Key points

- Private markets have grown significantly, with over $10tn in assets under management

- Private growth equity provides the potential for venture-like upside with lower risk, making it an attractive option for DC allocators

- Private companies can invest in long-term growth without the pressure of maximising current cash flow

All investment strategies have the potential for profit and loss, your or your clients’ capital may be at risk.

The recent DC Forum featured a discussion on the opportunities in private growth equity led by investment specialists Rachael Callaghan and Brian Kelly.

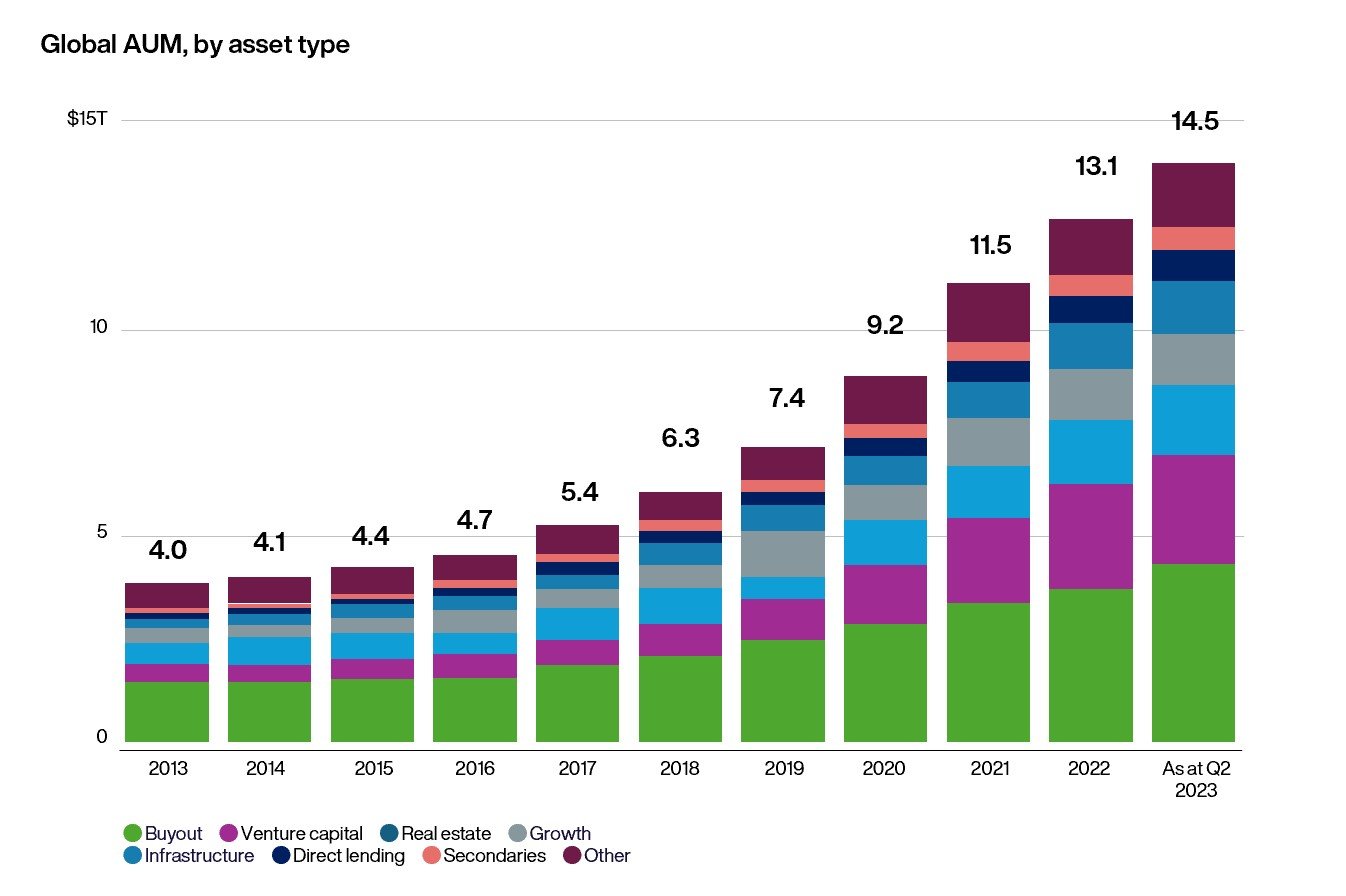

Growth of private markets

Callaghan started the discussion by highlighting the significant growth in private markets. Over the past decade, private markets have seen an increase of over $10tn in assets under management (AUM) and now account for 5 per cent of the investible universe available to allocators.

$10 trillion growth in private market AUM

Notes: Buyout category includes buyout, balanced, coinvestment, and coinvestment multimanager funds; secondaries includes real estate secondaries, infrastructure secondaries, direct secondaries (PE),

and secondaries (PE) fund types; other category includes fund-of-funds, mezzanine, natural resources, hybrid, private investment in public equity, and real assets; excludes distressed private equity.

Source: Preqin. US Dollar.

Drawing on his previous role as an allocator, Kelly provided insights into the challenges they face in public markets, which have driven the shift towards private markets.

He noted that public equities, while historically strong, have become more difficult for allocators whose role it is to diversify. Factors such as the rise of indexation and the subsequent lack of variety in public market portfolios have led investors to search for more diversification and potential returns in private markets.

Durable private market returns

Kelly touched upon the durability of returns in private markets. Unlike public markets, private markets are less affected by indexation. “You can’t index private companies because it is difficult to access, trade, and set a price on them. And so, it’s much harder to build an index,” he said.

He also highlighted that as private companies do not publish their financials, it is harder for quant funds to undertake arbitrage trades, which can lead to higher returns for those who are able to and who are willing to embrace slightly more risk to invest in private markets.

Another feature of private markets is the various building blocks for generating returns, including company formation, operational improvements and financial engineering.

Equity strategies in private markets

Callaghan and Kelly delved into the different equity strategies within private markets, including buyouts, venture capital and growth equity.

Callaghan explained that the defining characteristic of buyouts is control: " Investors take control of companies to break them apart and sell them off or send in operating professionals to improve and fix these businesses.”

This creates an opportunity for those who wish to invest in those companies that want to remain “standalone, independent companies.” Epic Games, for example, has remained a private company for 30 years despite the success of its Fortnite game.

She indicated early-stage venture capital was “your Silicon Valley stereotype: ‘two people, a garage, a god and an idea.” The term ‘unicorn’ was coined in 2013 to reflect the rarity of private companies valued at over $1bn, but this rarity is no longer true with over 1,500 unicorns today.

As a result, companies are outgrowing the venture capital ecosystem where investors' expertise is in understanding the product and technical risk rather than assessing the scalability part of the journey. Again, this creates an investment opportunity for those who understand how to analyse scalability.

Both these markets require extensive operational involvement, which necessitates higher fees, making them harder for cost-conscious allocators to access.

Baillie Gifford primarily operates in growth equity, which is characterised by minority investments in private high-growth companies. This strategy aims for venture-like upside with lower risk compared to early-stage venture capital.

Emergence of private growth equity

Companies are staying private longer, driven by structural changes such as the shift from active mutual funds to index funds and the alignment of shareholder interests.

The Great Financial Crisis marked a shift when companies realised “they had more safety in their growth plan if they stayed private,” said Kelly. He singled out Facebook for kickstarting the asset class, raising a massive $10bn privately before going public in 2012.

Previously, when companies went public, they would find investors within the deep pool of active mutual funds. Over the past decade, however, $3tn has moved from active into index funds, reducing the demand for smaller IPOs.

Once in public markets, companies cannot control their shareholders, and a diverse shareholder base will have different time horizons and objectives. However, they are likely to be united in their desire to maximise current cash flow, which can be at odds with maximising long-term growth potential.

Staying private for longer creates opportunities for companies to invest in long-term growth without the pressure of maximising current cash flow.

Kelly drew attention to SpaceX and Databricks as examples of private companies benefiting from strategic decisions prioritising long-term growth.

SpaceX, for example, is forgoing revenue by using its satellites in its spacecraft instead of third-party paying customers. That long-term approach would be challenging to do in the public markets.

In an AI-enabled world, Databricks is one of the leaders in cloud data, storage, and compute. It has made several billion-dollar acquisitions to cement its leadership in AI, which is more difficult for its public competitor, Snowflake.

Opportunities for DC allocators

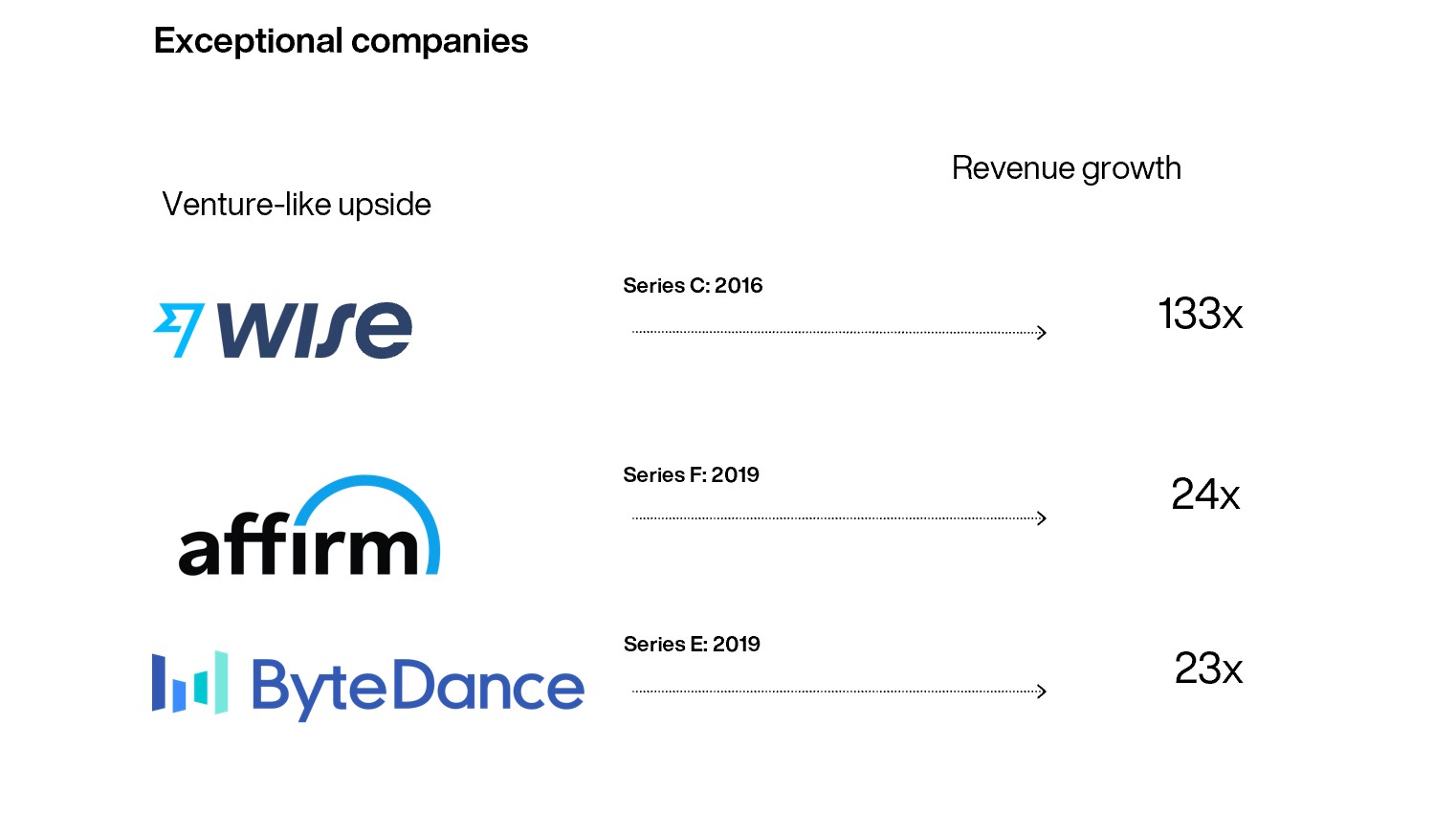

The session concluded with a discussion of the opportunities for DC allocators in private growth equity. Kelly reminded the audience that “growth equity has venture-like upside.”

To illustrate his point, he highlighted the revenue growth of Wise, Affirm and ByteDance during Baillie Gifford's ownership of them. This starkly contrasts public markets, with almost no growth forecast for the next 12 months.

Private growth - asset class feature

Source: Pitchbook. Data as at 30 September 2024. Logos courtesy of companies.

Baillie Gifford invests at the artificial inflection point when a great product becomes a great business, meaning that much of the uncertainty around demand for the product and the ability to execute has already been addressed. Therefore, he noted, “the risk is less than half of venture.”

The speakers emphasised the importance of access to exceptional companies such as Bending Spoons, selectivity, and fee structures when investing in private companies.

“Companies can pick their partners ... and typically they want someone who can also bring something to the table,” Kelly said.

In Baillie Gifford’s case, that’s its history of working with growth companies, which ties in with the selectivity point, as its investors are skilled at analysing what exceptional growth companies look like.

Private markets can be expensive, depending on how they are accessed. Venture funds have higher charges, which are less warranted for companies getting closer to public markets, where, as mentioned, you are no longer taking on the same level of risk.

Recognising the DC need for better liquidity and very low fees, Kelly highlighted the work Baillie Gifford is undertaking to broaden access to this asset class through customised funds and public-private structures.

Looking forward

Looking ahead, the speakers expressed optimism about the future of private growth equity. They noted that the post-Covid environment has created leaner and stronger companies, and current valuations present attractive opportunities for investors.

The goal is to continue generating returns through revenue growth and to broaden access to private growth equity for a broader range of investors.

Words by Gillian Christie

Rachael Callaghan, Investment Specialist

Rachael is an investment specialist in the Clients Department and is a member of the Private Companies Team. She joined Baillie Gifford in 2019 where she initially worked on one of our global equity ESG strategies before joining the Private Companies Team in 2020. Prior to joining the firm, she spent five years working as a regional and project manager for Aldi. Rachael graduated from the University of Durham in 2014 with an BA(Hons) in Modern Languages (French, German & Russian).

Brian Kelly, Investment Specialist

Brian is an investment specialist in the Clients Department and is a member of the Private Companies Team. He joined Baillie Gifford in 2024. Prior to joining the firm, he was head of Alternative Investments at Allen & Co Investment Advisors, where he oversaw investment research on opportunistic investments, alternatives, and third parties. Prior to Allen & Co, he was an analyst within global capital markets at Morgan Stanley in New York, focused on private capital markets and student loan securitizations. He graduated with a BSc in Mechanical Engineering from Brown University in 2008 and is a CFA Charterholder.

Risk factors

This communication was produced and approved in March 2025 and has not been updated subsequently. It represents views held at the time and may not reflect current thinking.

The views expressed should not be considered as advice or a recommendation to buy, sell or hold a particular investment. They reflect opinion and should not be taken as statements of fact nor should any reliance be placed on them when making investment decisions.

This communication contains information on investments which does not constitute independent research. Accordingly, it is not subject to the protections afforded to independent research and Baillie Gifford and its staff may have dealt in the investments concerned.

All information is sourced from Baillie Gifford & Co and is current unless otherwise stated.

The images used in this communication are for illustrative purposes only.

Past performance is not a guide to future performance.

Important Information

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). Baillie Gifford & Co Limited is an Authorised Corporate Director of OEICs.

142420 10053622