Key points

- EWIT’s unique portfolio offers access to high-potential assets from both public and private markets

- Recent process improvements and strategic adjustments mean EWIT is well-positioned for future growth.

- Voting against the proposed actions is crucial to retain the upside potential and enable shareholders to benefit from the next technological supercycle

Dear valued shareholders,

We are writing to ensure you have the information you need to act in your best interests. A specific shareholder is questioning the premise and potentially altering Edinburgh Worldwide Investment Trust (EWIT)’s ability to deliver on your investment expectations.

To help you respond and cast your vote, we wish to remind you of EWIT’s rich history, guiding philosophy and purpose, and why they are set to pay off handsomely for shareholders in the years ahead.

EWIT’s portfolio is unique, featuring a diverse range of early-stage but high-potential assets from both public and private markets. These private market opportunities are notoriously difficult for everyday investors to access cost-effectively. But through EWIT, you have a front-row seat to the companies shaping tomorrow. There’s simply no other investment opportunity quite like it in the UK.

Therefore, we strongly encourage you to vote for your shares at the upcoming meeting so that you can retain access to the potential we see ahead.

A timeless philosophy

Five foundational beliefs have underpinned EWIT’s investment philosophy and approach since 2014. These are:

- Innovation and technological progress are the strongest compounding forces that drive society and stock markets forward over the long term

- The greatest changes and innovations start small. Some of the greatest returns, therefore, accrue to innovative problem-solving companies that originate lower down the market cap scale.

- The results of human ingenuity and entrepreneurial flair do not manifest themselves predictably or linearly. Thoughtful long-termism and a willingness to tolerate uncertainty are key to unlocking them.

- These latter attributes are increasingly in short supply in modern equity markets. Patient investors can exploit this growing market inefficiency.

- Further down the market capitalisation spectrum, a higher-than-average individual failure rate is expected. But when technological progress, commercial execution, and profound scalable opportunities combine, the outcomes can be spectacular and the rewards enormous.

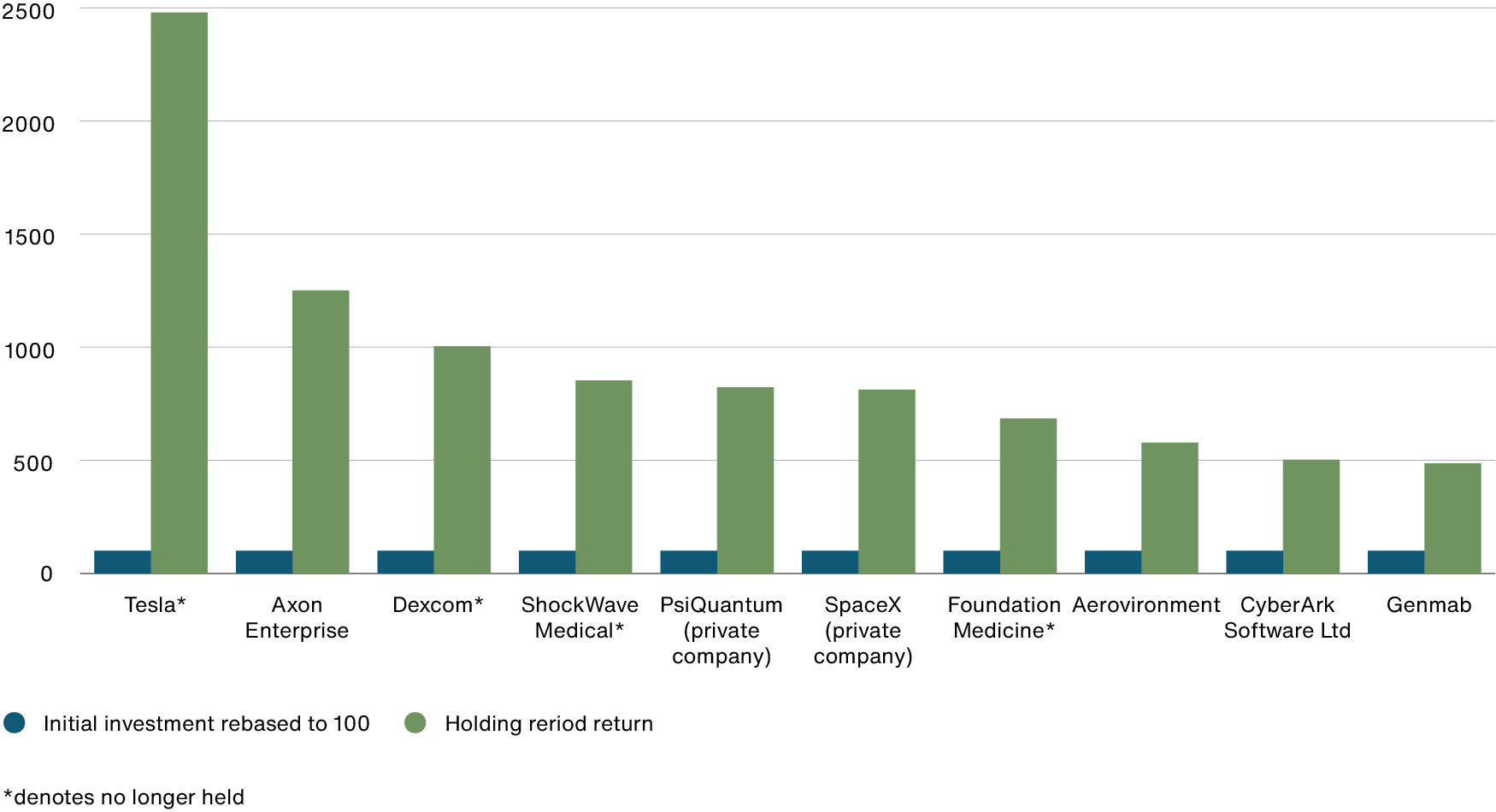

A track record of identifying outstanding investment opportunities

Source: Revolution. Sterling. From 31 January 2014 to 31 December 2024.

Recent performance

We believe in our foundational beliefs more strongly than ever. The inefficiencies we can exploit as stock pickers in public and private markets are increasing. However, recent years have presented a challenging backdrop for EWIT’s philosophy and approach.

The global pandemic directly led to an abrupt rise in inflation and interest rates. While these impacted the business environment and equity valuations broadly, they hit the earliest-stage companies most acutely. Our deliberate and structural skew towards immature businesses building for the future was deeply out of sync with a stock market that craved near-term cashflows and predictability.

We acknowledge some mistakes in execution. It is essential to be upfront about this. EWIT’s shareholders have seen highs and lows over the past decade, and we recognise how frustrating the past three years of poor performance have been for shareholders.

We have learnt important lessons and, over the past year, sought to apply these to our investment processes and portfolio management, with the crucial challenge and support of the Board.

As such, we have improved our ability to patiently support management teams while holding them accountable for strong execution. We have introduced additional process checks and balances to ensure that patience doesn’t stretch too far for holdings encountering a bumpy ride. This affects how we size portfolio positions and time their eventual exits.

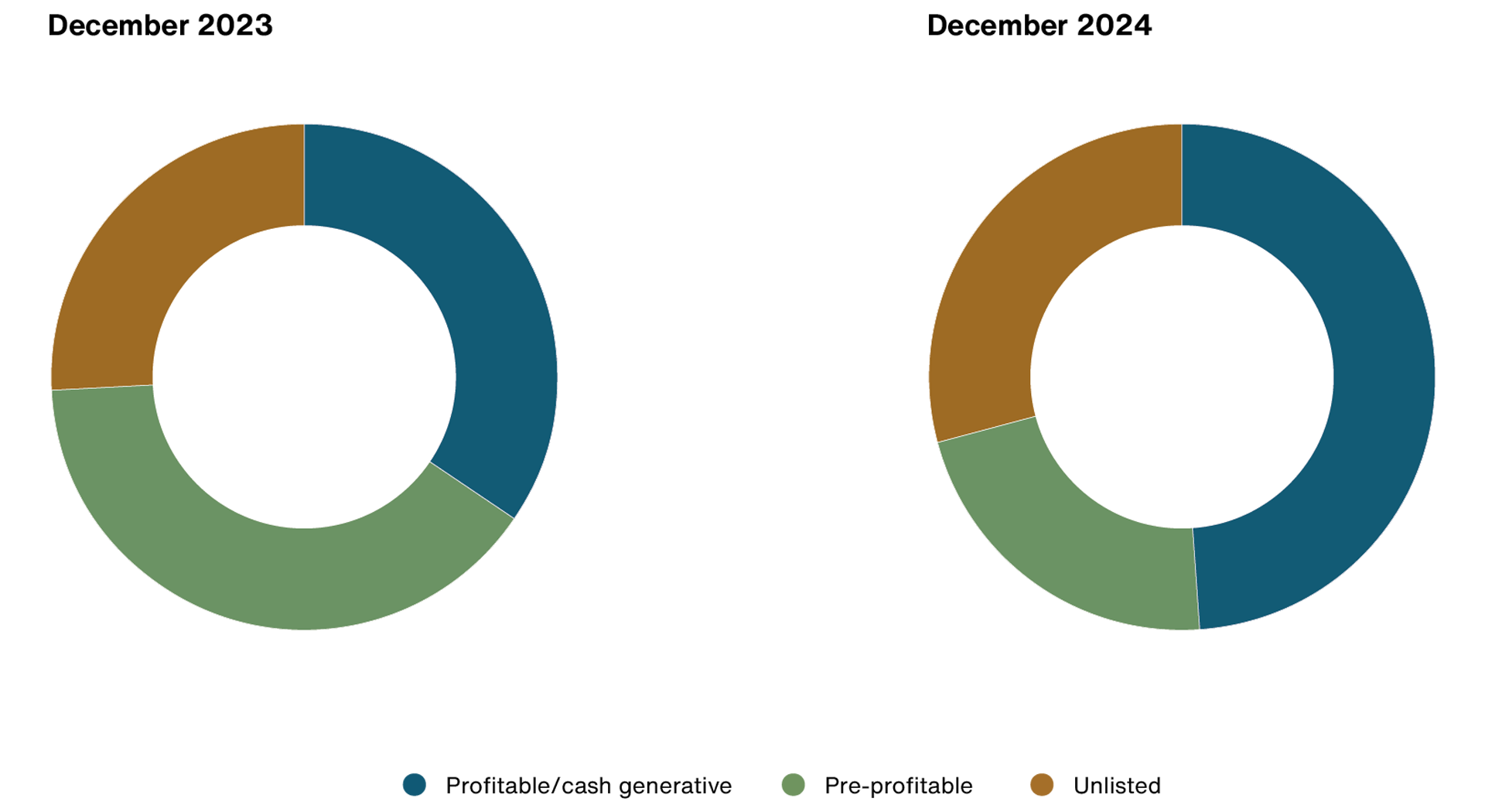

We have also sought to increase the share of profitable, cash-generating names in the portfolio and bolster industrial diversification to reflect the investment environment we anticipate in the years ahead. This has resulted in a better-balanced portfolio with stronger sales and earnings growth.

Source: Baillie Gifford.

The corner has been turned

Recent investment performance has stabilised. We believe that 2024 will prove to be a significant turning point for EWIT. Combined with our enduring enthusiasm for our mission, we’re energised by a sense that we are entering a new period for returns.

Past performance - 1 July 2024 to 31 December 2024

| Share Price | Net Asset Value | Index (S&P Global Small Cap) | |

| EWIT | +32.2% | +16.1% | +7.0% |

Source: Morningstar, S&P. Share price, total return. As at 31 December 2024.

Past performance is not a guide to future returns.

There are two key signs that the headwinds of previous years are falling away.

- The portfolio’s top-line growth has meaningfully accelerated over the past year and is set to accelerate further. This is in contrast to the broader smaller companies market. After a challenging 2023, many of our holdings have adapted and are now re-prioritising expansion. We’ve moved on from several holdings that weren’t meeting our expectations. Independent forecasts estimate that our holdings will grow their earnings at more than 20 per cent over the next three years, which is more than double the benchmark rate. And frankly, we believe that is conservative. These numbers, however, don’t fully capture the portfolio’s considerable growth potential. It feels primed for an exciting period, with our relatively more developed companies now hitting their stride and a wave of newly incubated ideas set to hatch.

- Portfolio valuations remain attractive. Following the turbulence of recent years, the small-cap asset class continues to trade on a significant discount relative to its long-term average and larger peers. Our portfolio has not been immune to this trend, with valuation metrics comfortably below the average level of the past few years. While we cannot accurately predict the trigger for this to unwind and normalise, there are early signals that investor appetite towards neglected opportunities at lower market cap scale is being restored, especially as many countries begin to ease interest rates. This trend has much further to go and would prove a helpful tailwind.

It would be a travesty for shareholders who have patiently held the course through such a challenging period to have the upside potential from this starting point taken from them through the proposed shareholder actions.

The moment of opportunity

Consider this: Do you believe smaller companies will stop innovating over the next decade? Do you imagine all the world’s largest companies will be the same in ten years, or can you see initially smaller challengers emerging to disrupt their dominance?

The world undoubtedly faces challenges in the coming years. Heightened geopolitical instability intuitively feels less comfortable to the more harmonious pro-globalisation backdrop we experienced before.

Yet amidst this, we see tremendous opportunity. From precision medicine to leading robotic automation, rocket technology and unlocking the quantum world, we are in the early stages of a golden age of human ingenuity and engineering prowess. The backdrop may be more volatile, but the tools to navigate it are increasingly relevant and applicable. Indeed, we strongly suspect that the dawning realisation of the importance of the next technological supercycle is at the crux of escalating geopolitical rumblings.

- For instance, as recently witnessed in semiconductors and AI processing, there is a growing geopolitical need for primacy in leading-edge capabilities. This extends into areas where technology affects aspects of national and domestic security. This is evident in the portfolio with AeroVironment, Axon and MP Materials reporting acceleration in demand.

- While AI is the topic of the day, we strongly suspect that quantum computing is the next significant breakthrough to unlock computing. Cracking the qubit will enable exponential computational scaling, allowing vast amounts of information to be processed in parallel and solving complex problems that traditional computers can’t. This will transform how we tackle simulation and modelling in every industry. It’s genuinely hard to comprehend the practical impact, but success would make the excitement around AI seem quaint. While this remains early, our large holding in privately held PsiQuantum is at the forefront of making the technology both practical and commercially relevant in a timeframe that we think will surprise many.

- While computing power is the current technology prism for geopolitical squabbles, this will surely shift towards space technology over the coming decade. Developing and maintaining a strategic advantage in the earth’s orbit will become the key military, communications and industrial frontier, with nations and companies all looking to assert dominance. We initially made a private investment in SpaceX in 2018. Despite its progress – it’s already returned almost seven times our initial investment – it feels like it’s approaching the precipice of generalised relevance in multiple domains.

- The healthcare field continues to fascinate and excite. Our advancing understanding of biology, particularly genetics, is kicking off a new wave of treatments and diagnostics that will transform the patient experience and serve a profound societal need. Development timelines are admittedly long, but our experience with Alnylam shows that over time companies and, by extension, their patient shareholders can be rewarded handsomely for the difference their products and services make.

Our ask of you

Your portfolio occupies the frontiers of technology, and we relentlessly pursue invention across asset classes, geographies and sectors. This results in a distinct investment offering that, despite recent challenges, retains enormous long-term relevance. Shareholders will struggle to find similar exposure elsewhere.

Our mission of investing in the next generation of companies is a privilege to which we remain fully committed, personally and professionally. For us, the true spirit of investing isn’t about chasing fleeting pricing anomalies. It’s about participating in long-term structural change and providing capital and support to the founders and innovators with the vision and audacity to drive change.

EWIT offers a rare opportunity to be involved in companies shaping and, ultimately, owning that future. We urge you to vote against the proposals that deny you that chance.

If you agree, please vote your shares accordingly at the upcoming meeting.

Yours faithfully,

Douglas Brodie, Luke Ward and Svetlana Viteva

The Edinburgh Worldwide co-managers

Legal notice

The S&P Global Small Cap Index is a product of S&P Dow Jones Indices LLC, a division of S&P Global, or its affiliates (“SPDJI”). Standard & Poor’s® and S&P® are registered trademarks of Standard & Poor’s Financial Services LLC, a division of S&P Global (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). Neither S&P Dow Jones Indices LLC, Dow Jones Trademark Holdings LLC, their affiliates nor their third party licensors make any representation or warranty, express or implied, as to the ability of any index to accurately represent the asset class or market sector that it purports to represent and neither S&P Dow Jones Indices LLC, Dow Jones Trademark Holdings LLC, their affiliates nor their third party licensors shall have any liability for any errors, omissions, or interruptions of any index or the data included therein.