As with any investment, your capital may be at risk.

We are stock pickers, but every now and then, it’s worth commenting on the bigger picture. Markets have been ebullient in recent months but skittish this year. We’ve faced war and, hopefully, some rapprochement in the Middle East. We’re experiencing a fracturing of geopolitics. The rulebook of the global economic order has been ripped up.

AI’s endless rapacity is ripping up markets, too. The SaaSpocalypse has spooked investors, causing the share prices of software-as-a-service companies to drop thanks to AI’s increasing ability to replace the tools and information processing they provide. Excitement abounds for blockbuster IPOs from companies whose technology seemed like science fiction less than a decade ago.

This follows 2025, a year in which a narrow range of AI names and cyclicals, including commodities and banks, led market returns. Meanwhile, quality growth de-rated sharply, its worst performance in nearly 30 years. We’ve seen this before. Emerging markets (EM), incidentally, have done well – perhaps the structural beneficiaries of a changing world order?

All this tumult is playing out against a very different market backdrop. Participation in stock markets has markedly changed: retail, short-term actors and passive funds now command a far greater share of market flows. And this is amplifying volatility significantly. It also presents a massive opportunity for smart and patient investors.

For their shortsighted – or perhaps faint-hearted – counterparts, it doesn’t look like a great time for long-term growth. But here’s the thing: we’ve been through choppy market cycles before. We know that if you combine an ability to see the signal through the noise, adapt to remain relevant, and, all the while, retain an enduring search for underappreciated growth, great returns should follow.

Given all that is unfolding, you might well ask us how on earth a long-term investor should navigate this brave new world. In this paper, we explore:

- Growth now – how short-term market distortions are playing out and what matters to long-term investors

- Growth then – what we have learned from a century of investment and how we are adapting to fundamental changes in the economic order

- Growth always – why our fundamental, long-term growth style remains well-positioned to deliver for clients who want to grow their capital

Growth now: hear Kitty roar

Markets have always been noisy. But the noise right now is louder than normal, and share prices are swinging about wildly. That is partly being driven by some fundamental changes to the landscape for growth companies, which we explore below in Growth then, but it also reflects changing market participation.

We’ve seen and commented on these dynamics for the better part of the past two decades. Now, we are reaching a tipping point. In 2023, passive equity funds overtook active equivalents, commanding more than half of global assets – just think for a second about the inefficiency that creates. It is now the case that the majority of markets by weight of assets under management (AUM) are commanded by flows that, by definition, follow others’ investments.

The thesis for passive is that it simply benefits from free markets – or gets a free ride. But now we’re seeing more market ownership commanded by short-term hedge funds, quant-driven strategies and, crucially, retail investors.

The newly awakened retail investor can be colourfully characterised by Roaring Kitty (an American whose real name, rather more prosaically, is Keith Gill) of 2021’s GameStop short-squeeze fame, and by Davey Day Trader, the moniker adopted by Dave Portnoy of Barstool Sports. Filming from home, they popularised investment as a form of sport during the pandemic. Droves of Reddit bros follow them, working together on the platform (in which we own shares) to get one up on Wall Street.

Roaring Kitty, Keith Gill

These investors now trade friction-free thanks to Robinhood’s widely used commission-free trading app, and they are prepared to make some punchy options-based bets to make a buck and have some fun along the way. Their investment horizon is 24 hours.

Between 2010 and 2025, roughly 10 percentage points of US equity trading volume shifted from institutional to retail investors – effectively a 20-percentage-point swing in their relative share. This trend will continue thanks to tokenisation, an even easier way for individuals to participate in and speculate on markets.

The passives – those following retail and technical investors – increase those investors’ influence dramatically, on a short-term view. This dynamic creates clear mispricing as share prices swing from day to day.

There has been a sharp surge in US equity market trading volumes, with equity turnover averaging more than a record $1tn per day in January, a nearly 50 percent increase from the same month in 2025. On a global basis, there are far more violent daily swings. The number of days when market returns have moved by more than two or three times January 2025’s daily average has increased. Short-term moves are becoming ever wilder. Stock markets have always reacted to short-term narratives. But the speed of transmission – and the distortion that comes with it – is growing.

Baillie Gifford might seem a rather quaint relic in this new world of fast markets and flash boys. But here’s the thing: we’ve been doing this for more than a century, we’ve adapted many times before, and we are doing so again. While some things change, such as the nature of growth or the precise nature of the inefficiency we’re trying to beat, some things don’t: impatience and a lack of imagination around exceptional growth lead to clearly exploitable inefficiencies.

Growth then: learning from the past century, always adapting

To find future growth, you have to learn from the past. That means recognising familiar patterns, but also recognising what is really different this time.

Let’s start by examining the familiar patterns. Well, we’ve seen a sell-off of many growth companies. It’s not the first time. The dotcom bust and the financial crisis gave rise to similar dynamics: growth temporarily fell out of favour, markets were volatile, and there was a flight to ‘safe, tangible’ assets. But share prices ultimately reconnected with fundamental growth, and the companies that delivered strong earnings outperformed on a five-year view. The trick is to use volatility to your advantage, and we’ve been doing that recently, adding attractive oversold positions across our portfolios.

We know how to do this because Baillie Gifford sits on a foundation of learning dating back more than 100 years (incidentally, only one in 10,000 listed companies survives that long). This depth of experience gives us valuable institutional knowledge for navigating paradigm shifts. Few investment houses can say the same.

Our roots are in the rubber plantations that boomed in the early 20th century as the motor car revolutionised transport. In the early 2000s, our portfolios delivered for clients thanks to the winners of the internet revolution and our exposure to the commodities supercycle that massive investment in Chinese infrastructure drove. We have always adapted.

So if market patterns are familiar (if more extreme), what is different? Two things: the backdrop has changed (with implications for where to find growth) and AI.

Companies have had to navigate more change post-pandemic than in the better part of two decades before it. Pre-Covid, conditions were relatively stable: capital was cheap and abundant, geopolitics was benign (with some straws in the wind), and technological innovation was advancing. That period, the seeds of which were sown 15 years earlier in the dotcom era, furnished us with capital-light technology platforms operating across a range of industries that delivered extremely attractive returns and increasing returns to scale. It was a transformative period for growth investors.

Even so, adding value as active managers was not easy. For every Amazon, there was a Cisco. But there was certainly a more stable operating environment for companies, and there was clear market momentum.

Today, the backdrop is different. The cost of capital is higher, and it’s less available. Geopolitics has fragmented. The stable and predictable global economic and political order has fractured. Companies – and investors – will need to be more flexible, agile and resilient. Coupled with AI-driven shifts, which we touch on below, the dispersion in fortunes for listed companies may well be greater than in the past (the power law in action, as always), and the winners may emerge from a wider opportunity set.

Two very different recent purchases, both growing far faster than the market.

MiniMax is an AI company that develops models and turns them into products for consumers and businesses. These span chat and agent tools, video, audio, music and tools for developers. We participated in the IPO in January. MiniMax is growing very quickly: revenues rose 159 percent year-over-year.

Ensign is a nursing home operator, serving the US’s growing elderly population. A strong balance sheet and excellent execution give the company an edge in what remains a difficult industry. With only 1-2 percent market share, the opportunity to expand is significant, and the company has delivered on this with earnings that have roughly doubled over five years.

So, we are redoubling our efforts to look for investments that furnish our portfolios with that resilience, adaptability and broader drivers of growth. Set against the changing market dynamics we explored at the outset, this allows us to thoughtfully construct resilient portfolios that can withstand a less certain backdrop and deliver growth. All our investment teams have taken time to reflect on their approach and overall portfolio positioning.

Even more significantly, AI changes everything. This isn’t just Google Search on steroids. AI changes the nature of the operating environment and the competitive dynamics of business. It will change the fabric of society and how we conceive of ourselves. Ironically, in an age of nationalism rather than globalisation, the AI behemoths challenge the very primacy of the nation-state.

We are investing in an entirely different paradigm now. To navigate it successfully, we must think broadly, challenge prior assumptions and expect more disruption. We must also keep a level head and stay the course. This sounds simple, but the discipline to do so is rare.

Despite the current market narrative, not all software companies will be losers – some retain compelling sources of competitive advantage that are underpinned by factors as low-tech as a physical installed base of devices or regulation. This doesn’t faze us. We’re effective at investing on the right side of creative destruction.

Growth always: the fundamentals still work, and we have a growing edge

We wrote earlier that the rewards for those who can withstand short-term volatility will be substantial. Let’s unpick why we know that’s the case.

Great growth companies are more likely to deliver strong long-term returns

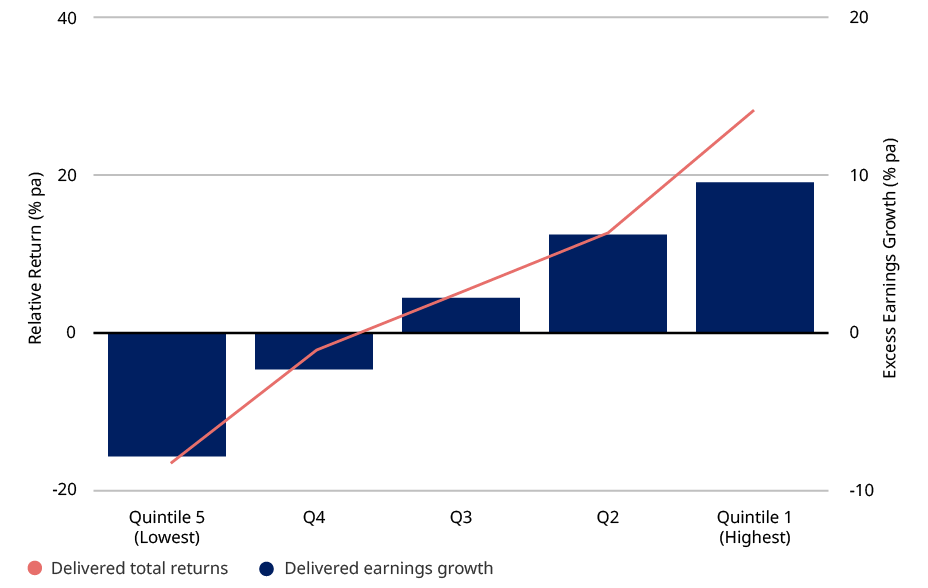

Last year, Tom Slater revisited his paper ‘Blue sky and base rates’ written about a decade earlier, in which he interrogated the pattern of stock market returns. Our work, sustained over decades, shows that returns are not normally distributed. Instead, a small cohort of companies delivers extreme returns. Holding them over the long run is the best way to generate value because of this skew. The graph below illustrates how this pattern remains true:

Stronger earnings growth has driven stronger returns

Rolling five-year horizons (1990-2025)

Source FactSet. MSCI ACWI companies from Dec 1990 to Dec 2025, excluding loss-makers and sub-$1bn market caps. Companies are grouped by earnings-growth quintile, with each quintile’s median share-price return compared with the universe median.

Across the firm, our various investment teams are very clear about which companies they seek to hold. Some look for the 5 percent of companies that could be worth five times as much over five years. Others aim to blend these names with a broader cohort that can roughly double over a similar period, which about a fifth of companies can achieve. Still others aim to deliver more stable returns by focusing on steady, durable growth.

All are looking for exceptional growth and to hold it patiently. As a result, our portfolios rest on strong fundamentals. Short-term traders might be playing sentiment-based chicken, unable to wait for fundamentals to come through. We stand on much firmer foundations.

The market consistently underestimates great growth

Beating the stock market must, by necessity, be a blend of science and art. Thoughtful analysis underpins what we do, but we also need to dare to imagine (or model) significant growth for those truly exceptional companies that can really deliver sustained superior returns. We all know that the future is not simply an extrapolation of the past.

The evidence shows that sell-side analysts are consistently terrible at projecting extreme outcomes. A recent study found that only 17 percent of sell-side analysts publish forecasts looking three years ahead. That may seem surprising to market practitioners, but it highlights the sell-side’s herding mentality.

The market rarely looks far enough ahead

MSCI ACWI: average number of sell-side forward estimates five years from 31 March 2026

TSMC, the semiconductor foundry company, which many Baillie Gifford portfolios hold in size, is a stark example. Of the 35 sell-side analysts who provide forward estimates on the company, just nine look out three years. The pull to mean reversion in estimates remains strong. Indeed, the underestimation of growth in emerging markets is particularly pronounced.

Even when analysts do rate companies a ‘buy’, they tend to significantly undershoot on earnings delivery during growth periods. Consider the chart below. This shows two things: firstly, consensus estimates consistently underestimate earnings growth; secondly, if your time horizon is three months, you miss the long-term compound earnings growth potential. Consensus estimates have been far too conservative. Throughout this period, our clients have benefited from our high-conviction holding.

Short-term noise, long-term compounding

TSMC: estimated earnings per share (quarter-on-quarter change)

TSMC: earnings per share

This is where we seek to provide insight. We don’t try to beat the passive and quant brigades by fiddling with complicated models or making bets on short-term re-ratings.

Over our time horizons, what matters is the ability to predict the scale and probability of future cash flows. Then, being able to assess the difference between our opinions and what’s represented by the market price.

When you walk the floors at Baillie Gifford, you still see analysts from a wide range of backgrounds reading from a wide range of sources with this crystal-clear aim in sight.

We have an informational advantage

In an age of AI, quant models and ever-increasing data transmission, interpersonal connections matter more than ever.

So our access to management gives us an edge – an understanding that cannot be reduced to data points accessible to the outside world. We consider the quality of a management team, the confidence with which it articulates its vision, and its long-term strategy, not just its quarterly guidance.

Baillie Gifford’s reputation as a long-term investor means we don’t just gain access to C-suite executives at listed companies’ investor roadshows (as valuable as those are). We have private face-to-face meetings with the leadership teams driving change and disruption – those creating some of the most exceptional companies in the world, public and private.

We command enviable access to private companies (we get our full allocation in 97 percent of the private equity deals we go in for). And we bring what we learn from conversations with the entrepreneurs who run them to bear on our listed equity portfolios, giving us a more complete picture – one built up over countless interactions and years, not one-off data points. Last year alone, we took more than 5,000 company meetings.

Recent examples with AI-related companies include:

- Time with the chief executive of Horizon Robotics in China, where Dr Kai Yu remarked that “perseverance is the scarce resource in China, not intelligence” (consider that, just for a moment)

- Our meeting with Anthropic, where chief executive Dario Amodei and colleagues spoke to us about their strategic direction

- Our conversation with Demis Hassabis, chief executive of Google’s DeepMind, who discussed both the speed at which AI might develop and the key roadblocks to real artificial general intelligence

Our company meetings, a mainstay of our approach, are a huge source of edge.

Most importantly, we have a behavioural and institutional advantage

Research shows that stocks with a longer-term active institutional shareholder base earn higher subsequent returns than stocks held by myopic institutions. The reason is that short-term incentives create systematic underinvestment and mispricing in firms that require patience to deliver returns.

This inefficiency is driven by myriad incentives for short-termism, from redemption pressure to career risk. Combined with well-documented loss aversion, it makes holding on to a stock – or an active manager – hard when times are tough. Yet the evidence is clear: patient capital is scarce. There is a common mispricing of long-term growth, particularly in volatile companies that are so hard to hold. Those who avoid the common behavioural pitfalls of pro-cyclical investment can exploit this mispricing.

We have a massive structural and behavioural advantage. Our ownership structure and long-term culture mean we can withstand the behavioural shortsightedness that dominates markets. This is not to ignore the lessons of the past, but to underline that we must maintain the discipline to look wrong in the short term in pursuit of capturing the benefits of being right over the long term. That is far easier to write than it is to do, but it remains essential. We retain the fundamental willingness – no, the desire – to be different.

In summary

The short-term noise is getting louder. As tempting as it is to cling to the index, it is increasingly volatile, and the inefficiency it represents is growing. Asset owners should consider whether they want to tether their returns to the quants, passives and retail cowboys who herd around narratives. This creates an even greater opportunity for patient investors.

Baillie Gifford has a century of investment experience, which allows us to learn and adapt and spot the shifts that matter.

In a changing world, our active, long-term approach works. We have an uncommon ability to identify exceptional growth opportunities and gain an edge thanks to our patience and company access. These aspects of our philosophy endure.

We retain the patience to exploit the systematic mispricing of growth and the bravery to be different. We are confident this will underpin strong returns for clients in future.

Future growth

We look forward with great confidence and optimism. Our investment teams remain relentlessly focused on finding the best growth opportunity for clients over the next decade. Below are some of the areas we’re most excited about.

AI, software and hardware

The AI revolution may be the most complex and important call we make over the long run. AI will transform, disrupt, destroy and invent whole new businesses. It may change the very nature of who we are. Market commentary is focused on the disruption of SaaS businesses, and some babies are being thrown out with the bathwater. Some companies have competitive moats that extend beyond their code, while others will be victims. Our US Growth Team explores this here and here.

Looking to the future, we are considering the exciting leaps possible when AI moves from thinking to acting in the physical world through robots and intelligent machines. Explore this here.

Emerging markets in a multipolar world

We are seeing fundamental shifts in geopolitics, ones that may structurally strengthen the prospects for many companies in emerging markets. EM countries are now more resilient than investors assume, with deeper domestic capital markets and less reliance on external dollar funding than in the past. All the while, intra-EM trade is increasing. We see a deep opportunity set that is exposed to structural drivers. Read and hear the thoughts of our EM Team here.

Energy systems in transition

Energy systems are transitioning. Fossil fuels remain an important input for the global economy, and some of our teams have increased their exposure lately. We still see a transition to electrified power systems and renewable energy as a long-term trend. Moreover, datacentres have supercharged this. It’s also playing out in emerging markets, where entirely new energy systems are developing. This is throwing up opportunities. We remain discerning in our search for companies with an enduring edge. Our Positive Change/Climate Future Team has more here.

Physical world bottlenecks

As we question the deep moats that a team of coders automatically conferred upon many software businesses before AI, we also note a world of physical bottlenecks. Energy systems are straining at the seams and commodity demand is growing. Meanwhile, protectionism is increasing. Companies that can address these physical bottlenecks, whether through traditional or novel means, have a significant opportunity.

And, of course, much beyond the above. We hope to continue finding great, idiosyncratic growth companies for your portfolio by following our natural curiosity.

Risk Factors

The views expressed should not be considered as advice or a recommendation to buy, sell or hold a particular investment. They reflect opinion and should not be taken as statements of fact nor should any reliance be placed on them when making investment decisions.

This communication was produced and approved in June 2026 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

Potential for Profit and Loss

All investment strategies have the potential for profit and loss, your or your clients’ capital may be at risk. Past performance is not a guide to future returns.

This communication contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research, but is classified as advertising under Art 68 of the Financial Services Act (‘FinSA’) and Baillie Gifford and its staff may have dealt in the investments concerned.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this communication are for illustrative purposes only.