant. A good quarterly letter would ideally contain only charming curiosities: businesses compounding, dividends growing, clients rewarded. But a portfolio manager who only collects flattering evidence eventually becomes another oddity. It is good discipline to keep a cabinet for the disappointments too - to label them clearly, study them carefully and remove them only when the lesson has been learned.

Expanding our range of beliefs

As we weed out poor performers, we aim to replace them with holdings that broaden the portfolio’s range of growth drivers. In recent times, thematic exposures have made our stock-picking ability invisible. We have been deliberate in addressing this, seeking to ensure that our relative performance reflects the quality of our ideas rather than unintended concentrations.

This is not about hugging the benchmark, but thoughtful diversification of growth sources so that the portfolio can compound in more than one scenario. This quarter, that included the addition of a second bank to the portfolio, Cullen/Frost Bankers.

Most banks are poorly suited to our approach. They are typically highly leveraged, deeply cyclical, sensitive to interest rates and regulation, and vulnerable to crises of confidence – in short, not in control of their own destiny. That belief holds in general. But in any sector, however challenging, there exist rare businesses whose culture, strategy and competitive position grant them an unusual degree of self-determination. Cullen Frost is such a company.

Founded in 1868 and still only on its seventh CEO, Cullen Frost operates a relationship-led model in Texas – a state that would be the world’s eighth-largest economy if it were standalone. Its Net Promoter Score is the joint highest among the top 50 US banks and it has grown its branch network 50 percent since 2018 through organic expansion into Austin and Dallas.

Its deposit franchise is extraordinary. Customers accept meaningfully lower rates because they value the relationship they have with their contact, giving Cullen Frost a structural funding advantage that is more valuable in a higher-rate world. The bank has never made a transformative acquisition, which means its data and technology estate is unusually clean, a genuine advantage as the industry deploys AI. Its credit discipline, demonstrated through multiple Texas energy busts and the 2023 regional banking crisis, gives us confidence in its resilience through cycles.

We have been candid that our emphasis on resilience and downside protection has come at a cost in rising markets. Adding Cullen Frost is one of several steps to broaden the drivers of growth in the portfolio. It should be seen not as a bet on banks but as a bet on a specific business whose conservative management, organic growth strategy and deposit moat we believe can compound book value at high single digits with less downside risk than peers. We believe there are opportunities like this in every sector, and we intend to keep finding them.

Why we still believe

The market’s current oddities should not obscure the uncomfortable truth that applying these beliefs has cost our clients — perhaps not in absolute terms, but certainly in opportunity cost. Relative returns over the past two years have been poor. When a small number of companies account for an ever-larger share of the index, any diversified portfolio will struggle to keep pace. We know we are testing your belief in us.

But the belief embedded in today’s index prices also deserves scrutiny. Valuations do not look obviously stretched by historical standards because the denominator — expected earnings — has grown enormously. The market is now pricing in a world where artificial intelligence powers corporate earnings growth of more than 20 percent next year, more than double the 8 percent rate achieved over the last century. In plain terms, that means people losing their jobs to machines so that company margins can expand. Whether this is technologically achievable remains debatable. Whether it is socially and politically palatable is, we think, the more important question.

You hired a manager to question these market beliefs and invest your capital prudently. One that would not abandon its own beliefs just as they were being tested, exchanging a diversified portfolio of dependable growth companies for a narrower expression of the market’s prevailing enthusiasms. We will keep testing our own assumptions, learning from mistakes, and broadening the portfolio’s sources of growth as markets change. And we will position the portfolio for outperformance not over a quarter, but over a decade, by investing in businesses that can compound steadily and provide resilience when markets become less forgiving.

In a market that increasingly asks investors to accept the strange as normal, the right response is not to suspend disbelief. It is to keep returning to the evidence: the growth of the companies we own, the dividends they pay, the resilience they demonstrate, and the discipline with which we respond when our own assumptions are tested. Those are the things by which we ask to be judged. And on that basis, we believe as strongly as ever in the portfolio we manage for you.

Global Income Growth

Annual past performance to 30 June each year (%)

| 2022 | 2023 | 2024 | 2025 | 2026 | |

| Global Income Growth Composite (gross) | -1.9 | 13.1 | 11.0 | 0.5 | 6.2 |

| Global Income Growth Composite (net) | -2.4 | 12.4 | 10.4 | -0.1 | 5.6 |

| Responsible Global Equity Income Composite (gross) | -1.2 | 14.9 | 12.9 | -0.2 | 7.2 |

| Responsible Global Equity Income Composite (net) | -1.8 | 14.3 | 12.2 | -0.8 | 6.6 |

| MSCI ACWI Index | -3.7 | 11.9 | 20.6 | 7.6 | 28.2 |

Annualised returns to 30 June 2026 (%)

| 1 year | 5 years | 10 years | Since inception* | |

| Global Income Growth Composite (gross) | 6.2 | 5.6 | 10.1 | N/A |

| Global Income Growth Composite (net) | 5.6 | 5.0 | 9.5 | N/A |

| Responsible Global Equity Income Composite (gross) | 7.2 | 6.5 | N/A | 10.9 |

| Responsible Global Equity Income Composite (net) | 6.6 | 5.9 | N/A | 10.3 |

| MSCI ACWI Index | 28.2 | 12.4 | 13.4 | 14.5 |

*Inception date for Responsible Global Equity Income: 31 December 2018.

Source: Revolution, MSCI. GBP. Net returns have been calculated by reducing the gross return by the highest annual management fee for the composite. 1 year figures are not annualised.

Past performance is not a guide to future returns.

Legal notice: MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, endorsed, reviewed or produced by MSCI. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Risk factors

The views expressed should not be considered as advice or a recommendation to buy, sell or hold a particular investment. They reflect opinion and should not be taken as statements of fact nor should any reliance be placed on them when making investment decisions.

This communication was produced and approved in June 2026 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

Potential for Profit and Loss

All investment strategies have the potential for profit and loss, your or your clients’ capital may be at risk. Past performance is not a guide to future returns.

This communication contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research, but is classified as advertising under Art 68 of the Financial Services Act (‘FinSA’) and Baillie Gifford and its staff may have dealt in the investments concerned.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this communication are for illustrative purposes only.

Important Information

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). Baillie Gifford & Co Limited is an Authorised Corporate Director of OEICs.

Baillie Gifford Overseas Limited provides investment management and advisory services to non-UK Professional/Institutional clients only. Baillie Gifford Overseas Limited is wholly owned by Baillie Gifford & Co. Baillie Gifford & Co and Baillie Gifford Overseas Limited are authorised and regulated by the FCA in the UK.

Persons resident or domiciled outside the UK should consult with their professional advisers as to whether they require any governmental or other consents in order to enable them to invest, and with their tax advisers for advice relevant to their own particular circumstances.

Financial Intermediaries

This communication is suitable for use of financial intermediaries. Financial intermediaries are solely responsible for any further distribution and Baillie Gifford takes no responsibility for the reliance on this document by any other person who did not receive this document directly from Baillie Gifford.

200901 10064115