Key points

- The balance of power in markets is shifting as passive investing, new market participants and investment vehicles reshape short-term price discovery

- For long-term investors, this may mean a more uncomfortable journey, but also greater potential rewards for genuine long-term active management

- The challenge is building portfolios that protect the patience needed for long-term compounding

As with any investment, your capital may be at risk.

There is a paradox at the heart of active fund management. Markets need to be inefficient enough for prices to depart meaningfully from long-term fundamental value, creating opportunities for profitable investment. At the same time, they need to be efficient enough that fundamentals ultimately reassert themselves.

However, this paradox resolves when we view market efficiency as investor behaviour, rather than a mathematical exercise. Markets are neither perfectly efficient nor permanently inefficient. They are adaptive systems, populated by investors with different incentives, constraints, mandates and time horizons.

Over the past decade, the ecosystem of market participants has evolved dramatically. There has been a mass migration of long-term institutional money into passive strategies.

Alongside the high-profile shift from active into passive investment strategies, the investment landscape has fractured with many new participants and investment options emerging and increasing in relative importance. Retail trading platforms, Exchange Traded Funds (ETFs) that package exposures into tradable baskets, hedge fund “pod shops”, and algorithmic-based trading strategies for instance, all account for a much greater share of how money flows into and within markets and have helped make speculation cheaper, easier and faster.

All these instruments and vehicles are becoming increasingly important. While these new channels differ in many ways, collectively they have increased the amount of money allocated for reasons other than fundamental value.

The changing ecosystem of market participants is altering the price discovery process, the mechanism by which markets determine what shares are worth. This is not merely of academic interest, it has two important implications.

First, the same changes that may make markets more prone to dislocations – periods when share prices move far away from a company’s long-term value – may also increase the rewards open to long-term active investors. If more capital is allocated according to rules, flows and narratives, then the opportunity for patient stock pickers may be growing.

The more capital that trades for reasons unrelated to fundamental value, the greater the potential for mispricing – and the larger the potential rewards for investors willing to focus on long-term fundamental value.

The challenge is that ownership of long-term portfolios may become more fragile, as the path of returns can be dominated for uncomfortable periods by flows, factors and narratives. Capturing these opportunities, therefore, increasingly requires portfolios that clients can hold through periods of discomfort, protecting the patience needed for long-term compounding.

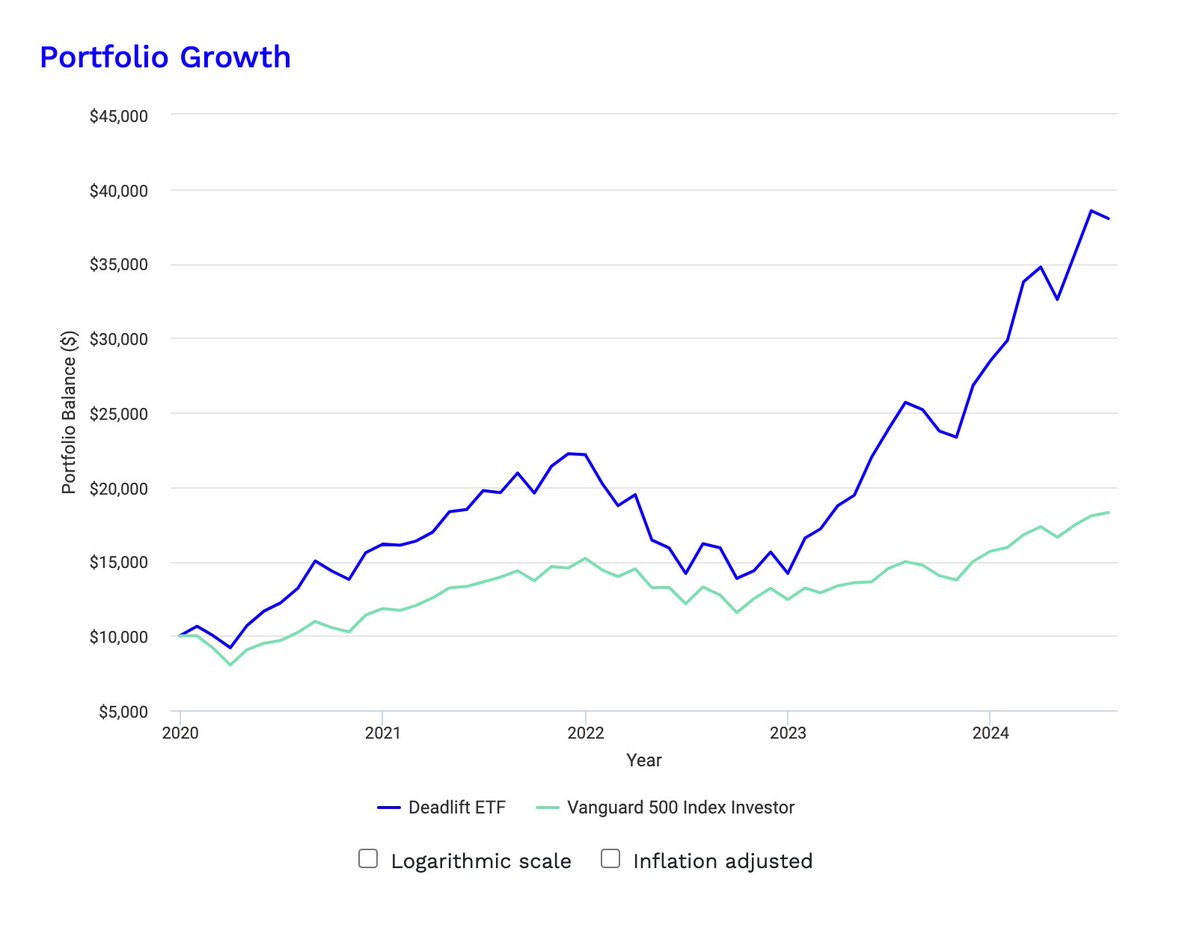

Lifting weights = $$$

The rise of passive investing is perhaps the most visible change. From 2006 to 2025, US-domiciled equity index mutual funds and ETFs recorded roughly $3.2tn in cumulative net inflows, while their active peers recorded almost identical net outflows.

As a result, vehicles which passively track the market have increased from less than a third to more than 60 percent at the end of March this year. With more than $19tn in invested assets, these vehicles now channel far more capital based on rules-based allocation – index membership and benchmark weights – rather than analysis of whether an individual company’s shares are likely to deliver attractive returns.

At the same time, the universe of available ETFs has exploded. Assets allocated to these funds have risen from less than $1tn in 2010 to $13.4tn in 2025. There are now more exchange-traded funds listed in the US than there are individual publicly listed companies.

As recently as 2020, there were only half as many ETFs. Furthermore, many of these ETFs carry significant leverage – borrowing, or the use of financial instruments to magnify gains and losses.

Passive investing often means tracking a broad index. But ETF providers can now quickly create funds that track much narrower themes. This is a new phenomenon: providers can now conceive, name, back-test, package, market and trade new indices almost instantaneously.

For investors who therefore want to take a more active view, ETF providers have become tremendously adept at packaging products to help investors express an almost infinite variety of investment hypotheses.

That this has reached the point of satire is illustrated by the Deadlift ETF. This proposal triggered significant interest when shared online alongside the marketing strapline ‘Lifting weights = $$$.’ The notional basket comprised companies led by chief executives (CEOs) who prioritise physical fitness, weightlifting and combat sports.

🏋️ I made a Deadlift ETF with only companies with CEOs that lift weights or do fight sports (not just cardio)

— @levelsio (@levelsio) August 19, 2024

It outperforms the S&P500 by 140% or 2.4x over the last 4 years!

Lifting weights = $$$

Back-testing showed significant outperformance relative to the S&P 500 over a multi-year period, supporting the view that companies led by well-muscled CEOs are more likely to outgrow the broader market.

The Deadlift ETF is a case of art imitating life, symptomatic of the fact that thematic ETFs of this nature have grown rapidly from a curious niche a decade ago to an allocation method of systemic importance today, amplified by the ease with which these funds can incorporate leverage.

This example also highlights the increasing importance of a compelling narrative. If this has always been true to some extent, what has changed is the speed with which these stories can impact share prices.

In February 2026, a financial research firm published a thought experiment: a fictional memo from June 2028 describing a world in which AI’s success had become economically destabilising. It turned a vague concern about AI’s disruptive potential into a vivid story.

As a result, the report was credited with catalysing heavy selling across software and online or digital companies more broadly, wiping out an estimated $700bn in market capitalisation in the sell-off.

There was no obvious new company-specific information to explain the scale of the move. There were no new company announcements, financial disclosures, accumulated body of economic evidence, or official data releases that established that AI would destroy white-collar employment. The story was enough.

We do not want to make the case that passive investing is bad. Or, that retail investors are the ‘dumb money’ and hedge funds are the Bond villains of modern capitalism. Although note our previous warning that markets dominated by passively allocated capital may suffer from classic free-rider problems, outlined here: Why true active management matters more than ever.

But this changing ecology does suggest strong evidence that the forces pushing prices towards fundamentals have changed. Compared with ten or five years ago, more investment decisions are now driven by index composition, inclusion in thematic baskets, sensitivity to various market factors and dominant market narratives rather than a rigorous assessment of company fundamentals.

Calibrated discomfort – making patience investable

Resilient markets require participants to bring diverse views, time horizons and constraints. Importantly, this ‘wisdom of the crowds’ only works if these views are formed independently of one another.

When views become correlated or more reliant on referencing the behaviour of other market participants, rotations can become more abrupt. Leverage intensifies this process.

The consequence is something of a paradox. Markets may have deep liquidity and be better informed, reflecting access to volumes of information unimaginable in any other era of human history, while simultaneously becoming more prone to episodes in which prices can detach from long-term business value for extended periods.

As a result, the scarce resource in modern markets is not information. It is the combination of analytical and behavioural advantages. As markets become faster, more narrative-driven and less connected to the engaged ownership of individual businesses, the opportunity for long-term stock picking grows.

But so does the difficulty of remaining invested long enough for it to matter. Long-term stock picking may become more valuable, but long-term portfolios become harder to own through the journey.

Both the size and duration of dislocations matter for the client experience. Clients do not experience returns in theoretical five- or ten-year blocks. They experience them quarter by quarter, year by year, through a sequence of uncomfortable decisions about whether to remain invested. The pattern of performance, ‘the ride’, matters in these decisions.

A portfolio may be filled with exceptional companies. However, if its returns are repeatedly overwhelmed by unintended exposure to broad market traits, such as growth, value, size or sensitivity to interest rates, violent style rotations or a single dominant narrative, clients may not remain invested long enough to benefit from the compounding those companies ultimately deliver.

Long-term investing is often described as if patience were simply a matter of temperament or culture. In part, it is. But patience also has to be protected and made behaviourally possible. ‘Don’t just do something, sit there’ is not an easy mantra.

The art of portfolio construction

If patience is becoming both more valuable and harder to maintain, then portfolio construction becomes increasingly important.

Portfolio construction is neither a substitute for stock-picking nor a constraint on ambition. It is there to help clients remain invested long enough to see this ambition rewarded.

The aim is not to reduce active risk or avoid volatility. A genuinely active growth portfolio will always have periods of discomfort. The aim is to ensure the discomfort is attached to the risks we intend to take.

We want more of the portfolio’s risk to come from stock-specific insight and less from accidental exposure to factors that can dominate returns over shorter periods. Investors must endure some volatility because it is the price of long-term excess return, but volatility without purpose erodes trust.

Readers should see the recent evolution of Global Alpha’s portfolio construction in this light. New analytical tools help provide greater awareness of the portfolio’s risk metrics and exposures, and how these are changing over time.

These help us understand how portfolios may perform in different scenarios, such as a sustained period of higher oil prices, or how the sizing of a new holding could shift our upside and downside capture ratios1.

These tools have helped inform our thinking in broadening the forms of growth the portfolio is exposed to. New holdings in banking, energy (where portfolios permit it) and natural resources are more than new sources of return; they change the shape of the portfolio.

This is evident both in the higher number of sectors and industries represented, and in ways that anticipate the pattern of future performance. These changes have helped dampen the predicted volatility profile, while tracking error2 and beta3 have fallen.

Most importantly, we have tilted the portfolio so that stock-picking, rather than factor risk4, is more likely to be the primary driver of returns. This is regardless of which holdings may be packaged into the latest trendy ETF with a great back-tested track record and incredible momentum.

In this sense, broader portfolio construction buys patience. It creates room to continue owning and adding to more controversial ideas when the market’s narrative turns against them. Patience, then, is not passivity or the refusal to change.

It is the willingness to keep underwriting long-term business value while making the portfolio resilient enough to survive the market’s changing short-term behaviour.

What should not change

There is a risk that all this sounds like a call to become more tactical. It is not. The competitive advantage of a genuinely active long-term growth investor remains the ability to underwrite exceptional companies over periods that many market participants find impossible.

As more capital operates on shorter horizons and under tighter constraints, patience itself becomes a scarcer resource. And like most scarce resources, its value rises.

We should be willing to look different because we own companies whose long-term prospects are underappreciated. We should be less willing to look different because of avoidable factor concentrations that neither reflect our best ideas nor improve the probability of long-term outperformance.

In a market ecosystem more prone to volatility and abrupt rotations, the role of portfolio construction is not to smooth away all discomfort. That would be impossible and undesirable. Rather, it is to ensure that the portfolio’s discomfort is purposeful.

The best active portfolios will still feel different. They will still underperform at times. They will still own companies whose futures are uncertain and whose share prices are volatile. But their risk should be intentional, sensibly diversified and connected to long-term return potential.

Markets have always changed – the cast of participants, the vehicles through which capital moves and the technologies that transmit information change.

Today’s market may be more efficient in some ways and less efficient in others. Quarterly earnings can be analysed faster and more thoroughly than ever before, and yet overreact more violently as the direction of initial reactions is amplified.

The challenge is that short-term outcomes may become more volatile, benchmark-relative performance may become more uncomfortable, and factor rotations5 may become more severe.

Long-term active management may become more valuable because genuine patience becomes scarcer precisely when it is most needed.

Long-term stock picking may become more valuable, but long-term portfolios become harder to own. Patience has become more uncomfortable, and therefore more valuable.

1 Upside and downside capture ratios: measure the ratio of the upside and downside of an investment vs a benchmark.

2 Tracking error: a measure in investment guidelines that shows how closely an investment account follows its benchmark index.

3 Beta: indicates how volatile a stock’s price has been in comparison to the market as a whole.

4 Factor risk: the underlying risk exposures that drive the return of an asset class. For example, the return from a share or stock can be broken down into equity market risk – movement within the broad equity market – and company-specific risk.

5 Factor rotations: an active investment strategy where investors dynamically shift their portfolio allocations between different investment styles or "factors" (such as Value, Growth, Momentum, Quality, or Size) based on changing macroeconomic conditions or performance trends

Risk factors

The views expressed should not be considered as advice or a recommendation to buy, sell or hold a particular investment. They reflect opinion and should not be taken as statements of fact nor should any reliance be placed on them when making investment decisions.

This communication was produced and approved in June 2026 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

Potential for profit and loss

All investment strategies have the potential for profit and loss, your or your clients’ capital may be at risk. Past performance is not a guide to future returns.

This communication contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research, but is classified as advertising under Art 68 of the Financial Services Act (‘FinSA’) and Baillie Gifford and its staff may have dealt in the investments concerned.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this communication are for illustrative purposes only.

Important Information

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). Baillie Gifford & Co Limited is an Authorised Corporate Director of OEICs.

Baillie Gifford Overseas Limited provides investment management and advisory services to non-UK Professional/Institutional clients only. Baillie Gifford Overseas Limited is wholly owned by Baillie Gifford & Co. Baillie Gifford & Co and Baillie Gifford Overseas Limited are authorised and regulated by the FCA in the UK.

Persons resident or domiciled outside the UK should consult with their professional advisers as to whether they require any governmental or other consents in order to enable them to invest, and with their tax advisers for advice relevant to their own particular circumstances.

Financial Intermediaries

This communication is suitable for use of financial intermediaries. Financial intermediaries are solely responsible for any further distribution and Baillie Gifford takes no responsibility for the reliance on this document by any other person who did not receive this document directly from Baillie Gifford.

199017 10064074