The debate on the value – or otherwise – of active management has existed since Jack Bogle of Vanguard first invented the passive fund in the 1970s. Incumbents with vested interests on both sides make their own self-serving arguments. On the one hand it’s a zero-sum game and fund manager performance has no persistence, so tracking the market at minimal costs is the only rational approach. On the other hand, there are clear characteristics associated with the few managers that do well, so all it takes to outperform is informed manager selection. Both sides show empirical evidence that proves their point. The real lesson here is that vested interests cloud objectivity.

It is therefore with self-awareness that we once again make the argument for active, and in fact that active equity is becoming more important to achieving good outcomes for the average investor. Readers should rightly be cynical. But our arguments are at least not those we have heard ad nauseam before.

The past few years have seen increasing attempts by regulators and governments to guide capital to where it has the greatest impact on real-world wealth creation and productivity. This is uncontroversial in principle, but in practice has resulted in equating productive capital deployment entirely to private markets. Private markets have a huge role to play, but this narrow interpretation of how our overall financial system works is likely to have unintended negative consequences.

Capital is not in practice deployed by financial market participants. It is deployed by the management of the companies in which we invest. They decide every day how much to spend on capital, training, R&D, marketing and any number of other things. These decisions are what make a business successful or otherwise. Productive investment does not depend on whether a company is public or private, or whether it is funded by primary capital or cash flow; it depends on the ambitions, horizons, capability and choices of management. The role of shareholders – that is, true investors, not speculators – is to identify companies with future potential and then assess, create and enable the conditions in which management can confidently take the decisions that create real long-term value.

Productive investment depends on the ambitions, horizons, capability and choices of management.

Such true investors are sometimes known as ‘quality shareholders’, a phrase which traces its roots back to the 1970s and has become more common again recently as a result of activities such as George Washington University’s Initiative on Quality Shareholders. Quality shareholders are defined as investors who select a small number of companies and invest meaningfully, hold their stakes for considerable periods of time and who are available and willing to engage with managers and boards for consultation if needed.

As assets move into low-cost quantitative and passive investment approaches, and average holding periods reduce to months not years, the influence of quality shareholders in public markets is waning. The deep levels of company-specific knowledge necessary to act as an engaged owner rather than simply a shareholder are not attainable within the economic realities of low-cost investment approaches which hold very large numbers of companies. Thus the supportive conditions for long-term wealth creation are becoming less common, so much so that stock markets are in some places no longer deemed ‘productive’ at all. If this is right it kicks away one of the foundations of our investment system, and it is remarkable that the topic has not had more attention. The good news is it’s not as simple as that. The solution is to switch attention from the artificial public-private divide and instead focus on shareholder-management relationships more generally.

The amount of cash flow available for growth within listed companies dwarfs that of the private markets, and the effectiveness with which it is deployed is central to real-world wealth creation at scale. This is why engaged active management by quality shareholders within listed companies matters. Studies show that there is a clear correlation: the more ‘ownerless’ a company is, the higher the likelihood of earnings manipulation, misalignment of managerial rewards, accounting misconduct and financial fraud.

Markets do not exist in a vacuum. Companies respond to the actions or inactions of shareholders, and the regulatory environment in which they operate, and they adjust their behaviours accordingly. Ambitious growth companies – the very ones that matter most for socially beneficial productivity gains – do not want to be beholden to disengaged short-term shareholders who at best care about quarterly earnings. The lack of quality shareholders isn’t just a problem for systemic capital allocation, it is driving more companies to stay private or even delist, bringing a different set of challenges around which investors are able to participate in economic growth.

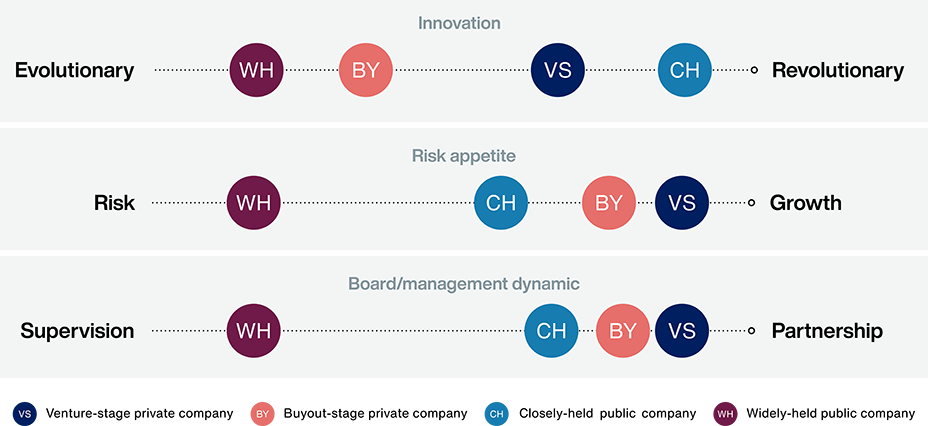

The following graphic is from a study undertaken by a New York-based thinktank, FCLT. It sets out how different companies self-identify in terms of appetite for innovation, risk and shareholder engagement (as represented by the board).

Widely held public companies – those that lack dominant and engaged shareholders – show low appetite for innovation, risk and shareholder engagement. In sharp contrast, closely held public companies – those with a small number of large shareholders who build relationships with management and typically own shares for very long periods (ie quality shareholders) – have much higher appetites for innovation, embrace risk and consider shareholder inputs much more than widely held public companies.

This distinction matters not just for economic productivity but for investment returns. Academic studies show that public companies where management and shareholders have constructive, engaged relationships and long-term alignment outperform those that don’t. What is obvious in private companies is ignored in public ones. It makes little sense that the fundamental oversight and encouragement of thoughtful capital allocation for growth is no longer seen as a pre-requisite for public company investing.

Stock markets were originally created to transform entrepreneurs’ need for long-term capital into a form which matches the liquidity and risk sharing requirements of investors. As the number of participants grew, mechanisms were put in place to enable investors to collectively oversee management, implicitly assuming that they had knowledge to do so. The joint stock company was one of the great enablers of economic growth. It is this system that is now increasingly dysfunctional.

Regulators have also played a role in this. The obligations attached to public-company status have become more extensive, with the fixed costs of disclosure, governance, controls and compliance weighing most heavily on smaller and younger companies.

Where does this end? I believe there are a number of likely unintended consequences. Firstly, as companies – particularly growth companies – stay in private markets, so they become less accessible to individual investors. Various fund structures are being created to partially address this, but a decreasing share of economic growth is available to those who are uncomfortable with reduced liquidity. Secondly, as quality shareholders diminish as a proportion of investors, the effectiveness of the financial system to support good capital deployment within listed companies reduces. The effect is virtually impossible to isolate, but is almost certainly significantly negative for society-wide productivity gains and listed company returns. Passive investors will track the index, but index returns will be lower. Not everyone can be a free-rider. Thirdly, the fees associated with accessing private companies are much higher even than active stock selection and high engagement approaches to investing in public companies. As growth concentrates in private markets, the cost of investment return per unit may well, counter-intuitively, go up rather than down.

Not everyone can be a free-rider.

None of this is to suggest that private markets do not play a crucial role in facilitating the funding of innovation and growth. They clearly do. Many of the best growth companies are to be found there and we invest in some of them. Rather, it is a plea to understand the consequences of letting the public equity system fail. This will come with serious consequences for growth and prosperity. Equity market returns don’t just happen in a vacuum. They are the product of a system of investor oversight and engagement that must be adequately resourced. Ignoring this will cost us all in the end.